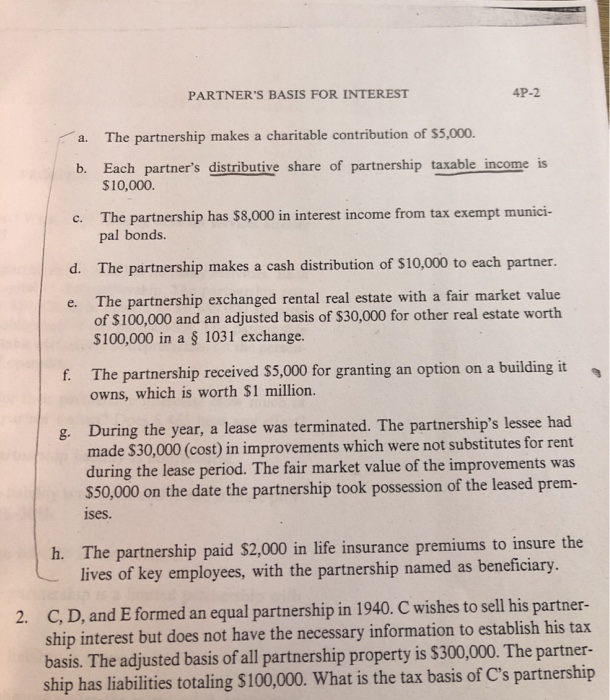

Tax Problem

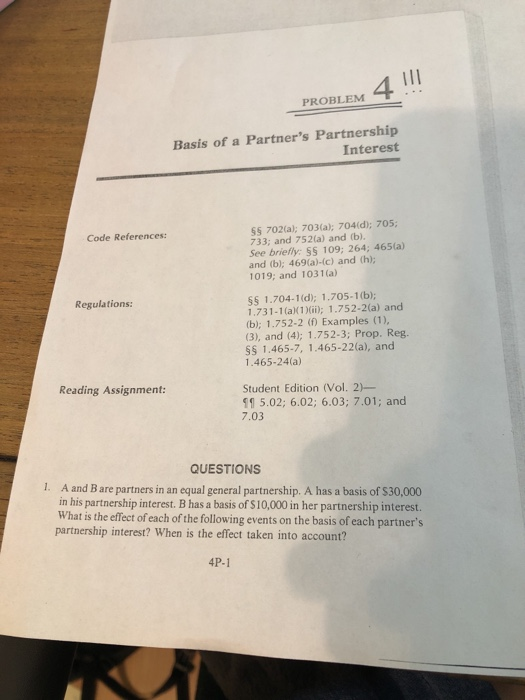

OBLEM 4 11 Basis of a Partner's Partnership Interest Code References: S$ 702 Cal; 703a); 704(d); 705; 733; and 752(a) and (b). See briefly: 55 109; 264; 465(a) and (b); 469(a)-(c) and th); 1019; and 1031(a) Regulations: SS 1.704-1(d); 1.705-1(b); 1.731-1(a)(1)(ii); 1.752-2(a) and (b); 1.752-2 (Examples (1), (3), and (4); 1.752-3; Prop. Reg. SS 1.465-7, 1.465-22(a), and 1.465-24(a) Reading Assignment: Student Edition (Vol. 2) 195.02; 6.02; 6.03; 7.01; and 7.03 QUESTIONS 1. A and B are partners in an equal general partnership. A has a basis of $30,000 in his partnership interest. B has a basis of $10,000 in her partnership interest. What is the effect of each of the following events on the basis of each partner's partnership interest? When is the effect taken into account? 4P-1 PARTNER'S BASIS FOR INTEREST 4P-2 a. b. The partnership makes a charitable contribution of $5,000. Each partner's distributive share of partnership taxable income is $10,000. c. The partnership has $8,000 in interest income from tax exempt munici- pal bonds. d. The partnership makes a cash distribution of $10,000 to each partner. e. The partnership exchanged rental real estate with a fair market value of $100,000 and an adjusted basis of $30,000 for other real estate worth $100,000 in a $ 1031 exchange. f. The partnership received $5,000 for granting an option on a building it owns, which is worth $1 million. g. During the year, a lease was terminated. The partnership's lessee had made $30,000 (cost) in improvements which were not substitutes for rent during the lease period. The fair market value of the improvements was $50,000 on the date the partnership took possession of the leased prem- ises. h. The partnership paid $2,000 in life insurance premiums to insure the lives of key employees, with the partnership named as beneficiary. 2. C, D, and E formed an equal partnership in 1940. C wishes to sell his partner- ship interest but does not have the necessary information to establish his tax basis. The adjusted basis of all partnership property is $300,000. The partner- ship has liabilities totaling $100,000. What is the tax basis of C's partnership OBLEM 4 11 Basis of a Partner's Partnership Interest Code References: S$ 702 Cal; 703a); 704(d); 705; 733; and 752(a) and (b). See briefly: 55 109; 264; 465(a) and (b); 469(a)-(c) and th); 1019; and 1031(a) Regulations: SS 1.704-1(d); 1.705-1(b); 1.731-1(a)(1)(ii); 1.752-2(a) and (b); 1.752-2 (Examples (1), (3), and (4); 1.752-3; Prop. Reg. SS 1.465-7, 1.465-22(a), and 1.465-24(a) Reading Assignment: Student Edition (Vol. 2) 195.02; 6.02; 6.03; 7.01; and 7.03 QUESTIONS 1. A and B are partners in an equal general partnership. A has a basis of $30,000 in his partnership interest. B has a basis of $10,000 in her partnership interest. What is the effect of each of the following events on the basis of each partner's partnership interest? When is the effect taken into account? 4P-1 PARTNER'S BASIS FOR INTEREST 4P-2 a. b. The partnership makes a charitable contribution of $5,000. Each partner's distributive share of partnership taxable income is $10,000. c. The partnership has $8,000 in interest income from tax exempt munici- pal bonds. d. The partnership makes a cash distribution of $10,000 to each partner. e. The partnership exchanged rental real estate with a fair market value of $100,000 and an adjusted basis of $30,000 for other real estate worth $100,000 in a $ 1031 exchange. f. The partnership received $5,000 for granting an option on a building it owns, which is worth $1 million. g. During the year, a lease was terminated. The partnership's lessee had made $30,000 (cost) in improvements which were not substitutes for rent during the lease period. The fair market value of the improvements was $50,000 on the date the partnership took possession of the leased prem- ises. h. The partnership paid $2,000 in life insurance premiums to insure the lives of key employees, with the partnership named as beneficiary. 2. C, D, and E formed an equal partnership in 1940. C wishes to sell his partner- ship interest but does not have the necessary information to establish his tax basis. The adjusted basis of all partnership property is $300,000. The partner- ship has liabilities totaling $100,000. What is the tax basis of C's partnership