Question: The case introduces a framework for the analysis that supports managerial decisions on how to comply with emissions reductions regulation, in this case, the 1990

The case introduces a framework for the analysis that supports managerial decisions on how to comply with emissions reductions regulation, in this case, the 1990 Clean Air Act amendments.

1.The company has several options available for complying with the new law. The cost of these options is derived either from investments required to reduce emissions internally in the company, or from purchasing allowances.

Estimate the cost of pursuing the following options:

The company installs scrubbers in 2000.

The company switches to low-sulfur coal in 1996.

The company switches to low-sulfur coal in 2000 (Phase II).

The company switches to low-sulfur coal in 1996, and installs scrubbers in 2000.

The company switches to low-sulfur coal in 2000, and installs scrubbers in 2000.

2.2. What should the company do?

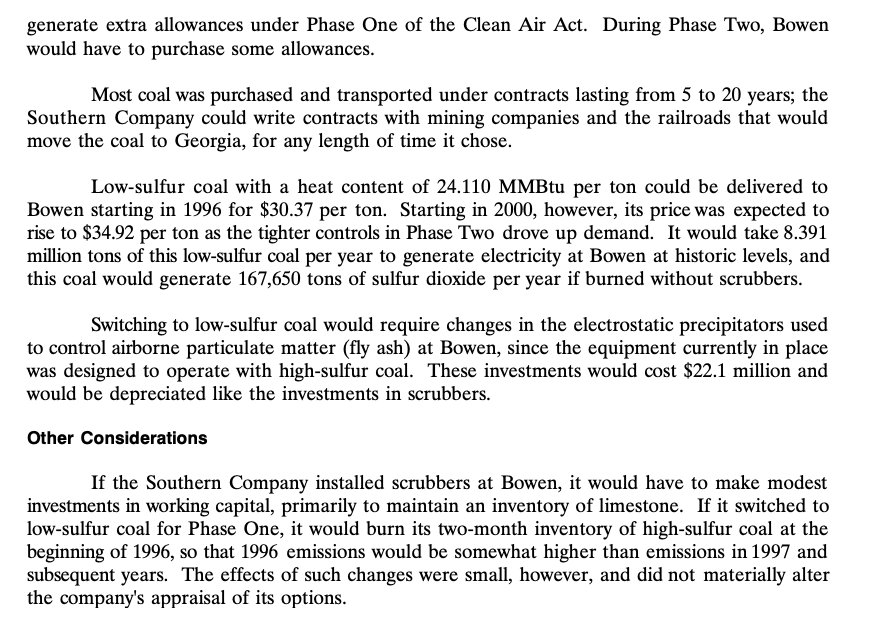

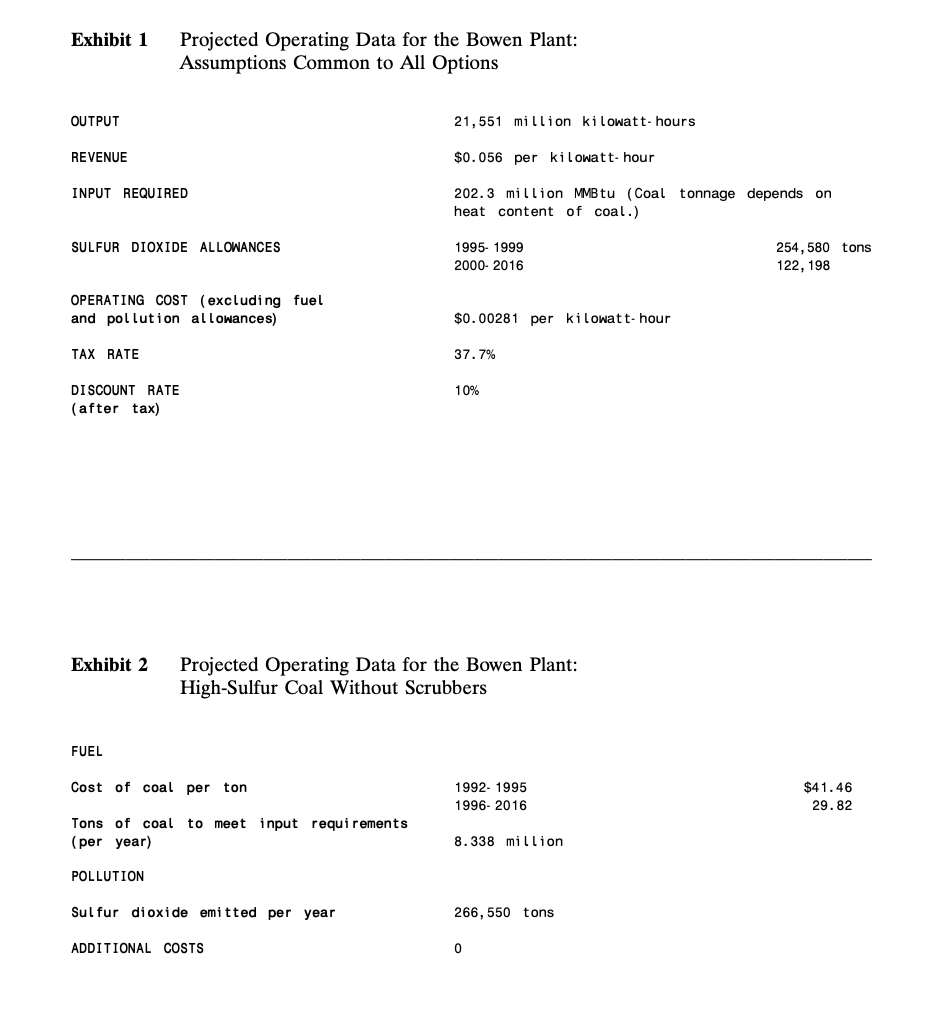

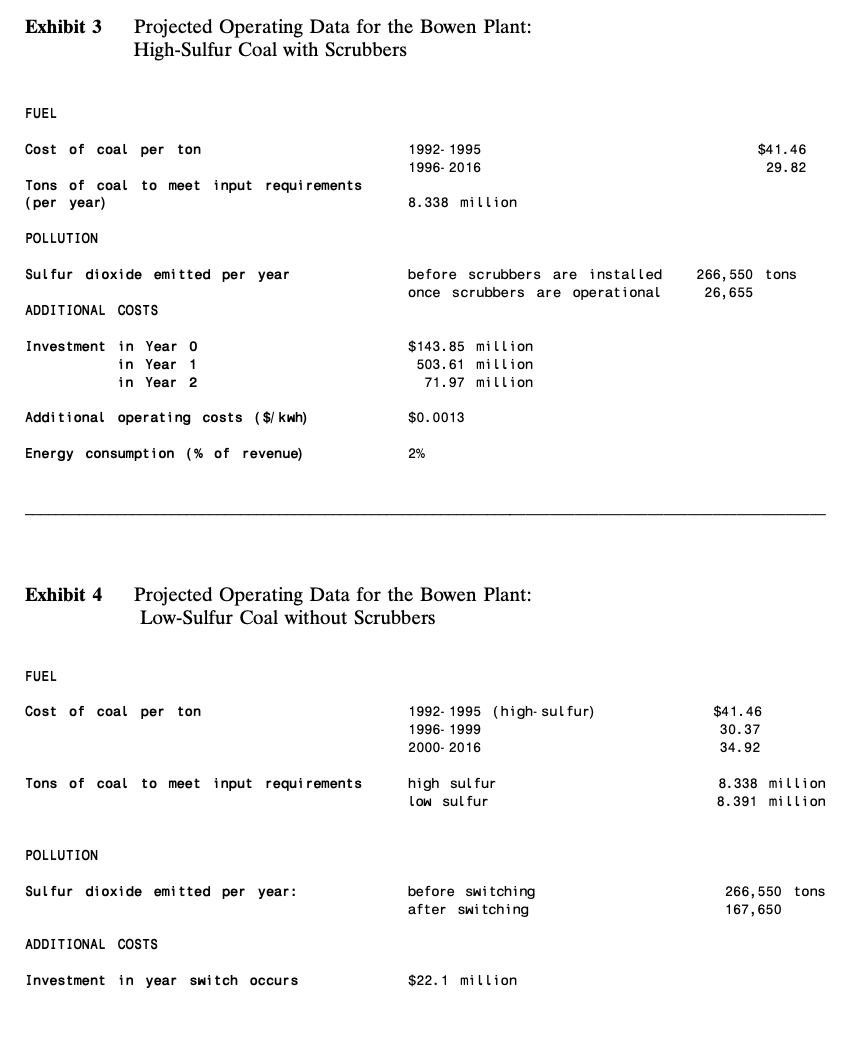

Early in 1992, managers at the Southern Company were reexamining their strategy for complying with the acid rain provisions of the 1990 amendments to the Clean Air Act. The Southern Company was a holding company; its operating units were electric utilities in Georgia, Alabama, Mississippi, and Florida. The largest Southern subsidiaries, Georgia Power and Alabama Power, provided most of the electricity in their respective states. Dozens of Southern Company executives had worked on compliance strategies since the Clean Air Act's passage in November 1990, but the time for analysis was just about over. Because of long lead times in installing pollution-control equipment, the final decisions on compliance strategy would have to be made in 1992 in order to meet the Act's 1995 effective date. The choices that the company faced at Georgia Power's Bowen coal-fired plant were representative of the dilemmas the Clean Air Act posed for the Southern Company as a whole. The Bowen plant sat on the banks of the Etowah River near Taylorsville, Georgia, northwest of the city of Atlanta. Completed in 1975, it was capable, when all four of its generators were running at capacity, of producing enough power to serve the residential, commercial, and industrial demands of 1 million people. The Bowen plant was an unusually large, but otherwise fairly typical, coal-fired steam electric plant. Coal was burned in massive vessels. Steam, traveling through pipes that ran through these vessels, was heated by the energy from the burning coal. Adjacent turbines converted the energy in the steam to mechanical energy, which was then converted to electrical energy in the plant's generators. Large coal-fired plants like Bowen had high fixed costs but relatively low variable costs and were designed to operate continuously. Utilities used them for baseload generation, supplementing the energy from the coal plants with power from oil- or gasfired plants to meet peak demands. Running the Bowen plant was an operation of vast scale. Hundreds of railroad cars, carrying coal from southeastern Kentucky, arrived at the plant each day, contributing to a pile of inventory that weighed over 1 million tons. During 1990, Bowen's generators consumed 8.338 million tons of coal (952 tons of coal every hour) and generated 21,551 million kilowatt-hours of electricity. The value of this electricity varied substantially across markets, but in 1990 the Southern Company realized an average of 5.6 cents per kilowatt-hour in revenues. Also during 1990, over 30 tons of sulfur dioxide left the stacks of the Bowen plant each hour. This pollutant was an important precursor of acid deposition, or acid rain, which had been implicated in damage to lakes, forest ecosystems, and manmade materials like metals and paints. New legislation aimed at controlling acid rain, passed by Congress and signed by President Bush in November 1990, would regulate these emissions starting