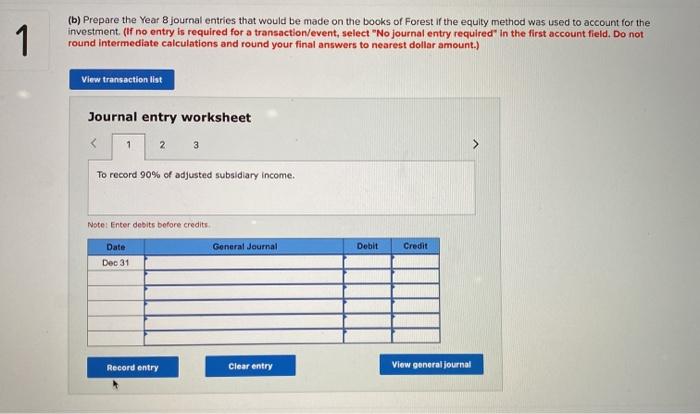

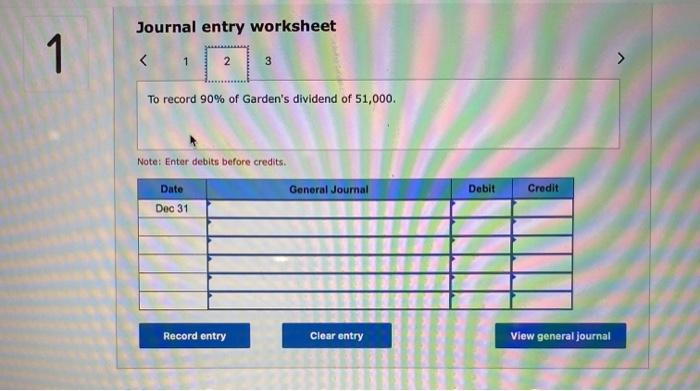

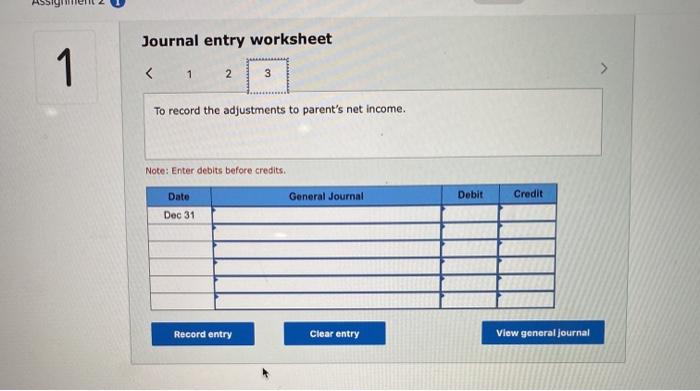

The balance sheets of Forest Company and Garden Company are presented below as at December 31, Year 8. 1 Garden $ 49,800 87,674 63,800 BALANCE SHEETS At December 31, Year 8 Forest Cash $ 13, 100 Receivables 25,100 Inventories 80, 100 Investment in shares of Garden 215, 100 Plant and equipment 740, 100 Accumulated depreciation (625, 8001 Patents Investment in bonds of Forest $ 447,700 Current liabilities $ 59, 169 Dividends payable 6,000 Bonds payable 6 94,846 Common shares 200,000 Retained earnings 87.685 $ 447,700 461,000 (349,400) 5,500 58,426 $ 376,000 $ 54,000 31,000 150,000 141,800 $ 376,000 Additional Information Forest acquired 90% of Garden for $215,100 on July 1. Year 1, and accounts for its investment under the cost method. At that time. the shareholders' equity of Garden amounted to $176,000, the accumulated amortization was $96,000, and the assets of Garden were undervalued by the following amounts: Inventory Buildings Patents $13,000 $11,000 remaining life, 10 years $20,000 remaining life, 8 years Sived ment 2 7 Forest acquired 90% of Garden for $215,100 on July 1 Year 1, and accounts for its investment under the cost method. At that time, the shareholders' equity of Garden amounted to $176,000, the accumulated amortization was $96,000, and the assets of Garden were undervalued by the following amounts: Inventory Buildings Patents $13,000 $11,000 renaining life, 10 years $20,000 remaining life, 8 years . During Year 8. Forest reported net income of $42,000 and declared dividends of $26,000, whereas Garden reported net income of $64,000 and declared dividends of $51,000. . During Years 2 to 7 goodwill impairment losses totalled $2,000. An impairment test conducted in Year 8 indicated a further loss of $7,200 Forest sells goods to Garden on a regular basis at a gross profit of 30%. During Year 8, these sales totalled $150,100. On January 1, Year 8, the inventory of Garden contained goods purchased from Forest amounting to $18,100, while the December 31, Year 8, inventory contained goods purchased from Forest amounting to $22,100. . On August 1. Year 6, Garden sold land to Forest at a profit of $18,100. During Year 8, Forest sold one-quarter of the land to an unrelated company Forest's bonds have a par value of $100,000, pay interest annually on December 31 at a stated rate of 6%, and mature on December 31, Year 11. Forest Incurs an effective Interest cost of 8% on these bonds. They had a carrying amount of $93,376 on January 1, Year 8. On that date, Garden acquired $60,000 of these bonds on the open market at a cost of $57.968. Garden will earn an effective rate of return of 7% on them. Both companies use the effective-interest method to account for their bonds. The Year 8 income statements of the two companies show the following with respect to bond interest Interest expense Interest revenue Forest Garden $7,470 $4.058 Garden owes Forest $22,100 on open account on December 31, Year 8. Assume a 40% corporate tax rate and allocate bond gains (losses) between the two companies 1 Required: (6) Prepare the following statements Consolidated balance sheet (Amounts to be deducted should be indicated by a minus sign. Do not round Intermediate calculations and round your final answers to nearest dollar amount. The balance sheet total may vary due to rounding.) Forest Company Consolidated Balance Sheet December 31, Year Total assets Total liabilities and shareholders' equity 1 (9) Consolidated retained earnings statement (Input all values as positive numbers. Do not round intermediate calculations and round your final answers to nearest dollar amount. Omit $ sign in your response.) Forest Company Consolidated Retained Earnings Statement Year B Click to select Click to selec Click to select Click to select (b) Prepare the Year journal entries that would be made on the books of Forest of the equity method was used to account for the investment (if no entry is required for a transaction/event, select "No journal entry required in the first account field. Do not round Intermediate calculations and round your final answers to nearest dollar amount.) 1 (b) Prepare the Year 8 journal entries that would be made on the books of Forest if the equity method was used to account for the investment. (If no entry is required for a transaction/event, select "No journal entry required in the first account field. Do not round intermediate calculations and round your final answers to nearest dollar amount.) View transaction list Journal entry worksheet 1 2 3 To record 90% of adjusted subsidiary income. Note: Enter debits before credits General Journal Debit Credit Date Dec 31 Record entry Clear entry View general Journal Journal entry worksheet 1 1 2 3 3 To record 90% of Garden's dividend of 51,000. Note: Enter debits before credits. Date General Journal Dec 31 Debit Credit Record entry Clear entry View general journal Journal entry worksheet 1 1 2 3 To record the adjustments to parent's net income. Note: Enter debits before credits Date General Journal Debit Credit Dec 31 Record entry Clear entry View general journal