Question

The CAPM Method for the expected return I have given you monthly returns for the stock market, Google, and the three-month treasury (risk-free rate). 1)

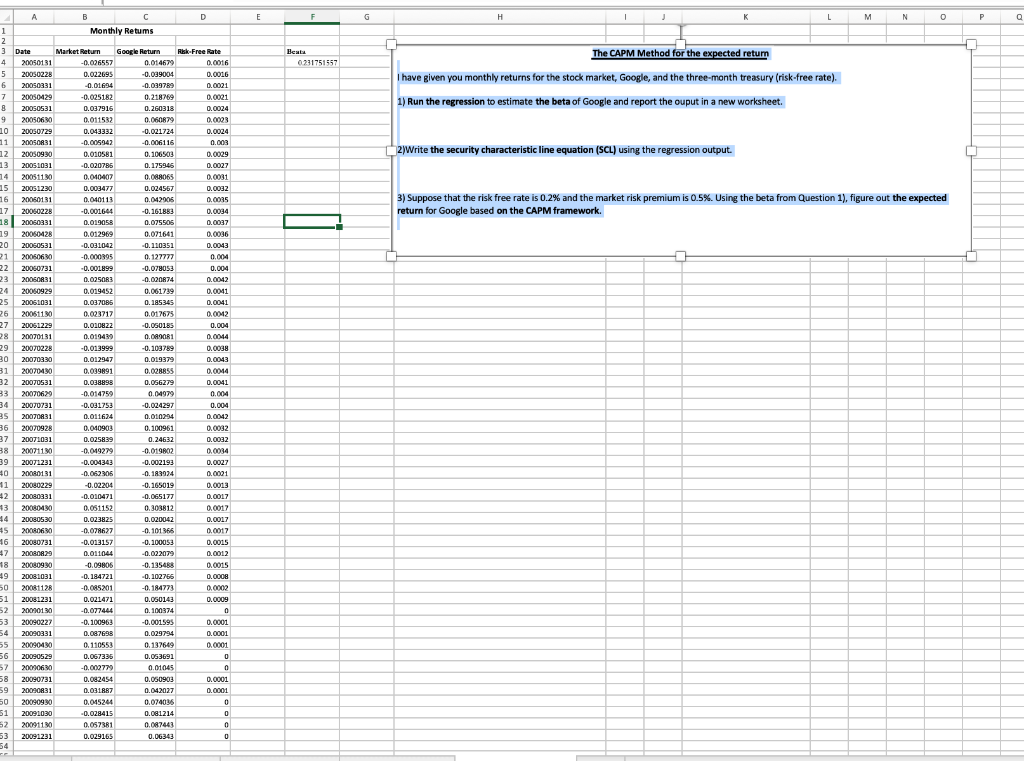

The CAPM Method for the expected return

I have given you monthly returns for the stock market, Google, and the three-month treasury (risk-free rate).

1) Run the regression to estimate the beta of Google and report the out put in a new worksheet.

put in a new worksheet.

2)Write the security characteristic line equation (SCL) using the regression output.

3) Suppose that the risk free rate is 0.2% and the market risk premium is 0.5%. Using the beta from Question 1), figure out the expected return for Google based on the CAPM framework.