in 1995. Most previous regulations for air pollution control had specified a particular quantity of pollution that a facility could emit. A firm faced fines or other sanctions if its emissions exceeded the permitted level, but it had no incentive to reduce its emissions below the level specified in the permit. The new acid rain law, by contrast, allowed firms to choose their own emissions levels. They would be granted allowances to emit a certain amount of sulfur dioxide, based on the amount of electricity they had generated in the past. Starting in 1995 (in "Phase One" of the law), each of about 100 large coal-fired utility plants across the country, including Bowen, would receive allowances to emit 2.5 pounds of sulfur dioxide per million British thermal units (MMBtu) of coal consumed. In the year 2000 ("Phase Two"), all coal-fired utility plants, including those regulated in Phase One, would get allowances worth 1.2 pounds per MMBtu of coal. If they wished, utilities could reduce their emissions below the amount for which they had been given allowances and sell the extra allowances to other utilities. Alternatively, they could purchase additional allowances from other firms, which would permit them to release larger quantities of sulfur dioxide. Compared to other plants that would be regulated in Phase One, Bowen was fairly clean; many other utility plants, including some in the Southern Company system, were emitting sulfur dioxide in quantities up to two times higher than Phase One levels. Nevertheless, Bowen would have to reduce its emissions by 1995 , or purchase allowances, in order to comply with the law. Further reductions or increased purchases of allowances would be necessary beginning in the year 2000 . The Clean Air Act amendments specified the quantity of allowances Bowen would receive. The plant would receive allowances for 254,580 tons of sulfur dioxide in each of the five years beginning in 1995. Starting in the year 2000, it would receive allowances worth 122,198 tons per year. There were several options for complying with the new law. First, the company could continue to operate Bowen as it had in the past, burning high-sulfur Kentucky coal without scrubbing the exhaust gases. If it did, its emissions would exceed the amounts for which it would receive allowances. Each year beginning in 1995, Bowen would purchase allowances from other Southern Company plants or on the open market to make up the difference. Second, the company could install scrubbers at the Bowen plant that would remove sulfur dioxide from the exhaust gases of the generators. The scrubbers could be installed from 1992 to 1994 so they would be on line during Phase One; in that case, Bowen would generate excess allowances that could be sold to other utilities or to other Southern Company plants. Alternatively, the company could delay the installation of the scrubbers until 1997 to 1999 , in which case they would begin working in the year 2000; in that case, Bowen would generate excess allowances starting in 2000, but during 1995 through 1999 it would need to buy allowances from other plants. The company's last option was to switch the Bowen plant to low-sulfur coal from Kentucky or West Virginia. This strategy would bring Bowen's emissions below the amount of its Phase One permits. In Phase Two, the Bowen plant would need to buy allowances. (Nothing prevented the Southern Company from switching fuels and also installing scrubbers, but this option made little sense economically. If a plant burned low-sulfur coal, the gases leaving its boilers would be sufficiently low in sulfur that scrubbers could not remove enough additional sulfur to pay for themselves.) Under any of the options, the Bowen plant would continue to generate electricity at its 1990 levels through the year 2016. In 2016, Bowen was likely to be retired as new, more efficient plants came on stream, and its salvage value would be negligible. Company planners expected the price of electricity to remain constant during the period Bowen was in