Question

The cash flow forecast is based on the following key assumptions: All sales are on 60 days credit, but customers take, on average, 90 days

The cash flow forecast is based on the following key assumptions: All sales are on 60 days credit, but customers take, on average, 90 days to pay, which is what is reflected in the cash flow forecast. No increases in selling prices are planned. Suppliers, on average, are paid in 60 days. Production is evenly scheduled throughout the year and finished goods are stored for the peak season; opening inventory on 01 January 2022 is 1.25 million and closing inventory on 31 December 2022 is estimated to be 0.90 million. Wages and operating costs are paid in the month incurred. The capital expenditure forecast for 2022 is 0.85 million in February for new plant to increase capacity and 0.35 million in June for new delivery vehicles. Further capital expenditure is planned in 2023 to meet expected demand. Depreciation on assets already owned by CPP on 01 January will be 0.85 million in 2022; the companys depreciation policy is 25% straight line, with a full year depreciation charged in the year of acquisition. Sales in October 2022, November 2022 and December 2022 are expected to be 2.82million, 2.11 million and 1.99 million respectively. Purchases for November 2022 and December 2022 are expected to be 1.01 million and 0.88 million respectively. 9 CPPs revenues are seasonal, with a peak in the autumn during the lead up to Christmas. The current banking facility (all overdraft) is 1.75million and interest at 6% on any of the facility used. In a recent meeting the companys bank, the Board of Directors was informed that the bank will not increase the existing facility without a material increase in the interest rate. The Board of Directors comprises five directors who between them own 70% of the ordinary shares but have no money to invest any more money in 2022 or 2023. The remaining 30% of the ordinary shares are owned by a variety of individuals that have little interest in participating in company operations and are satisfied just to continue to receive dividends at the levels currently being paid

Required.

1)Calculate CPPs estimated profit before taxation for the year to 31 December 2022. Show all workings.

2) Prepare a report for the Board of Directors of CPP advising of actions it may consider to improve the estimated 2022 cash flow and evaluate the impact of these actions on CPPs business.

