Answered step by step

Verified Expert Solution

Question

1 Approved Answer

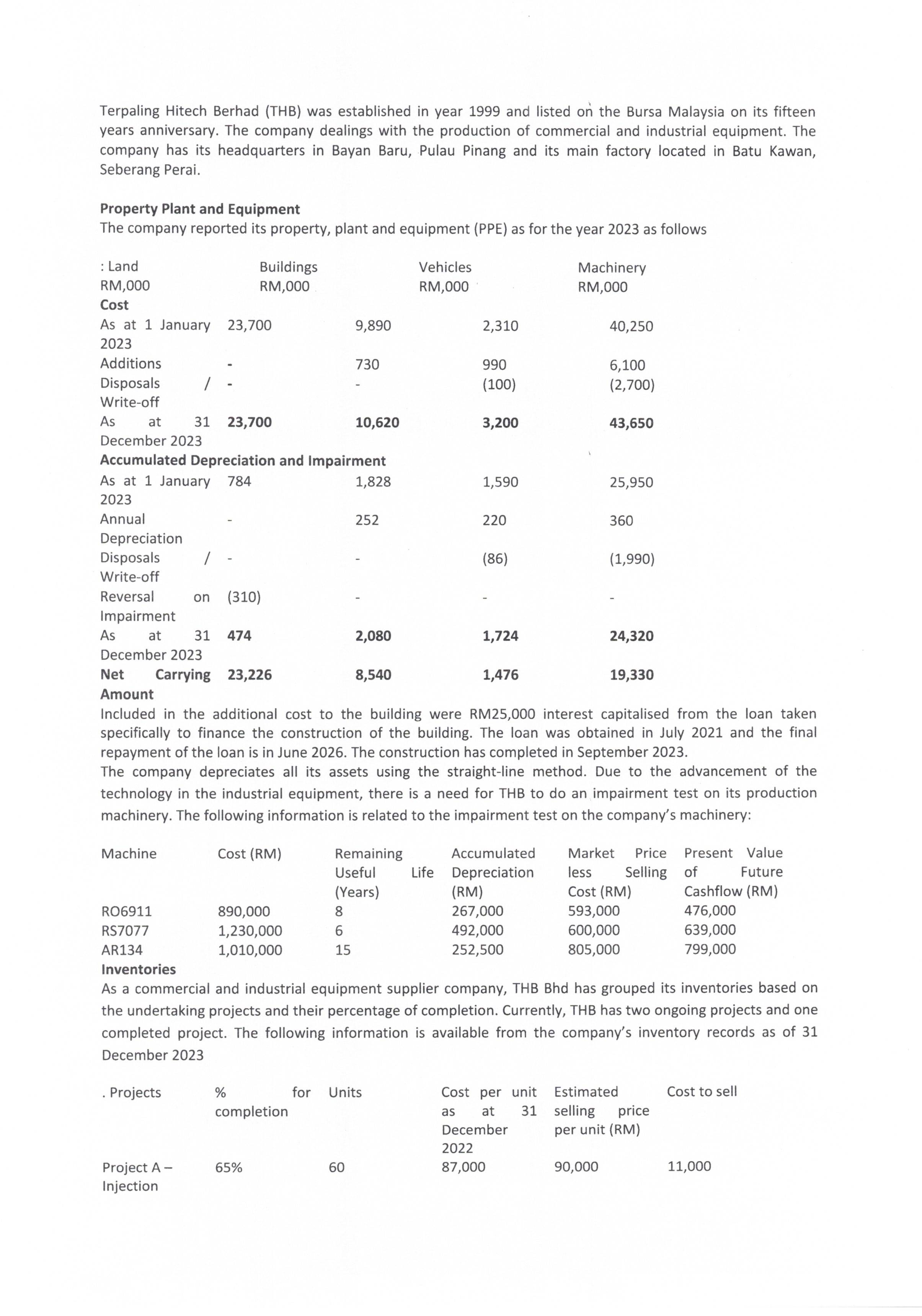

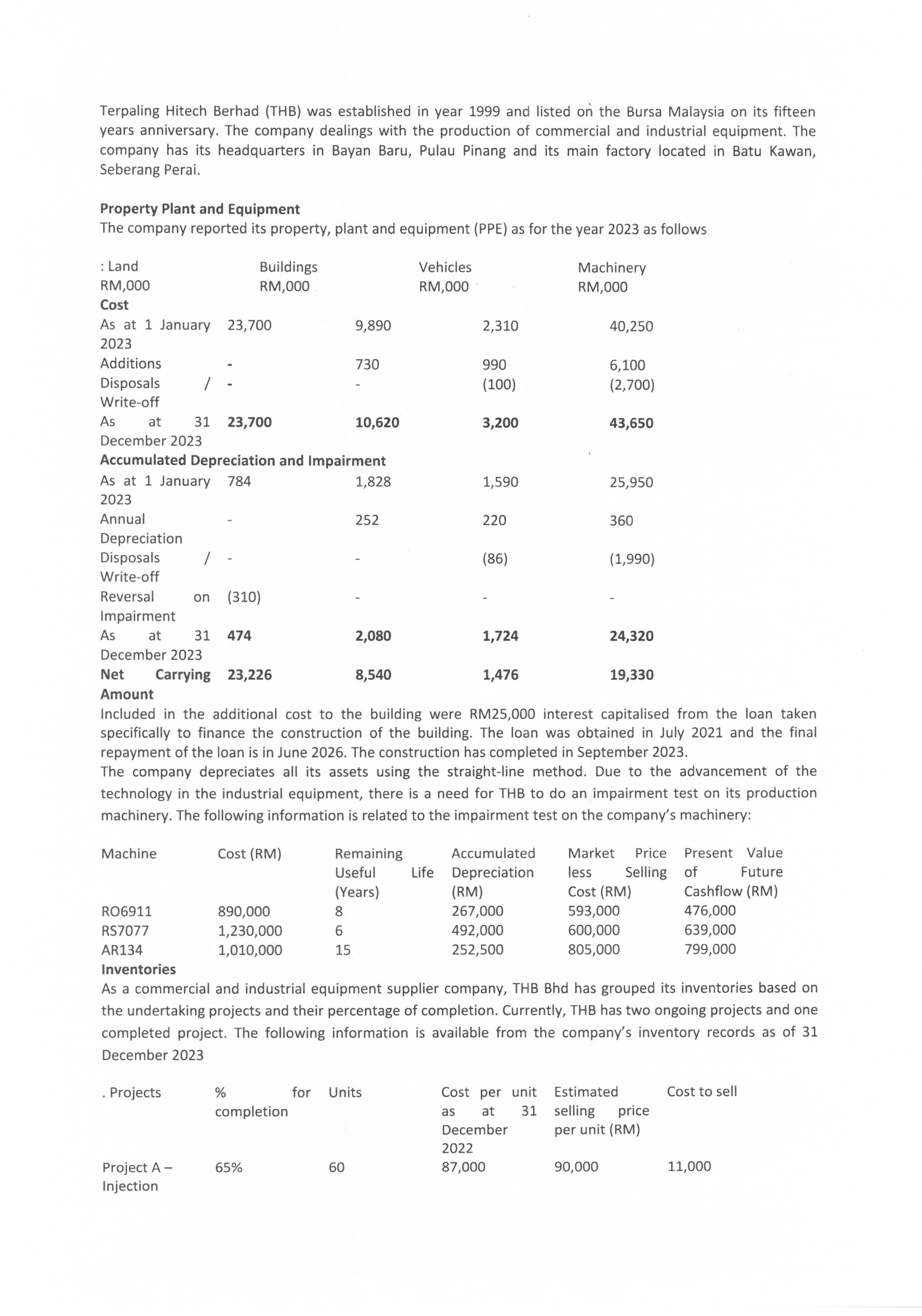

Terpaling Hitech Berhad ( THB ) was established in year 1 9 9 9 and listed on the Bursa Malaysia on its fifteen years anniversary.