operation. They also figured that operating costs exclusive of fuel and pollutioncontrol expenditures, which had averaged 0.00281 dollars per kilowatt-hour in recent years, would stay about the same until the plant was retired. The prices the Southern Company could charge for its electricity in Georgia were determined by the Public Service Commission, a body of five officials elected statewide. The utility customarily applied for rate increases to recover the costs of new construction or to pass on increases in operating costs. The Southern Company's government relations personnel were uncertain whether the commission would approve rate increases to cover the total costs of compliance with the Clean Air Act. The commission might force the company's shareholders to bear some of the costs of compliance rather than passing them on to its ratepayers. A second possibility was that the company might be allowed to recover its costs only if it could show that it had complied in the least-cost manner. In either case, the company executives felt that they ought to search for the cost-minimizing method of complying with the Act. Numerous government agencies and private firms had developed predictions of the prices of allowances in Phase One and Phase Two. As a working estimate, company planners felt that the price of allowances would probably be $250 per ton of sulfur dioxide in 1995 , the first year of Phase One, and that the price would rise at 10% per year through the year 2010. Thereafter, the allowances were expected to stay at their 2010 price. Allowances could be bought or sold on the open market, and a multiplant firm like the Southern Company could also move allowances from one of its plants to another in an internal transaction. From an economic standpoint, it was irrelevant whether allowances were traded within the firm or externally, since the value of an allowance-and hence the appropriate internal transfer price-would be determined in the external market. In Georgia, the Southern Company paid federal and state income taxes at a combined effective rate of 37.7%. The company customarily used an after-tax discount rate of 10% in evaluating investment opportunities. Option 1: Burn High-Sulfur Coal without Scrubbers; Purchase Allowances Aside from capital costs, costs of fuel were the largest single expense at Bowen. Coals varied widely both in delivered price per ton and in heat content per pound, so prices were usually expressed in dollars per ton and in dollars per MMBtu. The high-sulfur Kentucky coal burned at Bowen cost, on average, $41.46 per ton delivered to the plant. Starting in 1996 , the price was expected to fall to $29.82 per ton, delivered. Bowen's generators required coal with a total heat content of 202.3 million MMBtu; the heat content of the coal was 24.262 MMBtu per ton, so that Bowen needed 202,300,000/24.262 or 8.338 million tons of that sort of coal per year. The coal currently burned at Bowen contained an average of 1.6% sulfur by weight. Burning 8.338 million tons of this coal without installing additional pollution-control equipment would generate 266,550 tons of sulfur dioxide emissions. Option 2: Burn High-Sulfur Coal with Scrubbers; Sell Allowances In order to reduce emissions of sulfur dioxide at Bowen, the Southern Company could install wet-limestone flue gas desulfurization (FGD) equipment, commonly known as scrubbers. The gases from the generator already went through one pollution-control device called an electrostatic precipitator before release to the atmosphere; the precipitator eliminated most of the ash and particles from the gas. If scrubbers were installed, the gases, after leaving the precipitator, would enter another large chamber where they would be mixed with a slurry of water and limestone. The limestone would react with the sulfur dioxide, forming a sludge that could be landfilled. The gases, with 90% of the sulfur dioxide removed, would then be vented to the air. Scrubbers were enormous, as large as the generators themselves; they were also expensive. To