Question

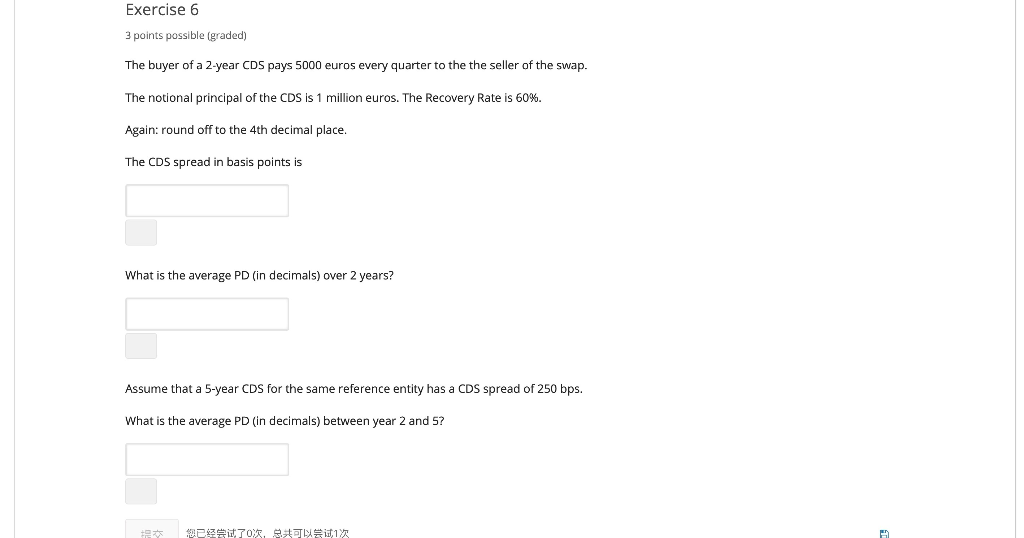

The buyer of a 2-year CDS pays 5000 euros every quarter to the seller of the swap. The notional principal of the CDS is 1

The buyer of a 2-year CDS pays 5000 euros every quarter to the seller of the swap.

The notional principal of the CDS is 1 million euros. The recovery Rate is 60%.

The CDS spread in basis points is:

What is the average PD (in dicimals) over 2 years:

Assume that 5-year CDS for the same reference entity has a CDS spread of 250 bps. What is the average PD (in decimals) between year 2 and 5.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting

Authors: Ray Garrison

12th Edition

B002ODFC0E