Terpaling Hitech Berhad THB was established in year and listed on the Bursa Malaysia on its fifteen

years anniversary. The company dealings with the production of commercial and industrial equipment. The

company has its headquarters in Bayan Baru, Pulau Pinang and its main factory located in Batu Kawan,

Seberang Perai.

Property Plant and Equipment

The company reported its property, plant and equipment PPE as for the year as follows

Amount

Included in the additional cost to the building were RM interest capitalised from the loan taken

specifically to finance the construction of the building. The loan was obtained in July and the final

repayment of the loan is in June The construction has completed in September

The company depreciates all its assets using the straightline method. Due to the advancement of the

technology in the industrial equipment, there is a need for THB to do an impairment test on its production

machinery. The following information is related to the impairment test on the company's machinery:

Inventories

As a commercial and industrial equipment supplier company, THB Bhd has grouped its inventories based on

the undertaking projects and their percentage of completion. Currently, THB has two ongoing projects and one

completed project. The following information is available from the company's inventory records as of

December Molding

Cost to complete per unit is estimated based on the for completion cost per unit as at December

Intangible assets

On December THB recorded an intangible asset, patent, at a revalued amount of RM The

patent is related to a sustainable technology in the commercial and industrial equipment, which was

developed by the R&D team of the company. The patent was initially recorded at RM on January

The management of the company expected that the estimated future benefits from the patent would be

consumed evenly for the next eight years. In due to advancement of new technology, the company

revalued the patent to market value of and revalued the remaining useful life of the patent to be

two years. Beside the patent, other intangible assets of THB consist of:

i A customer list purchased on April at a cost of RM The company expected that of

the estimated future benefits from the customer list will flow into the company in and the rest will be

generated evenly in the next three years.

i The company acquired a legal title to an industrial equipment brand on June for RM

The legal life of the brand is five years but is renewable every five years at little cost. The company intends to

renew it continuously. One of the company's directors believes that the brand should be amortised and an

impairment test should only be carried out when the brand is renewed. In due to covid pandemic the

company is expected to lose of the market share. However, it has evidence that the brand product will

generate positive cash inflows indefinitely.

Mr Lohan is a newly appointed Chief Operating Officer COO of THB He is an accounting graduate from the

most eminent university in Malaysia. He never involve in any accounting or auditing firms since his graduation.

He experienced more on marketing and investment activities than accounting. Thus, his knowledge of

accounting is limited and not uptodate. During the presentation by Madam Kay, the Head of Accounting

Depatment, Mr Lohan was expecting that the total interest from the bank loan taken to finance the newly

completed building, should be capitalised continuously until June Mr Lohan was also arguing on the

practice of impairment on the machineries. He feels that it might have a negative effect on the balance sheet

and related financial ratios because it may have a lower market value than its book value. He suggested that

the impairment test should not be carried out during the use of the asset and any loss would only be recorded

on the date of the disposal of the assets. Mr Lohan believes that the carrying amount shown in the statement

of financial postion is sufficient to show the current value of the assets. Further, Mr Lohan is also not literally

agreed with the use of LCNRV approach to determine the value of company's inventory as he is in the opinion

that it might distort the company's income data.

CASE INSTRUCTIONS ANSWER ALL THE QUESTIONS:

Briefly explain to Mr Lohan on the borrowing cost related to the construction of the

building, whether should be capitalise or expense. Support your explanations with the related

Malaysian accounting standard.

With regards to the argument on the impairment of the assets between Mr Lohan and

Madam Kay: a What is the issue facing Mr Lohan and Madam Kay? b Would the suggestion by Mr

Lohan affect THB

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

College Accounting A Contemporary Approach

Authors: David Haddock, John Price, Michael Farina

4th edition

978-1259995057, 1259995054, 978-0077503987, 77503988, 978-0077639730