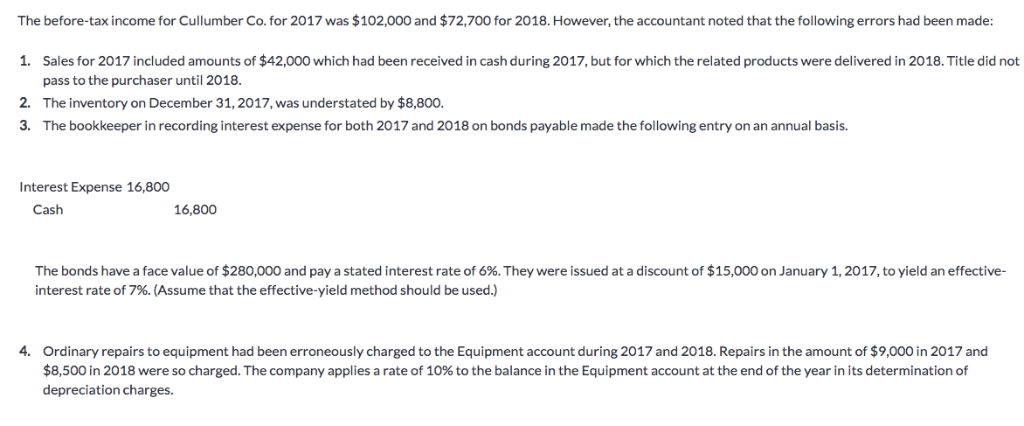

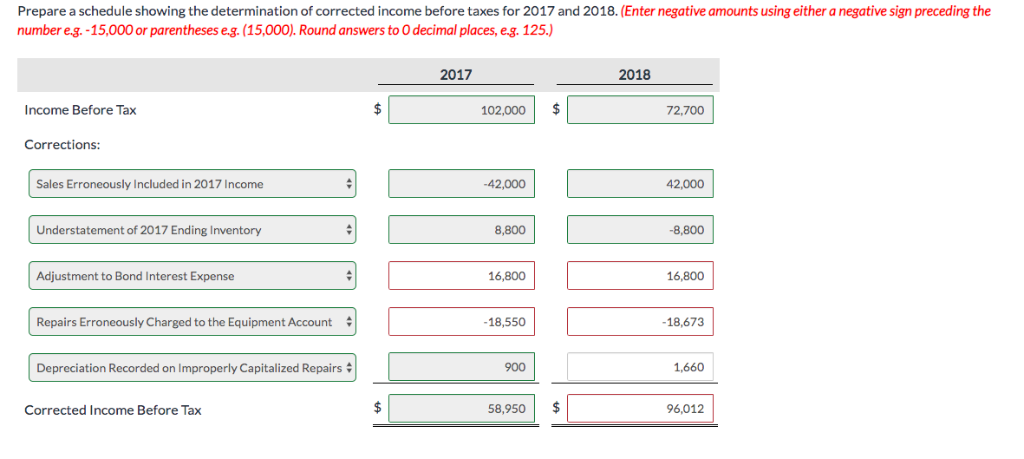

The before-tax income for Cullumber Co. for 2017 was $102,000 and $72,700 for 2018. However, the accountant noted that the following errors had been made: 1. Sales for 2017 included amounts of $42,000 which had been received in cash during 2017, but for which the related products were delivered in 2018. Title did not pass to the purchaser until 2018. 2. The inventory on December 31,2017, was understated by $8,800. 3. The bookkeeper in recording interest expense for both 2017 and 2018 on bonds payable made the following entry on an annual basis Interest Expense 16,800 Cash 16,800 The bonds have a face value of $280,000 and pay a stated interest rate of 6%. They were issued at a discount of $15,000 on January 1, 2017, to yield an effective- interest rate of 7%. (Assume that the effective-yield method should be used.) 4. Ordinary repairs to equipment had been erroneously charged to the Equipment account during 2017 and 2018. Repairs in the amount of $9,000 in 2017 and $8,500 in 2018 were so charged. The company applies a rate of 10% to the balance in the Equipment account at the end of the year in its determination of depreciation charges. Prepare a schedule showing the determination of corrected income before taxes for 2017 and 2018. (Enter negative amounts using either a negative sign preceding the number eg.-15,000 or parentheses e.g. (15,000). Round answers to O decimal places, e.g. 125.) 2017 2018 ncome Before Tax 102,000$ 72,700 Corrections: Sales Erroneously Included in 2017 Income 42,000 42,000 Understatement of 2017 Ending Inventory 8,800 8,800 Adjustment to Bond Interest Expense 16,800 16,800 Repairs Erroneously Charged to the Equipment Account # 18,550 18,673 Depreciation Recorded on Improperly Capitalized Repairs 900 1,660 Corrected Income Before Tax 58,950 96,012 The before-tax income for Cullumber Co. for 2017 was $102,000 and $72,700 for 2018. However, the accountant noted that the following errors had been made: 1. Sales for 2017 included amounts of $42,000 which had been received in cash during 2017, but for which the related products were delivered in 2018. Title did not pass to the purchaser until 2018. 2. The inventory on December 31,2017, was understated by $8,800. 3. The bookkeeper in recording interest expense for both 2017 and 2018 on bonds payable made the following entry on an annual basis Interest Expense 16,800 Cash 16,800 The bonds have a face value of $280,000 and pay a stated interest rate of 6%. They were issued at a discount of $15,000 on January 1, 2017, to yield an effective- interest rate of 7%. (Assume that the effective-yield method should be used.) 4. Ordinary repairs to equipment had been erroneously charged to the Equipment account during 2017 and 2018. Repairs in the amount of $9,000 in 2017 and $8,500 in 2018 were so charged. The company applies a rate of 10% to the balance in the Equipment account at the end of the year in its determination of depreciation charges. Prepare a schedule showing the determination of corrected income before taxes for 2017 and 2018. (Enter negative amounts using either a negative sign preceding the number eg.-15,000 or parentheses e.g. (15,000). Round answers to O decimal places, e.g. 125.) 2017 2018 ncome Before Tax 102,000$ 72,700 Corrections: Sales Erroneously Included in 2017 Income 42,000 42,000 Understatement of 2017 Ending Inventory 8,800 8,800 Adjustment to Bond Interest Expense 16,800 16,800 Repairs Erroneously Charged to the Equipment Account # 18,550 18,673 Depreciation Recorded on Improperly Capitalized Repairs 900 1,660 Corrected Income Before Tax 58,950 96,012