install them at Bowen in time to reduce emissions in 1995 would require outlays of $143.85 million in 1992, $503.61 million in 1993, and $71.97 million in 1994. Once installed, the scrubbers would add 0.13 cents per kilowatt-hour to the operating costs of the Bowen plant, primarily for the purchase of limestone and the disposal of the sludge. They would also consume 2% of the total amount of electricity generated at the plant once they were turned on. This would, in effect, reduce revenues by 2%. The capital costs of the scrubbers could be depreciated over 20 years beginning in the first year of operation (i.e., beginning in 1995 if the scrubbers were installed to meet Phase One deadlines). In each of the first 5 years of the depreciation schedule, 14% of the capital costs could be depreciated; for the next 15 years, the company could depreciate 2% of the capital costs. These capital costs would include the capitalized interest (at 10% per year) on the scrubbers during the period when the devices were being installed. The scrubbers were not expected to have an appreciable salvage value. The Southern Company could also wait to begin installing the scrubbers until 1997, bringing them on line in time for the more stringent Phase Two requirements. This strategy would delay the capital outlays of installing the scrubbers by five years, but in Phase One Bowen would have to buy allowances or burn lower-sulfur coal. Option 3: Burn Low-Sulfur Coal Instead of installing the FGD equipment, the Southern Company could switch to lowsulfur coal from Kentucky or West Virginia. If Bowen chose to switch to this type of coal, it would wait until the beginning of 1996 to do so, since the utility's take-or-pay contract with its current supplier would expire at the end of 1995 . The low-sulfur coal contained 1% sulfur by weight. It cost less than the company was currently paying for the coal burned at Bowen, but its cost was greater than the expected 1996 cost of high-sulfur coal. Its use, without scrubbers, would generate extra allowances under Phase One of the Clean Air Act. During Phase Two, Bowen would have to purchase some allowances. Most coal was purchased and transported under contracts lasting from 5 to 20 years; the Southern Company could write contracts with mining companies and the railroads that would move the coal to Georgia, for any length of time it chose. Low-sulfur coal with a heat content of 24.110MMBtu per ton could be delivered to Bowen starting in 1996 for $30.37 per ton. Starting in 2000, however, its price was expected to rise to $34.92 per ton as the tighter controls in Phase Two drove up demand. It would take 8.391 million tons of this low-sulfur coal per year to generate electricity at Bowen at historic levels, and this coal would generate 167,650 tons of sulfur dioxide per year if burned without scrubbers. Switching to low-sulfur coal would require changes in the electrostatic precipitators used to control airborne particulate matter (fly ash) at Bowen, since the equipment currently in place was designed to operate with high-sulfur coal. These investments would cost $22.1 million and would be depreciated like the investments in scrubbers. Other Considerations If the Southern Company installed scrubbers at Bowen, it would have to make modest investments in working capital, primarily to maintain an inventory of limestone. If it switched to low-sulfur coal for Phase One, it would burn its two-month inventory of high-sulfur coal at the beginning of 1996, so that 1996 emissions would be somewhat higher than emissions in 1997 and subsequent years. The effects of such changes were small, however, and did not materially alter the company's appraisal of its options. Exhibit 1 Projected Operating Data for the Bowen Plant: Assumptions Common to All Options OUTPUT REVENUE $0.056 per kilowat t-hour INPUT REQUIRED 202. 