Answered step by step

Verified Expert Solution

Question

1 Approved Answer

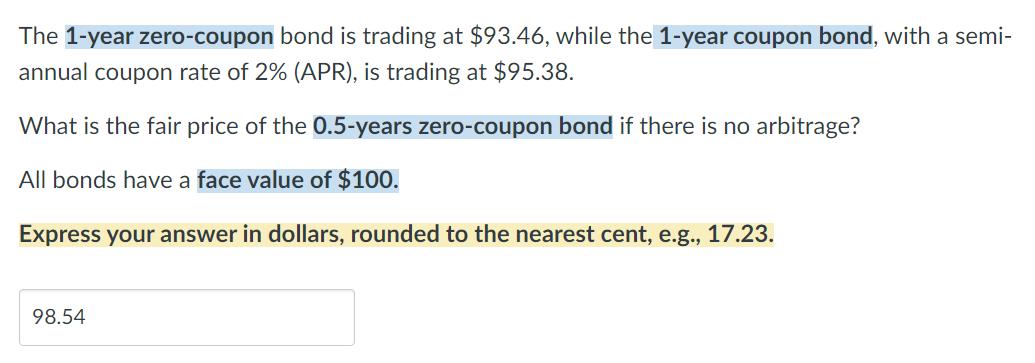

The 1-year zero-coupon bond is trading at $93.46, while the 1-year coupon bond, with a semi- annual coupon rate of 2% (APR), is trading

The 1-year zero-coupon bond is trading at $93.46, while the 1-year coupon bond, with a semi- annual coupon rate of 2% (APR), is trading at $95.38. What is the fair price of the 0.5-years zero-coupon bond if there is no arbitrage? All bonds have a face value of $100. Express your answer in dollars, rounded to the nearest cent, e.g., 17.23. 98.54

Step by Step Solution

There are 3 Steps involved in it

Step: 1

To calculate the fair price of the 05year zerocoupon bond we can use the concept of noarbitrage If t...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Practical Management Science

Authors: Wayne L. Winston, Christian Albright

5th Edition

1305631540, 1305631544, 1305250907, 978-1305250901