Answered step by step

Verified Expert Solution

Question

1 Approved Answer

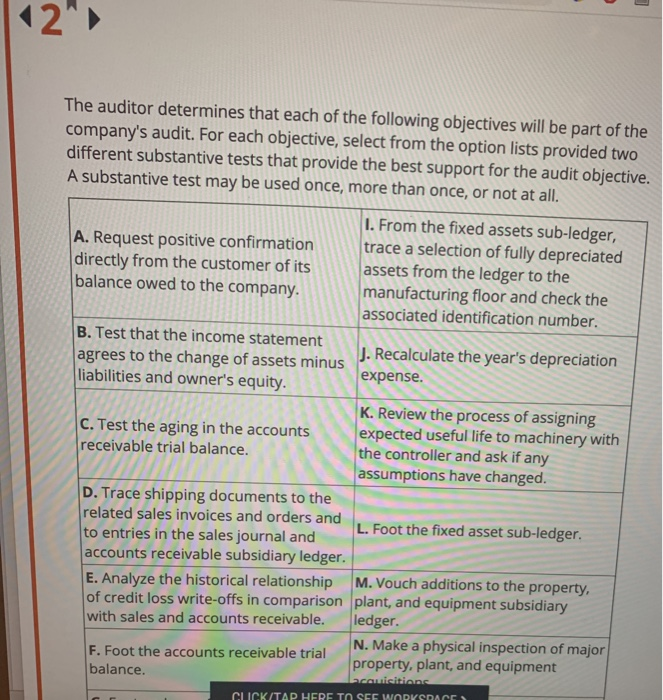

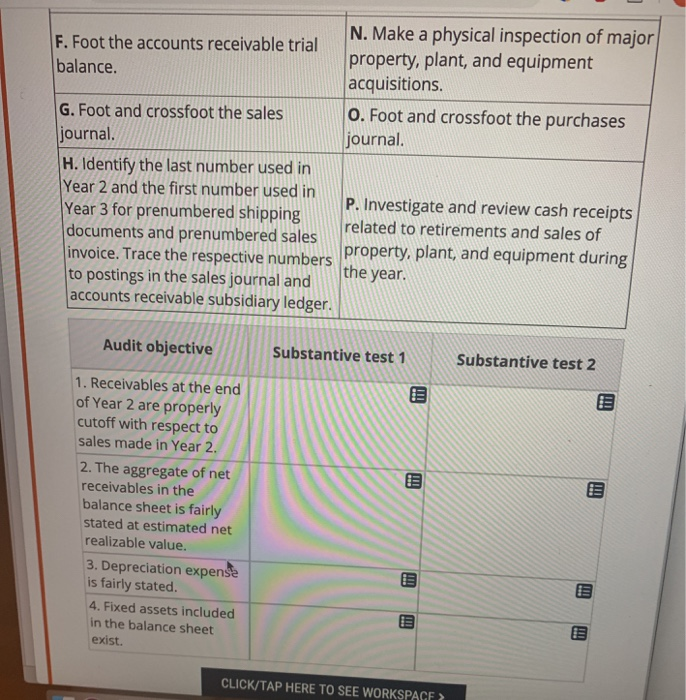

The auditor determines that each of the following objectives will be part of the company's audit. For each objective, select from the option lists provided

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Wiley CPAexcel Exam Review 2016 Study Guide January Auditing And Attestation

Authors: O. Ray Whittington

1st Edition

1119119960, 978-1119119968