L M N O P Q Monthly Retums 3 The CAPM Method for the expected retum 0221751557 I have given you monthly returns for the stock market, Google, and the three-month treasury (risk-free rate). 1) Run the regression to estimate the beta of Google and report the ouput in a new worksheet. 2) Write the security characteristic line equation (SCL) using the regression output. 3) Suppose that the risk free rate is 0.2% and the market risk premium is 0.5%. Using the beta from Question 1), figure out the expected return for Google based on the CAPM framework. NINS Date Market Return Google Return Risk-Free Rate 20050131 -0.006557 0.014679 0.0016 20080225 0.022695 -0.039004 0.0016 20050331 -0.01694 -0.039789 0.0021 20050429 -0.025182 0.218769 0.0021 20050531 0.037915 0.260318 0.0024 0.011532 0.060879 0.0023 20050729 0.043332 -0.021724 0.0024 -0.006116 0.003 20050930 0.010581 0.106503 0.0029 20051031 -0.020786 0.175945 0.0027 20051130 0.010407 0.088065 0.0031 20051230 0.003477 0.024567 0.0032 20050131 0.040113 0.042005 0.0035 20050226 -0.001664 -0.16188 0.0034 0.019058 0.0037 0.012966 0.071661 0.0036 20050531 -0.03.1042 -0.110351 0.0043 20050630 -0.000995 0.127777 0.004 20050731 -0.001899 -0.078053 0.004 0.0250R3 -0.020874 0.0042 20030929 0.019452 0.061739 0.0041 0.15345 0.0041 2005110 0.023717 0.017675 00012 20051229 0.010822 -0.050185 0,004 20070131 0.019439 0. 001 0.0044 20070228 -0.013999 -0.103789 20070330 0.012947 0.019379 0.0043 200704130 0.039891 0.028855 0.00114 20070531 0.038995 0.066279 0.0041 20070629 -0.014759 0.04979 0.004 20070731 -0.031753 -0.024297 0.004 20070831 0.011624 0.010294 0.0042 20070928 0.040903 0.100961 0.0032 20071031 0.025839 0.24632 0.0032 200711% -0.019279 -0.019802 0.0034 20071221 -0.004343 -0.002193 0.0027 20020131 -0.062305 -0.183924 0.0001 20080229 -0.02204 -0.165019 0.0013 20080331 -0.010471 -0.065177 0.0017 20080 0.051152 0.303812 0.0017 20080530 0.023825 0.020042 0.0017 20080680 -0.078627 -0.101366 0.0017 20080731 -0.013157 -0.100053 0.0015 20080829 0.011044 -0.022079 0.0012 20080930 -0.09806 -0.135488 0.0015 20081031 -0.184721 -0.102766 0.0008 20081128 -0.005201 -0.184773 20081231 0.021471 0.060143 0.0009 20070130 -0.077444 0.100374 20090227 -0.00159 0.0001 20090331 0.087698 0.029794 0.0001 20092010 0.110553 0.137649 0.0001 20070529 0.067335 0.033691 20010630 -0.000779 0.01045 20090731 0.082454 0.050903 0.0001 0.031887 0.042027 0.0001 20090930 0.04524 0.074095 20091030 -0.028415 0.001214 20091130 0.057381 0.087443 20091231 0.029155 0.06343 0.0002 0.100963 Na L M N O P Q Monthly Retums 3 The CAPM Method for the expected retum 0221751557 I have given you monthly returns for the stock market, Google, and the three-month treasury (risk-free rate). 1) Run the regression to estimate the beta of Google and report the ouput in a new worksheet. 2) Write the security characteristic line equation (SCL) using the regression output. 3) Suppose that the risk free rate is 0.2% and the market risk premium is 0.5%. Using the beta from Question 1), figure out the expected return for Google based on the CAPM framework. NINS Date Market Return Google Return Risk-Free Rate 20050131 -0.006557 0.014679 0.0016 20080225 0.022695 -0.039004 0.0016 20050331 -0.01694 -0.039789 0.0021 20050429 -0.025182 0.218769 0.0021 20050531 0.037915 0.260318 0.0024 0.011532 0.060879 0.0023 20050729 0.043332 -0.021724 0.0024 -0.006116 0.003 20050930 0.010581 0.106503 0.0029 20051031 -0.020786 0.175945 0.0027 20051130 0.010407 0.088065 0.0031 20051230 0.003477 0.024567 0.0032 20050131 0.040113 0.042005 0.0035 20050226 -0.001664 -0.16188 0.0034 0.019058 0.0037 0.012966 0.071661 0.0036 20050531 -0.03.1042 -0.110351 0.0043 20050630 -0.000995 0.127777 0.004 20050731 -0.001899 -0.078053 0.004 0.0250R3 -0.020874 0.0042 20030929 0.019452 0.061739 0.0041 0.15345 0.0041 2005110 0.023717 0.017675 00012 20051229 0.010822 -0.050185 0,004 20070131 0.019439 0. 001 0.0044 20070228 -0.013999 -0.103789 20070330 0.012947 0.019379 0.0043 200704130 0.039891 0.028855 0.00114 20070531 0.038995 0.066279 0.0041 20070629 -0.014759 0.04979 0.004 20070731 -0.031753 -0.024297 0.004 20070831 0.011624 0.010294 0.0042 20070928 0.040903 0.100961 0.0032 20071031 0.025839 0.24632 0.0032 200711% -0.019279 -0.019802 0.0034 20071221 -0.004343 -0.002193 0.0027 20020131 -0.062305 -0.183924 0.0001 20080229 -0.02204 -0.165019 0.0013 20080331 -0.010471 -0.065177 0.0017 20080 0.051152 0.303812 0.0017 20080530 0.023825 0.020042 0.0017 20080680 -0.078627 -0.101366 0.0017 20080731 -0.013157 -0.100053 0.0015 20080829 0.011044 -0.022079 0.0012 20080930 -0.09806 -0.135488 0.0015 20081031 -0.184721 -0.102766 0.0008 20081128 -0.005201 -0.184773 20081231 0.021471 0.060143 0.0009 20070130 -0.077444 0.100374 20090227 -0.00159 0.0001 20090331 0.087698 0.029794 0.0001 20092010 0.110553 0.137649 0.0001 20070529 0.067335 0.033691 20010630 -0.000779 0.01045 20090731 0.082454 0.050903 0.0001 0.031887 0.042027 0.0001 20090930 0.04524 0.074095 20091030 -0.028415 0.001214 20091130 0.057381 0.087443 20091231 0.029155 0.06343 0.0002 0.100963 Na

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance At Work

Authors: Valérie Boussard

1st Edition

113820403X, 978-1138204034