The annual risk free rate is 0.02. We have the following information about three risky assets (on an annual basis). Asset 1 Asset 2

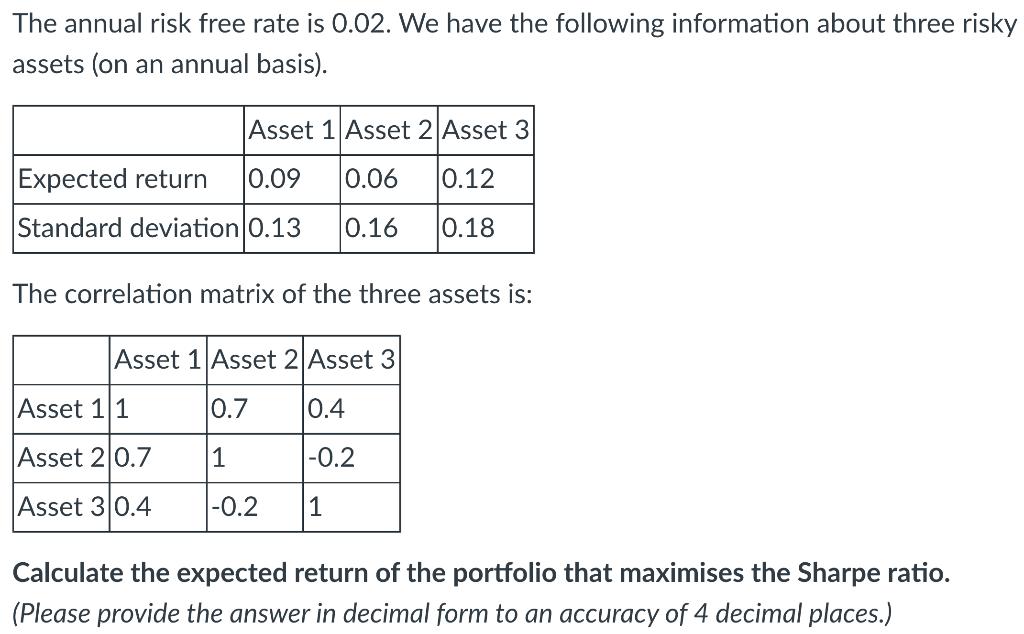

The annual risk free rate is 0.02. We have the following information about three risky assets (on an annual basis). Asset 1 Asset 2 Asset 3 Expected return 10.09 0.06 0.12 Standard deviation 0.13 0.16 0.18 The correlation matrix of the three assets is: Asset 1 Asset 2 Asset 3 0.7 0.4 1 -0.2 -0.2 1 Asset 11 Asset 2 0.7 Asset 3 0.4 Calculate the expected return of the portfolio that maximises the Sharpe ratio. (Please provide the answer in decimal form to an accuracy of 4 decimal places.)

Step by Step Solution

3.40 Rating (156 Votes )

There are 3 Steps involved in it

Step: 1

Expected re...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Charles Henry Brase, Corrinne Pellillo Brase

6th Edition

978-1133525097, 1133525091, 1111827028, 978-1133110316, 1133110312, 978-1111827021