Question

Tango vs Victor Case You should develop a valuation model for the company Victor as is ( Scenario 1 ). you should project the Income

Tango vs Victor Case

You should develop a valuation model for the company Victor "as is" (Scenario 1). you should project the Income Statement and the Free Cash Flow to Equity (FCFE) for the next five years (2007/2011) using 2006 as the "base year".

As far as the Terminal Value was concerned:

- in Scenario 1 you should calculate the Equity TV (TVV) using the growing perpetuity formula with a growth rate (g) of 2.5%. Please take into account that after December 2011 there will be no more debt.

You should then answer the following questions:

What was the Enterprise Value of Victor "as is" (Scenario 1)? What was the Equity Value? What was the Equity Value of Victor "per share"? What was the difference between this value and the current share price?

in Scenario 2 you should assume that the Enterprise Value of New Victor at the end of 2011 (TVEV) will be equal to 6 times 2011 EBITDA and then calculate the Equity TV consistently.

For the sake of simplicity you should assume that the buyout would take place on 31st December 2006, and all cash flows should be discounted to that date. You should also assume that both the repayment of debt and the payment of dividends (whenever applicable) take place at the end of the year.

You should then answer the following questions:

1. What was the value of Victor if it was taken over by Tango through the leveraged buyout (Scenario 2)? Please calculate both the Equity Value and the Enterprise Value. You should note that, in this case, due to the constraint imposed by the lenders, the relevant equity cash flows are: the dividends actually received by the shareholders plus the Equity Terminal Value (TVV).

2. Assuming Victor was bought out by New Victor at 25 per share:

2.1 What would be the Equity investment of Tango? (In order to answer this question please prepare a Table of Sources and Applications of Funds in the buyout)