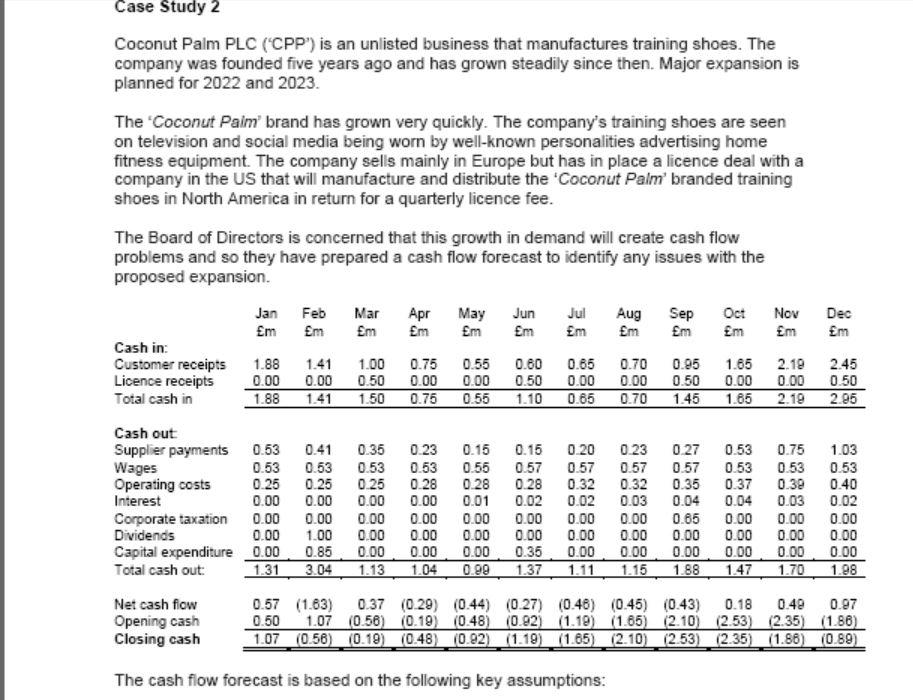

Case Study 2 Coconut Palm PLC (CPP) is an unlisted business that manufactures training shoes. The company was founded five years ago and has grown steadily since then. Major expansion is planned for 2022 and 2023. The Coconut Paim' brand has grown very quickly. The company's training shoes are seen on television and social media being worn by well-known personalities advertising home fitness equipment. The company sells mainly in Europe but has in place a licence deal with a company in the US that will manufacture and distribute the 'Coconut Palm branded training shoes in North America in return for a quarterly licence fee. The Board of Directors is concerned that this growth in demand will create cash flow problems and so they have prepared a cash flow forecast to identify any issues with the proposed expansion Feb Mar Apr May Jun Jul Aug Sep Oct Nov m Em Em Em Em Em Em m m m Cash in: Customer receipts 1.88 1.41 1.00 0.75 0.55 0.60 0.85 0.70 0.95 1.65 2.19 Licence receipts 0.00 0.00 0.50 0.00 0.00 0.50 0.00 0.00 0.50 0.00 0.00 Total cash in 1.88 1.50 0.75 0.55 1.10 0.65 0.70 1.45 1.65 2.19 Jan m Dec m 2.45 0.50 2.95 1.41 Cash out Supplier payments 0.53 0.41 0.35 0.23 0.15 0.15 0.20 0.23 0.27 0.53 0.75 1.03 Wages 0.53 0.53 0.53 0.53 0.55 0.57 0.57 0.57 0.57 0.53 0.53 0.53 Operating costs 0.25 0.25 0.25 0.28 0.28 0.28 0.32 0.32 0.35 0.37 0.39 0.40 Interest 0.00 0.00 0.00 0.00 0.01 0.02 0.02 0.03 0.04 0.04 0.03 0.02 Corporate taxation 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.65 0.00 0.00 0.00 Dividends 0.00 1.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 Capital expenditure 0.00 0.85 0.00 0.00 0.00 0.35 0.00 0.00 0.00 0.00 0.00 0.00 Total cash out: 1.31 3.04 1.13 1.04 0.99 1.37 1.11 1.15 1.88 1.47 1.70 1.98 Net cash flow 0.57 (1.63) 0.37 (0.29) (0.44) (0.27) (0.46) (0.45) (0.43) 0.18 0.49 0.97 Opening cash 0.50 1.07 (0.56) (0.19) (0.48) (0.92) (1.1) (1.65) (2.10) (2.53) (2.35) (1.86) Closing cash 1.07 (0.56) (0.19) (0.48) (0.82) (1.19) (1.85) (2.10) (2.53) (2.35) (1.86) (0.89) The cash flow forecast is based on the following key assumptions: Case Study 2 Coconut Palm PLC (CPP) is an unlisted business that manufactures training shoes. The company was founded five years ago and has grown steadily since then. Major expansion is planned for 2022 and 2023. The Coconut Paim' brand has grown very quickly. The company's training shoes are seen on television and social media being worn by well-known personalities advertising home fitness equipment. The company sells mainly in Europe but has in place a licence deal with a company in the US that will manufacture and distribute the 'Coconut Palm branded training shoes in North America in return for a quarterly licence fee. The Board of Directors is concerned that this growth in demand will create cash flow problems and so they have prepared a cash flow forecast to identify any issues with the proposed expansion Feb Mar Apr May Jun Jul Aug Sep Oct Nov m Em Em Em Em Em Em m m m Cash in: Customer receipts 1.88 1.41 1.00 0.75 0.55 0.60 0.85 0.70 0.95 1.65 2.19 Licence receipts 0.00 0.00 0.50 0.00 0.00 0.50 0.00 0.00 0.50 0.00 0.00 Total cash in 1.88 1.50 0.75 0.55 1.10 0.65 0.70 1.45 1.65 2.19 Jan m Dec m 2.45 0.50 2.95 1.41 Cash out Supplier payments 0.53 0.41 0.35 0.23 0.15 0.15 0.20 0.23 0.27 0.53 0.75 1.03 Wages 0.53 0.53 0.53 0.53 0.55 0.57 0.57 0.57 0.57 0.53 0.53 0.53 Operating costs 0.25 0.25 0.25 0.28 0.28 0.28 0.32 0.32 0.35 0.37 0.39 0.40 Interest 0.00 0.00 0.00 0.00 0.01 0.02 0.02 0.03 0.04 0.04 0.03 0.02 Corporate taxation 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.65 0.00 0.00 0.00 Dividends 0.00 1.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 Capital expenditure 0.00 0.85 0.00 0.00 0.00 0.35 0.00 0.00 0.00 0.00 0.00 0.00 Total cash out: 1.31 3.04 1.13 1.04 0.99 1.37 1.11 1.15 1.88 1.47 1.70 1.98 Net cash flow 0.57 (1.63) 0.37 (0.29) (0.44) (0.27) (0.46) (0.45) (0.43) 0.18 0.49 0.97 Opening cash 0.50 1.07 (0.56) (0.19) (0.48) (0.92) (1.1) (1.65) (2.10) (2.53) (2.35) (1.86) Closing cash 1.07 (0.56) (0.19) (0.48) (0.82) (1.19) (1.85) (2.10) (2.53) (2.35) (1.86) (0.89) The cash flow forecast is based on the following key assumptionsStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Security Audit And Control Features Oracle E Business Suite

Authors: Deloitte Touche Tohmatsu Research Team And Isaca

3rd Edition

1604201061, 978-1604201062