3 million MMBtu (Coal tonnage depends on heat content of coal.) SULFUR DIOXIDE ALLOWANCES 1995199920002016254,580122,198 OPERATING COST (excluding fuel and pollution allowances) $0.00281 per kilowatt-hour TAX RATE 37.7% DISCOUNT RATE 10% (after tax) Exhibit 2 Projected Operating Data for the Bowen Plant: High-Sulfur Coal Without Scrubbers FUEL Cost of coal per ton 1992199519962016$41.4629.82 Tons of coal to meet input requirements (per year) 8. 338million POLLUTION Sulfur dioxide emitted per year 266,550 tons ADDITIONAL COSTS 0 Exhibit 3 Projected Operating Data for the Bowen Plant: High-Sulfur Coal with Scrubbers EIICI Exhibit 4 Projected Operating Data for the Bowen Plant: Low-Sulfur Coal without Scrubbers Early in 1992, managers at the Southern Company were reexamining their strategy for complying with the acid rain provisions of the 1990 amendments to the Clean Air Act. The Southern Company was a holding company; its operating units were electric utilities in Georgia, Alabama, Mississippi, and Florida. The largest Southern subsidiaries, Georgia Power and Alabama Power, provided most of the electricity in their respective states. Dozens of Southern Company executives had worked on compliance strategies since the Clean Air Act's passage in November 1990, but the time for analysis was just about over. Because of long lead times in installing pollution-control equipment, the final decisions on compliance strategy would have to be made in 1992 in order to meet the Act's 1995 effective date. The choices that the company faced at Georgia Power's Bowen coal-fired plant were representative of the dilemmas the Clean Air Act posed for the Southern Company as a whole. The Bowen plant sat on the banks of the Etowah River near Taylorsville, Georgia, northwest of the city of Atlanta. Completed in 1975, it was capable, when all four of its generators were running at capacity, of producing enough power to serve the residential, commercial, and industrial demands of 1 million people. The Bowen plant was an unusually large, but otherwise fairly typical, coal-fired steam electric plant. Coal was burned in massive vessels. Steam, traveling through pipes that ran through these vessels, was heated by the energy from the burning coal. Adjacent turbines converted the energy in the steam to mechanical energy, which was then converted to electrical energy in the plant's generators. Large coal-fired plants like Bowen had high fixed costs but relatively low variable costs and were designed to operate continuously. Utilities used them for baseload generation, supplementing the energy from the coal plants with power from oil- or gasfired plants to meet peak demands. Running the Bowen plant was an operation of vast scale. Hundreds of railroad cars, carrying coal from southeastern Kentucky, arrived at the plant each day, contributing to a pile of inventory that weighed over 1 million tons. During 1990, Bowen's generators consumed 8.338 million tons of coal (952 tons of coal every hour) and generated 21,551 million kilowatt-hours of electricity. The value of this electricity varied substantially across markets, but in 1990 the Southern Company realized an average of 5.6 cents per kilowatt-hour in revenues. Also during 1990, over 30 tons of sulfur dioxide left the stacks of the Bowen plant each hour. This pollutant was an important precursor of acid deposition, or acid rain, which had been implicated in damage to lakes, forest ecosystems, and manmade materials like metals and paints. New legislation aimed at controlling acid rain, passed by Congress and signed by President Bush in November 1990, would regulate these emissions starting in 1995. Most previous regulations for air pollution control had specified a particular quantity of pollution that a facility could emit. A firm faced fines or other sanctions if its emissions exceeded the permitted level, but it had no incentive to reduce its emissions below the level specified in the permit. The new acid rain law, by contrast, allowed firms to choose their own emissions levels. They would be granted allowances to emit a certain amount of sulfur dioxide, based on the amount of electricity they had generated in the past. Starting in 1995 (in "Phase One" of the