Question

The analysts at ABC Plc use a two-step process to manage the assets and risk in their portfolio. First, they use a Value at Risk

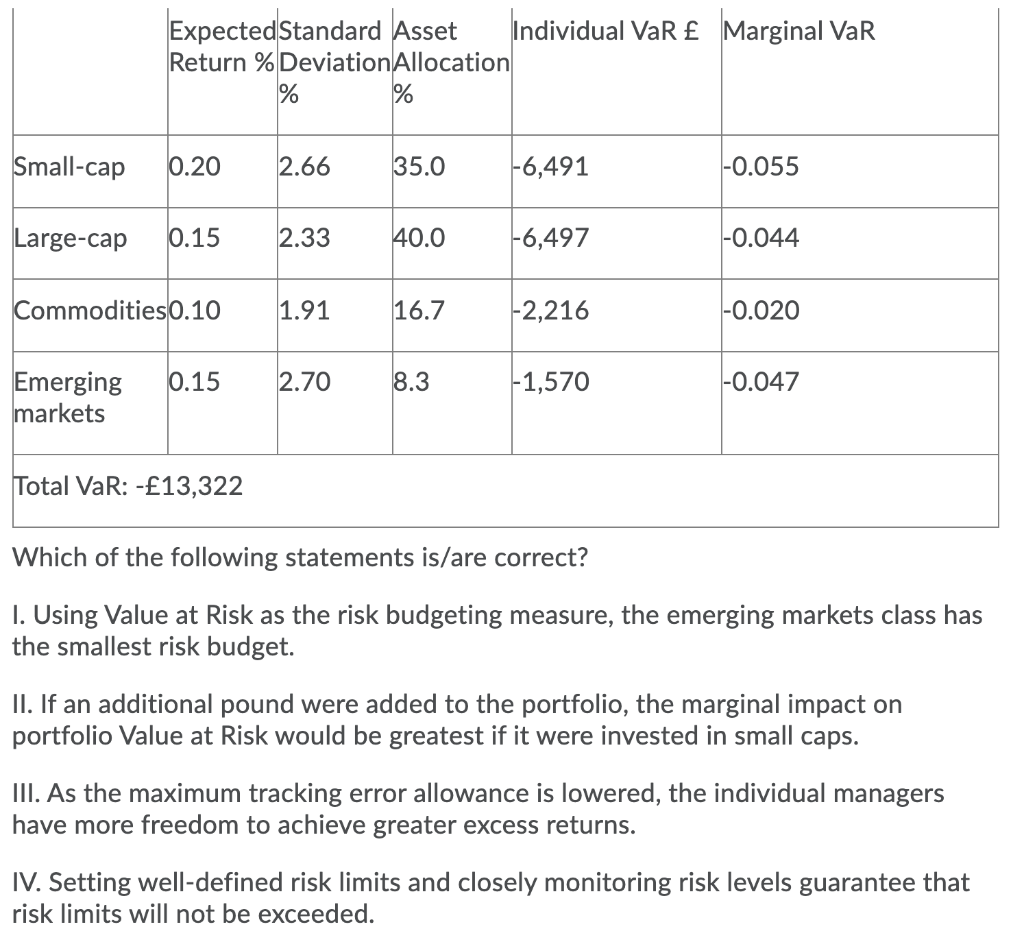

The analysts at ABC Plc use a two-step process to manage the assets and risk in their portfolio. First, they use a Value at Risk (VaR)-based risk budgeting process to determine the asset allocation across four broad asset classes. Then, within each asset class, they set a maximum tracking error allowance from a benchmark index and determine an active risk budget to distribute among individual managers. Assume the returns are all normally distributed. From the first step in the process, the following information is available.

| I and II only. | |

|

| I, II, III, and IV. |

|

| II and III. |

|

| I only. |

|

| None of the other answers. |

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Elements Of Structured Finance

Authors: Ann Rutledge, Sylvain Raynes

1st Edition

0195179986, 978-0195179989