Answered step by step

Verified Expert Solution

Question

1 Approved Answer

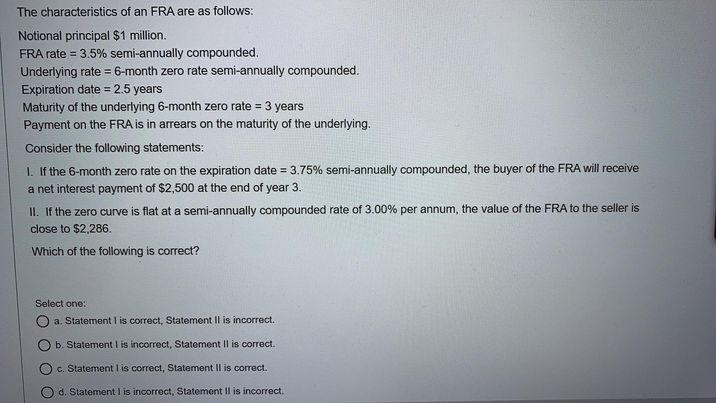

The characteristics of an FRA are as follows: Notional principal $1 million. FRA rate = 3.5% semi-annually compounded. Underlying rate = 6-month zero rate semi-annually

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Professionals Handbook Of Financial Risk Management

Authors: Lev Borodovsky, Marc Lore

1st Edition

0750641118, 978-0750641111