law), each of about 100 large coal-fired utility plants across the country, including Bowen, would receive allowances to emit 2.5 pounds of sulfur dioxide per million British thermal units (MMBtu) of coal consumed. In the year 2000 ("Phase Two"), all coal-fired utility plants, including those regulated in Phase One, would get allowances worth 1.2 pounds per MMBtu of coal. If they wished, utilities could reduce their emissions below the amount for which they had been given allowances and sell the extra allowances to other utilities. Alternatively, they could purchase additional allowances from other firms, which would permit them to release larger quantities of sulfur dioxide. Compared to other plants that would be regulated in Phase One, Bowen was fairly clean; many other utility plants, including some in the Southern Company system, were emitting sulfur dioxide in quantities up to two times higher than Phase One levels. Nevertheless, Bowen would have to reduce its emissions by 1995 , or purchase allowances, in order to comply with the law. Further reductions or increased purchases of allowances would be necessary beginning in the year 2000 . The Clean Air Act amendments specified the quantity of allowances Bowen would receive. The plant would receive allowances for 254,580 tons of sulfur dioxide in each of the five years beginning in 1995. Starting in the year 2000, it would receive allowances worth 122,198 tons per year. There were several options for complying with the new law. First, the company could continue to operate Bowen as it had in the past, burning high-sulfur Kentucky coal without scrubbing the exhaust gases. If it did, its emissions would exceed the amounts for which it would receive allowances. Each year beginning in 1995, Bowen would purchase allowances from other Southern Company plants or on the open market to make up the difference. Second, the company could install scrubbers at the Bowen plant that would remove sulfur dioxide from the exhaust gases of the generators. The scrubbers could be installed from 1992 to 1994 so they would be on line during Phase One; in that case, Bowen would generate excess allowances that could be sold to other utilities or to other Southern Company plants. Alternatively, the company could delay the installation of the scrubbers until 1997 to 1999 , in which case they would begin working in the year 2000; in that case, Bowen would generate excess allowances starting in 2000, but during 1995 through 1999 it would need to buy allowances from other plants. The company's last option was to switch the Bowen plant to low-sulfur coal from Kentucky or West Virginia. This strategy would bring Bowen's emissions below the amount of its Phase One permits. In Phase Two, the Bowen plant would need to buy allowances. (Nothing prevented the Southern Company from switching fuels and also installing scrubbers, but this option made little sense economically. If a plant burned low-sulfur coal, the gases leaving its boilers would be sufficiently low in sulfur that scrubbers could not remove enough additional sulfur to pay for themselves.) Under any of the options, the Bowen plant would continue to generate electricity at its 1990 levels through the year 2016. In 2016, Bowen was likely to be retired as new, more efficient plants came on stream, and its salvage value would be negligible. Company planners expected the price of electricity to remain constant during the period Bowen was in operation. They also figured that operating costs exclusive of fuel and pollutioncontrol expenditures, which had averaged 0.00281 dollars per kilowatt-hour in recent years, would stay about the same until the plant was retired. The prices the Southern Company could charge for its electricity in Georgia were determined by the Public Service Commission, a body of five officials elected statewide. The utility customarily applied for rate increases to recover the costs of new construction or to pass on increases in operating costs. The Southern Company's government relations personnel were