Answered step by step

Verified Expert Solution

Question

1 Approved Answer

the book value of liabilities is 675 million the book value of equity is 75 million The bank has decided to go with a short-duration

the book value of liabilities is 675 million

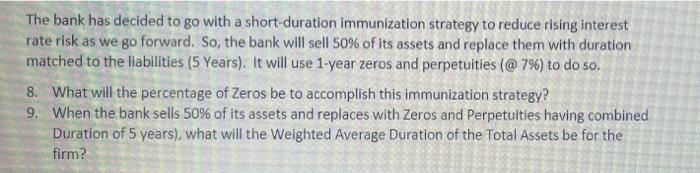

The bank has decided to go with a short-duration immunization strategy to reduce rising interest rate risk as we go forward. So, the bank will sell 50% of its assets and replace them with duration matched to the liabilities (5 Years). It will use 1-year zeros and perpetuities (@ 7%) to do so. 8. What will the percentage of Zeros be to accomplish this immunization strategy? 9. When the bank sells 50% of its assets and replaces with Zeros and Perpetuities having combined Duration of 5 years), what will the Weighted Average Duration of the Total Assets be for the firm? The bank has decided to go with a short-duration immunization strategy to reduce rising interest rate risk as we go forward. So, the bank will sell 50% of its assets and replace them with duration matched to the liabilities (5 Years). It will use 1-year zeros and perpetuities (@ 7%) to do so. 8. What will the percentage of Zeros be to accomplish this immunization strategy? 9. When the bank sells 50% of its assets and replaces with Zeros and Perpetuities having combined Duration of 5 years), what will the Weighted Average Duration of the Total Assets be for the firm the book value of equity is 75 million

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Options Trading For Beginners

Authors: Mike Hartley

1st Edition

979-8864514832