Question

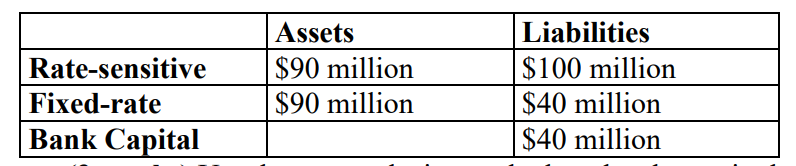

the balance sheet of the Bank can be divided as follows: (i) Use the gap analysis to calculate the change in the banks profit if

the balance sheet of the Bank can be divided as follows:

(i) Use the gap analysis to calculate the change in the banks profit if the interest rate decreases from 9% to 6%.

(ii) Suppose that the average duration of its assets is four years, while the average duration of its liabilities is six years. Use the duration analysis to calculate the approximate change of the banks net worth as a percentage of the total original asset value if the interest rate decreases from 9% to 6%.

(iii) Given your answers above, suggest what the bank manager can do to reduce the interest rate risk the bank faces when the interest rate is too high and is likely to fall in the near future.

Rate-sensitive Fixed-rate Bank Capital Assets $90 million $90 million Liabilities $100 million $40 million $40 millionStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investment Theory And Risk Management

Authors: Steven Peterson

1st Edition

9781118129593