uncertain whether the commission would approve rate increases to cover the total costs of compliance with the Clean Air Act. The commission might force the company's shareholders to bear some of the costs of compliance rather than passing them on to its ratepayers. A second possibility was that the company might be allowed to recover its costs only if it could show that it had complied in the least-cost manner. In either case, the company executives felt that they ought to search for the cost-minimizing method of complying with the Act. Numerous government agencies and private firms had developed predictions of the prices of allowances in Phase One and Phase Two. As a working estimate, company planners felt that the price of allowances would probably be $250 per ton of sulfur dioxide in 1995 , the first year of Phase One, and that the price would rise at 10% per year through the year 2010. Thereafter, the allowances were expected to stay at their 2010 price. Allowances could be bought or sold on the open market, and a multiplant firm like the Southern Company could also move allowances from one of its plants to another in an internal transaction. From an economic standpoint, it was irrelevant whether allowances were traded within the firm or externally, since the value of an allowance-and hence the appropriate internal transfer price-would be determined in the external market. In Georgia, the Southern Company paid federal and state income taxes at a combined effective rate of 37.7%. The company customarily used an after-tax discount rate of 10% in evaluating investment opportunities. Option 1: Burn High-Sulfur Coal without Scrubbers; Purchase Allowances Aside from capital costs, costs of fuel were the largest single expense at Bowen. Coals varied widely both in delivered price per ton and in heat content per pound, so prices were usually expressed in dollars per ton and in dollars per MMBtu. The high-sulfur Kentucky coal burned at Bowen cost, on average, $41.46 per ton delivered to the plant. Starting in 1996 , the price was expected to fall to $29.82 per ton, delivered. Bowen's generators required coal with a total heat content of 202.3 million MMBtu; the heat content of the coal was 24.262 MMBtu per ton, so that Bowen needed 202,300,000/24.262 or 8.338 million tons of that sort of coal per year. The coal currently burned at Bowen contained an average of 1.6% sulfur by weight. Burning 8.338 million tons of this coal without installing additional pollution-control equipment would generate 266,550 tons of sulfur dioxide emissions. Option 2: Burn High-Sulfur Coal with Scrubbers; Sell Allowances In order to reduce emissions of sulfur dioxide at Bowen, the Southern Company could install wet-limestone flue gas desulfurization (FGD) equipment, commonly known as scrubbers. The gases from the generator already went through one pollution-control device called an electrostatic precipitator before release to the atmosphere; the precipitator eliminated most of the ash and particles from the gas. If scrubbers were installed, the gases, after leaving the precipitator, would enter another large chamber where they would be mixed with a slurry of water and limestone. The limestone would react with the sulfur dioxide, forming a sludge that could be landfilled. The gases, with 90% of the sulfur dioxide removed, would then be vented to the air. Scrubbers were enormous, as large as the generators themselves; they were also expensive. To install them at Bowen in time to reduce emissions in 1995 would require outlays of $143.85 million in 1992, $503.61 million in 1993, and $71.97 million in 1994. Once installed, the scrubbers would add 0.13 cents per kilowatt-hour to the operating costs of the Bowen plant, primarily for the purchase of limestone and the disposal of the sludge. They would also consume 2% of the total amount of electricity generated at the plant once they were turned on. This would, in effect, reduce revenues by 2%. The capital costs of the scrubbers could be depreciated over 20 years beginning in the