2.2 What percentage of the Equity in "New Victor" would the management hold? What percentage would Tango hold?

2.3 Please calculate the expected returns (Internal Rate of Return) for both the management team and Tango.

3. Based on your analysis should Bob do the deal?

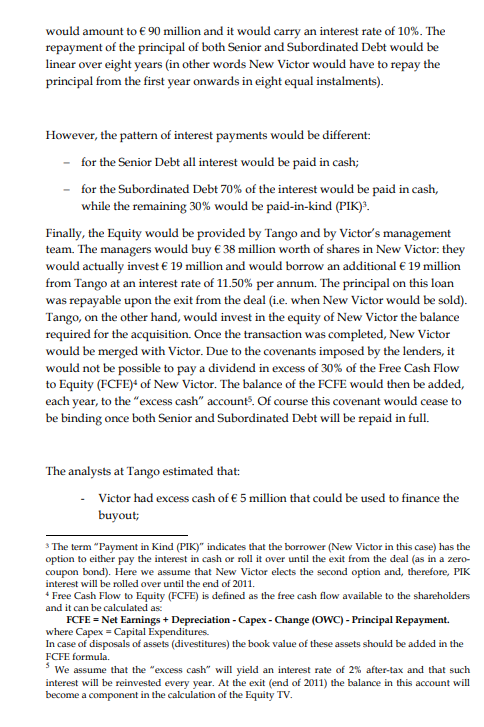

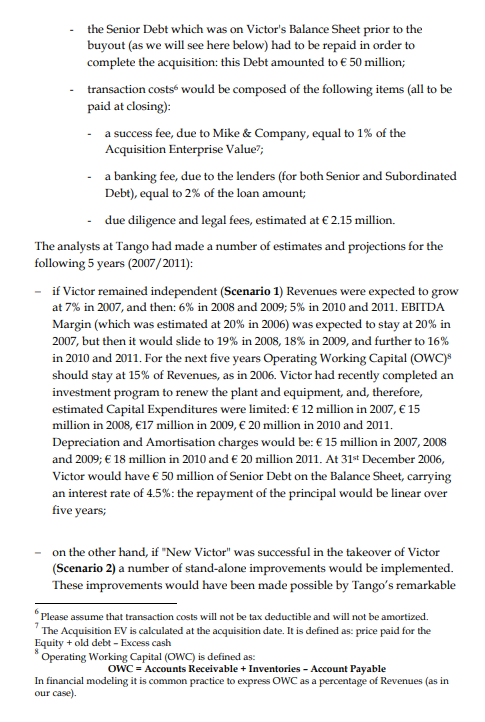

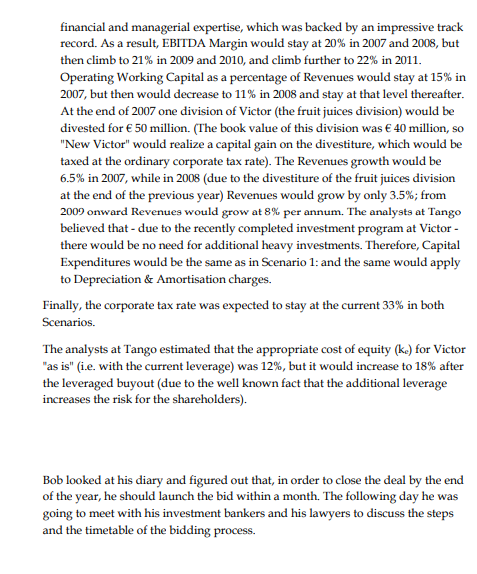

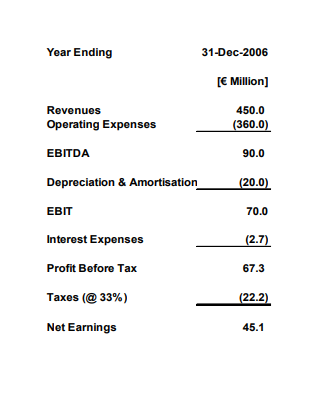

Tango vs. Victor - Part A On Tuesday 28h August, 2006 Bob Fisher, managing partner of Tango, a pan- European private equity fund, was sitting in his office in the West End of London. He had just come back from a long weekend in Ireland and he was considering whether or not his fund should invest in the leveraged buyout (LBO) of Victor, a French company in the soft drinks industry, which was exporting to Italy, Switzerland and the Benelux. This industry was considered a mature business with steady cash flows, and this made Victor an attractive candidate for an LBO. Bob and his colleagues believed that Victor's shares were undervalued in the market, and that there was room for realizing a substantial value by way of stand-alone improvements and divestiture of a non-strategic division. Moreover, the top 20 managers at Victor were ready to invest in the buyout and they were also ready to commit themselves to remain with the company for the next five years. During the month of July Bob had received the due diligence reports that he had commissioned to a well-known strategy-consulting firm and to his auditors and he felt very positive about the deal. He had also travelled to Paris to have lunch with Peter Clark, the CEO of Victor, and he was impressed by his personality and professional attitude. Exhibit A1 shows the estimate of the Income Statement of Victor for the year ending 315 December 2006. (These estimates were available to Bob and his colleagues at that time). Victor was listed on the Paris stock exchange: in August 2006 the share price was 20 per share. According to Mike & Company, Tango's investment bankers, a tender offer at 25 per share would be accepted by Victor's shareholders. There were 20,000,000 (twenty-million) shares outstanding. Tango planned to take over Victor through a leveraged vehicle ("New Victor"). New Victor would be financed through a mixture of debt and equity. The debt would be composed of Senior Debt' and Mezzanine (Subordinated Debt)2. The Senior Debt was going to be provided by a group of commercial banks: it would amount to 280 million and it would carry an interest rate of 5%. The Subordinated Debt would be provided by a group of financial institutions: it would amount to 90 million and it would carry an interest rate of 10%. The repayment of the principal of both Senior and Subordinated Debt would be linear over eight years in other words New Victor would have to repay the principal from the first year onwards in eight equal instalments). However, the pattern of interest payments would be different: - for the Senior Debt all interest would be paid in cash; for the Subordinated Debt 70% of the interest would be paid in cash, while the remaining 30% would be paid-in-kind (PIK). Finally, the Equity would be provided by Tango and by Victor's management team. The managers would buy 38 million worth of shares in New Victor: they would actually invest 19 million and would borrow an additional 19 million from Tango at an interest rate of 11.50% per annum. The principal on this loan was repayable upon the exit from the deal (i.e. when New Victor would be sold). Tango, on the other hand, would invest in the equity of New Victor the balance required for the acquisition. Once the transaction was completed, New Victor would be merged with Victor. Due to the covenants imposed by the lenders, it would not be possible to pay a dividend in excess of 30% of the Free Cash Flow to Equity (FCFE) of New Victor. The balance of the FCFE would then be added, each year, to the "excess cash" accounts. Of course this covenant would cease to be binding once both Senior and Subordinated Debt will be repaid in full. The analysts at Tango estimated that: Victor had excess cash of 5 million that could be used to finance the buyout; 3 The term "Payment in Kind (PIK)" indicates that the borrower (New Victor in this case) has the option to either pay the interest in cash or roll it over until the exit from the deal (as in a zero- coupon bond). Here we assume that New Victor elects the second option and therefore, PIK interest will be rolled over until the end of 2011. * Free Cash Flow to Equity (FCFE) is defined as the free cash flow available to the shareholders