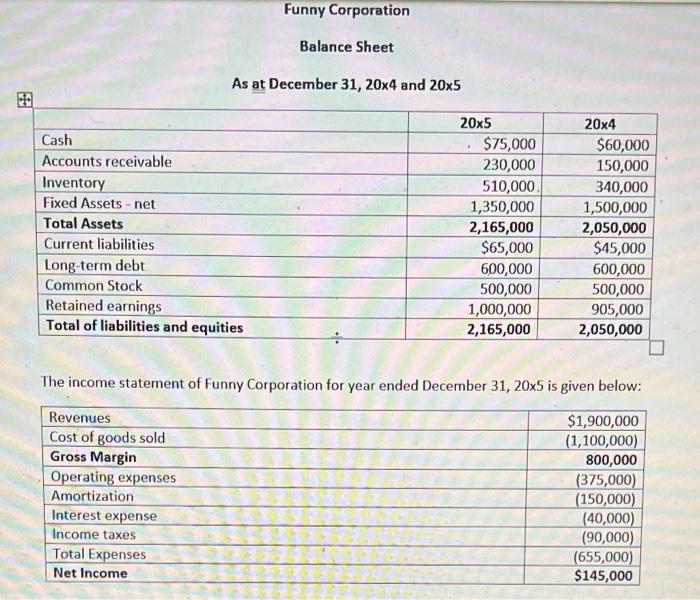

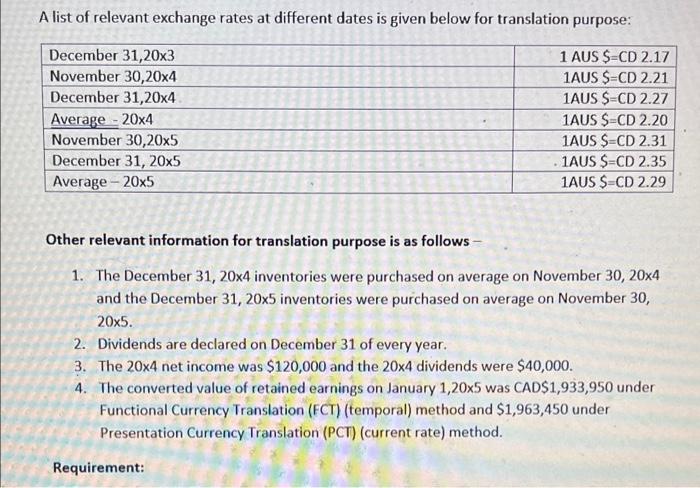

The Campbell Company of Canada purchased 100% of the shares of Funny Corporation of Australia on December 31, 20x3 for developing new markets for their products. It is a public company and operating business successfully for last five years. Funny Corporation sells the goods imported from Campbell Company. Campbell produces all goods for sale in Australia. Campbell Company also dictates the operational procedures of Funny Corporation. IAS 21 requires that financial statements of subsidiary are to be translated into the investor company's presentation currency before preparing consolidated financial statements. There are two major methods for translating the foreign operations under Canadian GAAP. After the adoption of IFRSs in 2011, there was no change in translation methods. IAS 21 also uses the similar approach for translating the financial statements of foreign operations. Funny Corporation prepares financial statenents in Australian dollar (AUSS). The financial statements for the Funny Corporation are as follows: Funny Corporation Balance Sheet As at December 31, 20x4 and 20x5 Cash Accounts receivable Inventory Fixed Assets - net Total Assets Current liabilities Long-term debt Common Stock Retained earnings Total of liabilities and equities 20x5 $75,000 230,000 510,000 1,350,000 2,165,000 $65,000 600,000 500,000 1,000,000 2,165,000 20x4 $60,000 150,000 340,000 1,500,000 2,050,000 $45,000 600,000 500,000 905,000 2,050,000 The income statement of Funny Corporation for year ended December 31, 20x5 is given below: Revenues Cost of goods sold Gross Margin Operating expenses Amortization Interest expense Income taxes Total Expenses Net Income $1,900,000 (1,100,000) 800,000 (375,000) (150,000) (40,000) (90,000) (655,000) $145,000 IAS 21 establishes accounting standards for the translation of the financial statements of a foreign operation for use by a reporting enterprise (a Canadian investor) A foreign operation is viewed as either integrated or self-sustaining for translation purposes, depending on whether the functional currency of the foreign entity is the same as or different from the functional currency of the Canadian reporting entity. IAS 21 defines functional currency as the currency of primary economic environment in which the entity operates. The primary economic environment is normally the one in which the entity primarily generates and expends cash. There are many indicators for determining the functional currency for a foreign operation. When the indicators are mixed and the functional currency is not obvious, management uses its professional judgement to determine the functional currency. To translate the foreign operation's financial statement into presentation currency of investor, different exchange rates are used for different items under different methods of translation. A list of relevant exchange rates at different dates is given below for translation purpose: A list of relevant exchange rates at different dates is given below for translation purpose: December 31,20x3 November 30,20x4 December 31,20x4 Average - 20x4 November 30,20x5 December 31, 20x5 Average - 2005 1 AUS SECD 2.17 1AUS S=CD 2.21 1AUS S=CD 2.27 1AUS S=CD 2.20 1AUS SECD 2.31 1AUS S=CD 2.35 1AUS S=CD 2.29 Other relevant information for translation purpose is as follows - 1. The December 31, 20x4 inventories were purchased on average on November 30, 20x4 and the December 31, 20x5 inventories were purchased on average on November 30, 20x5. 2. Dividends are declared on December 31 of every year. 3. The 20x4 net income was $120,000 and the 20x4 dividends were $40,000. 4. The converted value of retained earnings on January 1,20x5 was CAD$1,933,950 under Functional Currency Translation (FCT) (temporal) method and $1,963,450 under Presentation Currency Translation (PCT) (current rate) method. Requirement: 1. What difference does it make whether the foreign operation's functional currency is the same or different than the parent's presentation currency? What method of translation should be used for each? (3) 2. Based on the information provided, determine the type of foreign subsidiary for translation purpose. (Give reason for your selection of a specific type). (2) 3. Prepare a translated income statement for the year ended December 31,20x5_and (7) 4. Prepare a translated balance sheet as at December 31, 20x5. (6)