Answered step by step

Verified Expert Solution

Question

1 Approved Answer

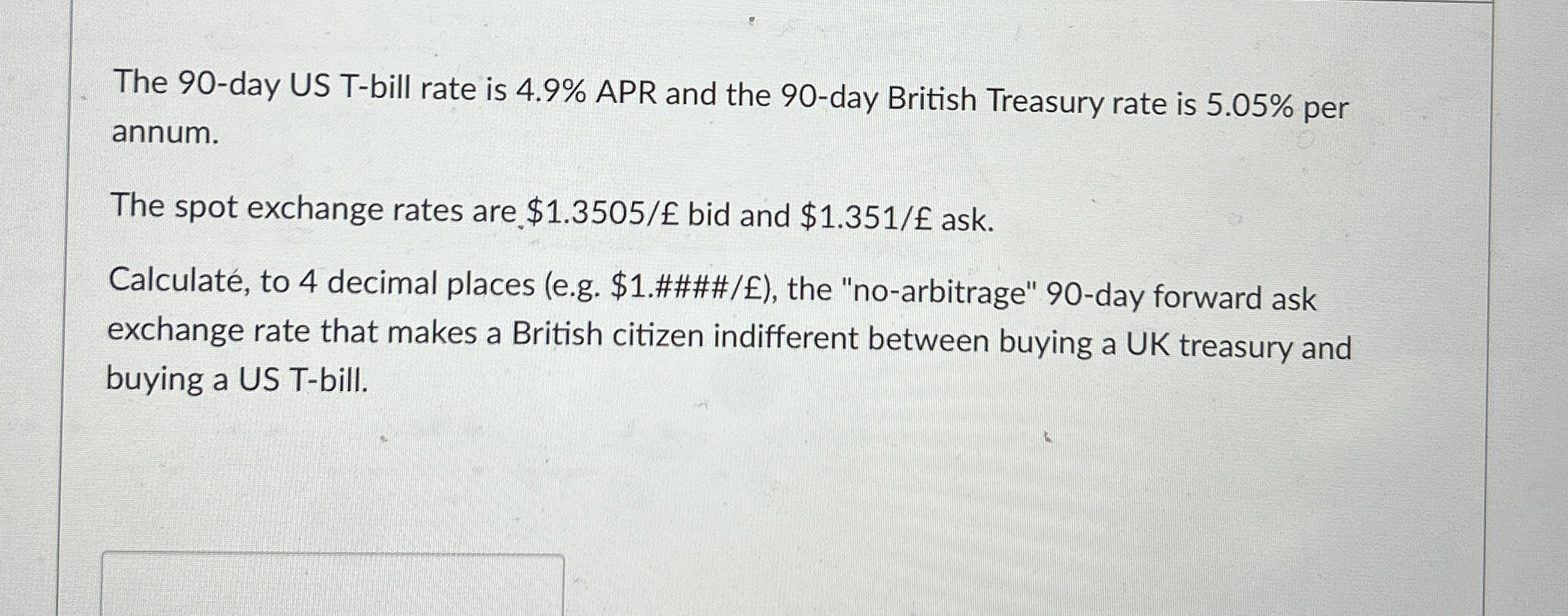

The 9 0 - day US T - bill rate is 4 . 9 % APR and the 9 0 - day British Treasury rate

The day US Tbill rate is APR and the day British Treasury rate is per annum.

The spot exchange rates are. $ bid and $ ask.

Calculat to decimal places eg $#### the noarbitrage" day forward ask exchange rate that makes a British citizen indifferent between buying a UK treasury and buying a US Tbill.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started