and it can be calculated as: FCFE = Net Earnings + Depreciation - Capex - Change (OWC) - Principal Repayment. where Capex - Capital Expenditures. In case of disposals of assets (divestitures) the book value of these assets should be added in the FCFE formula We assume that the "excess cash" will yield an interest rate of 2% after-tax and that such interest will be reinvested every year. At the exit (end of 2011) the balance in this account will become a component in the calculation of the Equity TV. the Senior Debt which was on Victor's Balance Sheet prior to the buyout (as we will see here below) had to be repaid in order to complete the acquisition: this Debt amounted to 50 million; transaction costs would be composed of the following items (all to be paid at closing): a success fee, due to Mike & Company, equal to 1% of the Acquisition Enterprise Value; a banking fee, due to the lenders (for both Senior and Subordinated Debt), equal to 2% of the loan amount due diligence and legal fees, estimated at 2.15 million. The analysts at Tango had made a number of estimates and projections for the following 5 years (2007/2011): - if Victor remained independent (Scenario 1) Revenues were expected to grow at 7% in 2007, and then: 6% in 2008 and 2009; 5% in 2010 and 2011. EBITDA Margin (which was estimated at 20% in 2006) was expected to stay at 20% in 2007, but then it would slide to 19% in 2008, 18% in 2009, and further to 16% in 2010 and 2011. For the next five years Operating Working Capital (OWC) should stay at 15% of Revenues, as in 2006. Victor had recently completed an investment program to renew the plant and equipment, and therefore, estimated Capital Expenditures were limited: 12 million in 2007, 15 million in 2008, 617 million in 2009, 20 million in 2010 and 2011. Depreciation and Amortisation charges would be: 15 million in 2007, 2008 and 2009; 18 million in 2010 and 20 million 2011. At 315 December 2006, Victor would have 50 million of Senior Debt on the Balance Sheet, carrying an interest rate of 4.5%: the repayment of the principal would be linear over five years; on the other hand, if "New Victor" was successful in the takeover of Victor (Scenario 2) a number of stand-alone improvements would be implemented. These improvements would have been made possible by Tango's remarkable Please assume that transaction costs will not be tax deductible and will not be amortized. The Acquisition EV is calculated at the acquisition date. It is defined as: price paid for the Equity + old debt - Excess cash Operating Working Capital (OWC) is defined as: OWC = Accounts Receivable + Inventories - Account Payable In financial modeling it is common practice to express OWC as a percentage of Revenues (as in our case). financial and managerial expertise, which was backed by an impressive track record. As a result, EBITDA Margin would stay at 20% in 2007 and 2008, but then climb to 21% in 2009 and 2010, and climb further to 22% in 2011. Operating Working Capital as a percentage of Revenues would stay at 15% in 2007, but then would decrease to 11% in 2008 and stay at that level thereafter. At the end of 2007 one division of Victor (the fruit juices division) would be divested for 50 million. (The book value of this division was 40 million, so "New Victor" would realize a capital gain on the divestiture, which would be taxed at the ordinary corporate tax rate). The Revenues growth would be 6.5% in 2007, while in 2008 (due to the divestiture of the fruit juices division at the end of the previous year) Revenues would grow by only 3.5%; from 2009 onward Revenues would grow at 8% per annum. The analysts at Tango believed that - due to the recently completed investment program at Victor - there would be no need for additional heavy investments. Therefore, Capital Expenditures would be the same as in Scenario 1: and the same would apply to Depreciation & Amortisation charges. Finally, the corporate tax rate was expected to stay at the current 33% in both Scenarios. The analysts at Tango estimated that the appropriate cost of equity (ke) for Victor "as is" (i.e. with the current leverage) was 12%, but it would increase to 18% after the leveraged buyout (due to the well known fact that the additional leverage increases the risk for the shareholders). Bob looked at his diary and figured out that, in order to close the deal by the end of the year, he should launch the bid within a month. The following day he was going to meet with his investment bankers and his lawyers to discuss the steps and the timetable of the bidding process. Year Ending 31-Dec-2006 [ Million] Revenues Operating Expenses 450.0 (360.0) EBITDA 