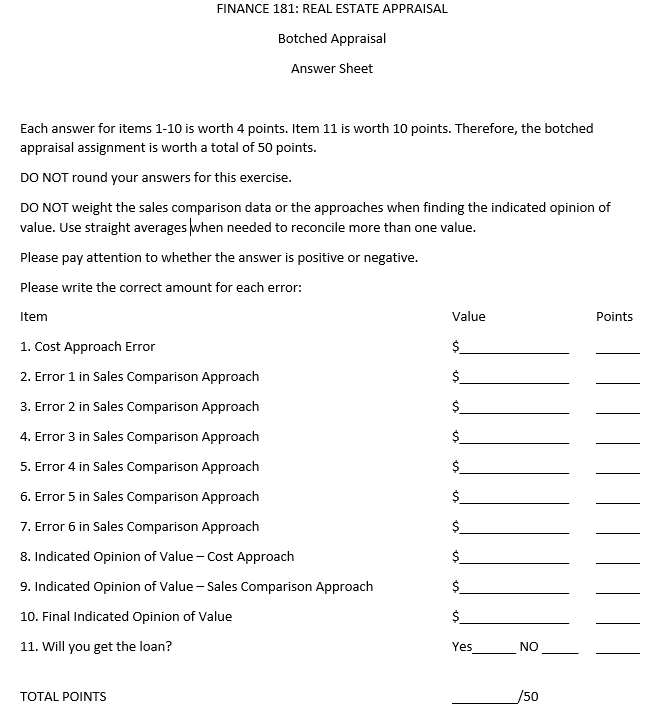

The Case of the Botched Appraisal You have recently graduated from University of Texas, Arlington and now doing well at your new job in Old Town, Maryland. Up until now you have been living in a small apartment but you have spent the past six months shopping for a house. Finally, you find the perfect house, a beautiful three-story house located at 849 Bershire Drive. The current owner accepts your offer of $230,000. You have $23,000 ($13,000 in cash and a $10,000 gift from your parents) to put down so you need a loan of $207,000 from the bank (90% of the sale price). You go to Colonial Mortgage for financing. Congratulations! You have passed Colonial Mortgage's underwriting criteria. Your income ratios (MHE and TOR) are acceptable and your credit history is good. This Savings and Loan is willing to lend you the $207,000 contingent on the appraisal of the property. Colonial hires John C. Appraiser to appraise the property. Seven days later you receive a letter from Colonial Mortgage stating that they will not lend you the money. The reason is that the appraiser's value of the property was only $214,000. The Savings and Loan explains that they cannot make a loan of $207,000 on a property worth $214,000. Based on the appraiser's market value estimate of $214,000 that is only about 3% equity ($7,000), this Saving and Loan requires you to have 10% equity. You are very disappointed! Instead of just giving up on your dream house, you remember that the bank must provide a copy of the appraisal if you make a written request. You write the bank and they send you a copy of the appraisal (see the attached appraisal). The first page of the appraisal is a description of the property (neighborhood, site, and improvements). You note that the appraiser has made positive comments on the neighborhood (increasing property values" etc.). Also, the site and improvements look pretty good too with an effective age of eight and "no apparent functional or external inadequacies" (obsolescence). The second page of the appraisal report contains the approaches to value. The appraiser used two of the three traditional approaches, the Cost Approach (located at the top of the page) and the Sales Comparison Approach (located in the middle of the page). You look at his analysis for a while and you determine that something is wrong in each approach. The appraiser has made seven mistakes, one major mistake in the Cost Approach and six mistakes regarding the adjustments in the Sales Comparison Approach (you have no problem with the actual dollar amount of the adjustments but you think that the appraiser reversed several of the signs by make some positive adjustment negative and negative adjustments positive). You figure that if you can identify the mistakes in the appraisal report, fix them, and determine what the market value of the property should be, you can go back to Colonial and save your loan. Assignment: Step 1: Read the appraisal report carefully. Try to get a feel for the market and the property being appraised. Step 2: Identify the one error in the Cost Approach and the six mistaken adjustments in the Sales Comparison Approach (remember you have no problem with the dollar amounts of the adjustments, just the signs). You can identify the mistakes simply by highlighting them on the report Step 3: Correct the mistakes and reappraise this property. Fix the mistakes and determine what the values by the Cost and Sales Comparison Approaches should be. Finally, reconcile the Cost and Sales Comparison Approaches and tell me what you think the property is really worth. Will you get the loan? FINANCE 181: REAL ESTATE APPRAISAL Botched Appraisal Answer Sheet Each answer for items 1-10 is worth 4 points. Item 11 is worth 10 points. Therefore, the botched appraisal assignment is worth a total of 50 points. DO NOT round your answers for this exercise. DO NOT weight the sales comparison data or the approaches when finding the indicated opinion of value. Use straight averages when needed to reconcile more than one value. Please pay attention to whether the answer is positive or negative. Please write the correct amount for each error: Item Value Points 1. Cost Approach Error 2. Error 1 in Sales Comparison Approach 3. Error 2 in Sales Comparison Approach 4. Error 3 in Sales Comparison Approach 5. Error 4 in Sales Comparison Approach 6. Error 5 in Sales Comparison Approach 7. Error 6 in Sales Comparison Approach 8. Indicated Opinion of Value - Cost Approach 9. Indicated Opinion of Value - Sales Comparison Approach ||||||||||| 10. Final Indicated Opinion of Value 11. Will you get