Answered step by step

Verified Expert Solution

Question

1 Approved Answer

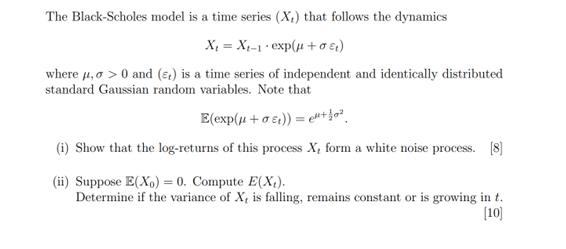

The Black-Scholes model is a time series (X) that follows the dynamics X =X-1 exp(+1) where ,0 and (e) is a time series of

The Black-Scholes model is a time series (X) that follows the dynamics X =X-1 exp(+1) where ,0 and (e) is a time series of independent and identically distributed standard Gaussian random variables. Note that E(exp(+)) =+ f (i) Show that the log-returns of this process X, form a white noise process. [8] (ii) Suppose E(X) = 0. Compute E(X). Determine if the variance of X, is falling, remains constant or is growing in t. [10]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Ten Projects In Applied Statistics

Authors: Peter McCullagh

1st Edition

3031142748, 978-3031142741