90.0 Depreciation & Amortisation (20.0) EBIT 70.0 (2.7) Interest Expenses Profit Before Tax 67.3 Taxes (@33%) (22.2) Net Earnings 45.1 Tango vs. Victor - Part A On Tuesday 28h August, 2006 Bob Fisher, managing partner of Tango, a pan- European private equity fund, was sitting in his office in the West End of London. He had just come back from a long weekend in Ireland and he was considering whether or not his fund should invest in the leveraged buyout (LBO) of Victor, a French company in the soft drinks industry, which was exporting to Italy, Switzerland and the Benelux. This industry was considered a mature business with steady cash flows, and this made Victor an attractive candidate for an LBO. Bob and his colleagues believed that Victor's shares were undervalued in the market, and that there was room for realizing a substantial value by way of stand-alone improvements and divestiture of a non-strategic division. Moreover, the top 20 managers at Victor were ready to invest in the buyout and they were also ready to commit themselves to remain with the company for the next five years. During the month of July Bob had received the due diligence reports that he had commissioned to a well-known strategy-consulting firm and to his auditors and he felt very positive about the deal. He had also travelled to Paris to have lunch with Peter Clark, the CEO of Victor, and he was impressed by his personality and professional attitude. Exhibit A1 shows the estimate of the Income Statement of Victor for the year ending 315 December 2006. (These estimates were available to Bob and his colleagues at that time). Victor was listed on the Paris stock exchange: in August 2006 the share price was 20 per share. According to Mike & Company, Tango's investment bankers, a tender offer at 25 per share would be accepted by Victor's shareholders. There were 20,000,000 (twenty-million) shares outstanding. Tango planned to take over Victor through a leveraged vehicle ("New Victor"). New Victor would be financed through a mixture of debt and equity. The debt would be composed of Senior Debt' and Mezzanine (Subordinated Debt)2. The Senior Debt was going to be provided by a group of commercial banks: it would amount to 280 million and it would carry an interest rate of 5%. The Subordinated Debt would be provided by a group of financial institutions: it would amount to 90 million and it would carry an interest rate of 10%. The repayment of the principal of both Senior and Subordinated Debt would be linear over eight years in other words New Victor would have to repay the principal from the first year onwards in eight equal instalments). However, the pattern of interest payments would be different: - for the Senior Debt all interest would be paid in cash; for the Subordinated Debt 70% of the interest would be paid in cash, while the remaining 30% would be paid-in-kind (PIK). Finally, the Equity would be provided by Tango and by Victor's management team. The managers would buy 38 million worth of shares in New Victor: they would actually invest 19 million and would borrow an additional 19 million from Tango at an interest rate of 11.50% per annum. The principal on this loan was repayable upon the exit from the deal (i.e. when New Victor would be sold). Tango, on the other hand, would invest in the equity of New Victor the balance required for the acquisition. Once the transaction was completed, New Victor would be merged with Victor. Due to the covenants imposed by the lenders, it would not be possible to pay a dividend in excess of 30% of the Free Cash Flow to Equity (FCFE) of New Victor. The balance of the FCFE would then be added, each year, to the "excess cash" accounts. Of course this covenant would cease to be binding once both Senior and Subordinated Debt will be repaid in full. The analysts at Tango estimated that: Victor had excess cash of 5 million that could be used to finance the buyout; 3 The term "Payment in Kind (PIK)" indicates that the borrower (New Victor in this case) has the option to either pay the interest in cash or roll it over until the exit from the deal (as in a zero- coupon bond). Here we assume that New Victor elects the second option and therefore, PIK interest will be rolled over until the end of 2011. * Free Cash Flow to Equity (FCFE) is defined as the free cash flow available to the shareholders and it can be calculated as: FCFE = Net Earnings + Depreciation - Capex - Change (OWC) - Principal Repayment. where Capex - Capital Expenditures. In case of disposals of assets (divestitures) the book value of these assets should be added in the FCFE formula We assume that the "excess cash" will yield