the loan? Yes NO TOTAL POINTS The Case of the Botched Appraisal You have recently graduated from University of Texas, Arlington and now doing well at your new job in Old Town, Maryland. Up until now you have been living in a small apartment but you have spent the past six months shopping for a house. Finally, you find the perfect house, a beautiful three-story house located at 849 Bershire Drive. The current owner accepts your offer of $230,000. You have $23,000 ($13,000 in cash and a $10,000 gift from your parents) to put down so you need a loan of $207,000 from the bank (90% of the sale price). You go to Colonial Mortgage for financing. Congratulations! You have passed Colonial Mortgage's underwriting criteria. Your income ratios (MHE and TOR) are acceptable and your credit history is good. This Savings and Loan is willing to lend you the $207,000 contingent on the appraisal of the property. Colonial hires John C. Appraiser to appraise the property. Seven days later you receive a letter from Colonial Mortgage stating that they will not lend you the money. The reason is that the appraiser's value of the property was only $214,000. The Savings and Loan explains that they cannot make a loan of $207,000 on a property worth $214,000. Based on the appraiser's market value estimate of $214,000 that is only about 3% equity ($7,000), this Saving and Loan requires you to have 10% equity. You are very disappointed! Instead of just giving up on your dream house, you remember that the bank must provide a copy of the appraisal if you make a written request. You write the bank and they send you a copy of the appraisal (see the attached appraisal). The first page of the appraisal is a description of the property (neighborhood, site, and improvements). You note that the appraiser has made positive comments on the neighborhood (increasing property values" etc.). Also, the site and improvements look pretty good too with an effective age of eight and "no apparent functional or external inadequacies" (obsolescence). The second page of the appraisal report contains the approaches to value. The appraiser used two of the three traditional approaches, the Cost Approach (located at the top of the page) and the Sales Comparison Approach (located in the middle of the page). You look at his analysis for a while and you determine that something is wrong in each approach. The appraiser has made seven mistakes, one major mistake in the Cost Approach and six mistakes regarding the adjustments in the Sales Comparison Approach (you have no problem with the actual dollar amount of the adjustments but you think that the appraiser reversed several of the signs by make some positive adjustment negative and negative adjustments positive). You figure that if you can identify the mistakes in the appraisal report, fix them, and determine what the market value of the property should be, you can go back to Colonial and save your loan. Assignment: Step 1: Read the appraisal report carefully. Try to get a feel for the market and the property being appraised. Step 2: Identify the one error in the Cost Approach and the six mistaken adjustments in the Sales Comparison Approach (remember you have no problem with the dollar amounts of the adjustments, just the signs). You can identify the mistakes simply by highlighting them on the report Step 3: Correct the mistakes and reappraise this property. Fix the mistakes and determine what the values by the Cost and Sales Comparison Approaches should be. Finally, reconcile the Cost and Sales Comparison Approaches and tell me what you think the property is really worth. Will you get the loan? FINANCE 181: REAL ESTATE APPRAISAL Botched Appraisal Answer Sheet Each answer for items 1-10 is worth 4 points. Item 11 is worth 10 points. Therefore, the botched appraisal assignment is worth a total of 50 points. DO NOT round your answers for this exercise. DO NOT weight the sales comparison data or the approaches when finding the indicated opinion of value. Use straight averages when needed to reconcile more than one value. Please pay attention to whether the answer is positive or negative. Please write the correct amount for each error: Item Value Points 1. Cost Approach Error 2. Error 1 in Sales Comparison Approach 3. Error 2 in Sales Comparison Approach 4. Error 3 in Sales Comparison Approach 5. Error 4 in Sales Comparison Approach 6. Error 5 in Sales Comparison Approach 7. Error 6 in Sales Comparison Approach 8. Indicated Opinion of Value - Cost Approach 9. Indicated Opinion of Value - Sales Comparison Approach ||||||||||| 10. Final Indicated Opinion of Value 11. Will you get the loan? Yes NO