first year of operation (i.e., beginning in 1995 if the scrubbers were installed to meet Phase One deadlines). In each of the first 5 years of the depreciation schedule, 14% of the capital costs could be depreciated; for the next 15 years, the company could depreciate 2% of the capital costs. These capital costs would include the capitalized interest (at 10% per year) on the scrubbers during the period when the devices were being installed. The scrubbers were not expected to have an appreciable salvage value. The Southern Company could also wait to begin installing the scrubbers until 1997, bringing them on line in time for the more stringent Phase Two requirements. This strategy would delay the capital outlays of installing the scrubbers by five years, but in Phase One Bowen would have to buy allowances or burn lower-sulfur coal. Option 3: Burn Low-Sulfur Coal Instead of installing the FGD equipment, the Southern Company could switch to lowsulfur coal from Kentucky or West Virginia. If Bowen chose to switch to this type of coal, it would wait until the beginning of 1996 to do so, since the utility's take-or-pay contract with its current supplier would expire at the end of 1995 . The low-sulfur coal contained 1% sulfur by weight. It cost less than the company was currently paying for the coal burned at Bowen, but its cost was greater than the expected 1996 cost of high-sulfur coal. Its use, without scrubbers, would generate extra allowances under Phase One of the Clean Air Act. During Phase Two, Bowen would have to purchase some allowances. Most coal was purchased and transported under contracts lasting from 5 to 20 years; the Southern Company could write contracts with mining companies and the railroads that would move the coal to Georgia, for any length of time it chose. Low-sulfur coal with a heat content of 24.110MMBtu per ton could be delivered to Bowen starting in 1996 for $30.37 per ton. Starting in 2000, however, its price was expected to rise to $34.92 per ton as the tighter controls in Phase Two drove up demand. It would take 8.391 million tons of this low-sulfur coal per year to generate electricity at Bowen at historic levels, and this coal would generate 167,650 tons of sulfur dioxide per year if burned without scrubbers. Switching to low-sulfur coal would require changes in the electrostatic precipitators used to control airborne particulate matter (fly ash) at Bowen, since the equipment currently in place was designed to operate with high-sulfur coal. These investments would cost $22.1 million and would be depreciated like the investments in scrubbers. Other Considerations If the Southern Company installed scrubbers at Bowen, it would have to make modest investments in working capital, primarily to maintain an inventory of limestone. If it switched to low-sulfur coal for Phase One, it would burn its two-month inventory of high-sulfur coal at the beginning of 1996, so that 1996 emissions would be somewhat higher than emissions in 1997 and subsequent years. The effects of such changes were small, however, and did not materially alter the company's appraisal of its options. Exhibit 1 Projected Operating Data for the Bowen Plant: Assumptions Common to All Options OUTPUT REVENUE $0.056 per kilowat t-hour INPUT REQUIRED 202. 3 million MMBtu (Coal tonnage depends on heat content of coal.) SULFUR DIOXIDE ALLOWANCES 1995199920002016254,580122,198 OPERATING COST (excluding fuel and pollution allowances) $0.00281 per kilowatt-hour TAX RATE 37.7% DISCOUNT RATE 10% (after tax) Exhibit 2 Projected Operating Data for the Bowen Plant: High-Sulfur Coal Without Scrubbers FUEL Cost of coal per ton 1992199519962016$41.4629.82 Tons of coal to meet input requirements (per year) 8. 338million POLLUTION Sulfur dioxide emitted per year 266,550 tons ADDITIONAL COSTS 0 Exhibit 3 Projected Operating Data for the Bowen Plant: High-Sulfur Coal with Scrubbers EIICI Exhibit 4 Projected Operating Data for the Bowen Plant: Low-Sulfur Coal without Scrubbers

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts