Answered step by step

Verified Expert Solution

Question

1 Approved Answer

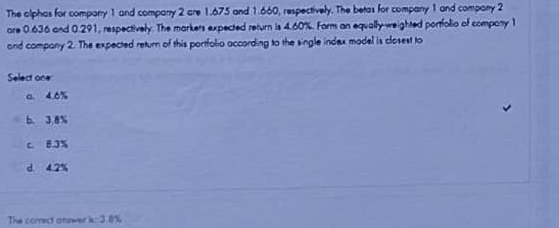

The alphas for company 1 and company 2 are 1 . 6 7 5 and 1 . 6 6 0 , respectively. The beta for

The alphas for company and company are and respectively. The beta for company and company are and respectively. The expected return of this portfolio according to the single index model is closest to

a

b

c

d

The answer is b write out the workings

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Reinventing The CFO How Financial Managers Can Transform Their Roles And Add Greater Value

Authors: Jeremy Hope

1st Edition

1591399459, 978-1591399452