an interest rate of 2% after-tax and that such interest will be reinvested every year. At the exit (end of 2011) the balance in this account will become a component in the calculation of the Equity TV. the Senior Debt which was on Victor's Balance Sheet prior to the buyout (as we will see here below) had to be repaid in order to complete the acquisition: this Debt amounted to 50 million; transaction costs would be composed of the following items (all to be paid at closing): a success fee, due to Mike & Company, equal to 1% of the Acquisition Enterprise Value; a banking fee, due to the lenders (for both Senior and Subordinated Debt), equal to 2% of the loan amount due diligence and legal fees, estimated at 2.15 million. The analysts at Tango had made a number of estimates and projections for the following 5 years (2007/2011): - if Victor remained independent (Scenario 1) Revenues were expected to grow at 7% in 2007, and then: 6% in 2008 and 2009; 5% in 2010 and 2011. EBITDA Margin (which was estimated at 20% in 2006) was expected to stay at 20% in 2007, but then it would slide to 19% in 2008, 18% in 2009, and further to 16% in 2010 and 2011. For the next five years Operating Working Capital (OWC) should stay at 15% of Revenues, as in 2006. Victor had recently completed an investment program to renew the plant and equipment, and therefore, estimated Capital Expenditures were limited: 12 million in 2007, 15 million in 2008, 617 million in 2009, 20 million in 2010 and 2011. Depreciation and Amortisation charges would be: 15 million in 2007, 2008 and 2009; 18 million in 2010 and 20 million 2011. At 315 December 2006, Victor would have 50 million of Senior Debt on the Balance Sheet, carrying an interest rate of 4.5%: the repayment of the principal would be linear over five years; on the other hand, if "New Victor" was successful in the takeover of Victor (Scenario 2) a number of stand-alone improvements would be implemented. These improvements would have been made possible by Tango's remarkable Please assume that transaction costs will not be tax deductible and will not be amortized. The Acquisition EV is calculated at the acquisition date. It is defined as: price paid for the Equity + old debt - Excess cash Operating Working Capital (OWC) is defined as: OWC = Accounts Receivable + Inventories - Account Payable In financial modeling it is common practice to express OWC as a percentage of Revenues (as in our case). financial and managerial expertise, which was backed by an impressive track record. As a result, EBITDA Margin would stay at 20% in 2007 and 2008, but then climb to 21% in 2009 and 2010, and climb further to 22% in 2011. Operating Working Capital as a percentage of Revenues would stay at 15% in 2007, but then would decrease to 11% in 2008 and stay at that level thereafter. At the end of 2007 one division of Victor (the fruit juices division) would be divested for 50 million. (The book value of this division was 40 million, so "New Victor" would realize a capital gain on the divestiture, which would be taxed at the ordinary corporate tax rate). The Revenues growth would be 6.5% in 2007, while in 2008 (due to the divestiture of the fruit juices division at the end of the previous year) Revenues would grow by only 3.5%; from 2009 onward Revenues would grow at 8% per annum. The analysts at Tango believed that - due to the recently completed investment program at Victor - there would be no need for additional heavy investments. Therefore, Capital Expenditures would be the same as in Scenario 1: and the same would apply to Depreciation & Amortisation charges. Finally, the corporate tax rate was expected to stay at the current 33% in both Scenarios. The analysts at Tango estimated that the appropriate cost of equity (ke) for Victor "as is" (i.e. with the current leverage) was 12%, but it would increase to 18% after the leveraged buyout (due to the well known fact that the additional leverage increases the risk for the shareholders). Bob looked at his diary and figured out that, in order to close the deal by the end of the year, he should launch the bid within a month. The following day he was going to meet with his investment bankers and his lawyers to discuss the steps and the timetable of the bidding process. Year Ending 31-Dec-2006 [ Million] Revenues Operating Expenses 450.0 (360.0) EBITDA 90.0 Depreciation & Amortisation (20.0) EBIT 70.0 (2.7) Interest Expenses Profit Before Tax 67.3 Taxes (@33%) (22.2) Net Earnings 45.1

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Production And Operations Analysis

Authors: Steven Nahmias, Tava Lennon Olsen

7th Edition

1478623063, 9781478623069