Answered step by step

Verified Expert Solution

Question

1 Approved Answer

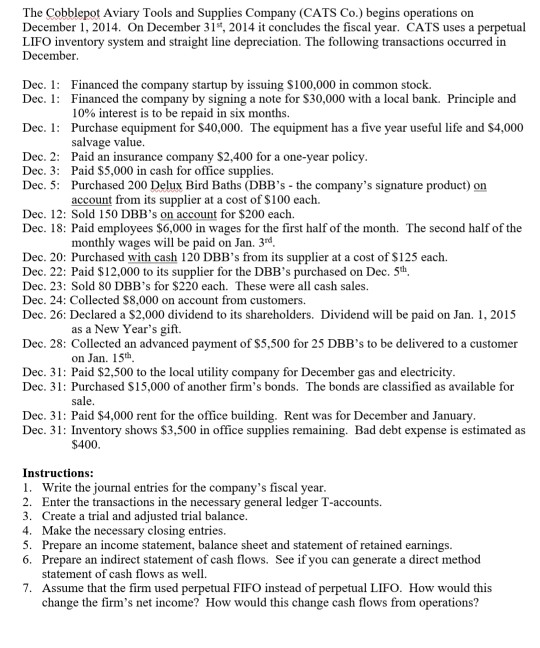

The Cobblepot Aviary Tools and Supplies Company (CATS Co.) begins operations on December 1, 2014. On December 31, 2014 it concludes the fiscal year.

The Cobblepot Aviary Tools and Supplies Company (CATS Co.) begins operations on December 1, 2014. On December 31, 2014 it concludes the fiscal year. CATS uses a perpetual LIFO inventory system and straight line depreciation. The following transactions occurred in December. Dec. 1: Financed the company startup by issuing $100,000 in common stock. Dec. 1: Dec. 1: Dec. 2: Dec. 3: Dec. 5: Financed the company by signing a note for $30,000 with a local bank. Principle and 10% interest is to be repaid in six months. Purchase equipment for $40,000. The equipment has a five year useful life and $4,000 salvage value. Paid an insurance company $2,400 for a one-year policy. Paid $5,000 in cash for office supplies. Purchased 200 Delux Bird Baths (DBB's - the company's signature product) on account from its supplier at a cost of $100 each. Dec. 12: Sold 150 DBB's on account for $200 each. Dec. 18: Paid employees $6,000 in wages for the first half of the month. The second half of the monthly wages will be paid on Jan. 3rd, Dec. 20: Purchased with cash 120 DBB's from its supplier at a cost of $125 each. Dec. 22: Paid $12,000 to its supplier for the DBB's purchased on Dec. 5th. Dec. 23: Sold 80 DBB's for $220 each. These were all cash sales. Dec. 24: Collected $8,000 on account from customers. Dec. 26: Declared a $2,000 dividend to its shareholders. Dividend will be paid on Jan. 1, 2015 as a New Year's gift. Dec. 28: Collected an advanced payment of $5,500 for 25 DBB's to be delivered to a customer on Jan. 15th Dec. 31: Paid $2,500 to the local utility company for December gas and electricity. Dec. 31: Purchased $15,000 of another firm's bonds. The bonds are classified as available for sale. Dec. 31: Paid $4,000 rent for the office building. Rent was for December and January. Dec. 31: Inventory shows $3,500 in office supplies remaining. Bad debt expense is estimated as $400. Instructions: 1. Write the journal entries for the company's fiscal year. 2. Enter the transactions in the necessary general ledger T-accounts. 3. Create a trial and adjusted trial balance. 4. Make the necessary closing entries. 5. Prepare an income statement, balance sheet and statement of retained earnings. 6. Prepare an indirect statement of cash flows. See if you can generate a direct method statement of cash flows as well. 7. Assume that the firm used perpetual FIFO instead of perpetual LIFO. How would this change the firm's net income? How would this change cash flows from operations?

Step by Step Solution

★★★★★

3.38 Rating (154 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamental Accounting Principles Volume 1

Authors: Kermit Larson, Tilly Jensen, Heidi Dieckmann

15th Canadian Edition

1259259803, 978-1259259807