Answered step by step

Verified Expert Solution

Question

1 Approved Answer

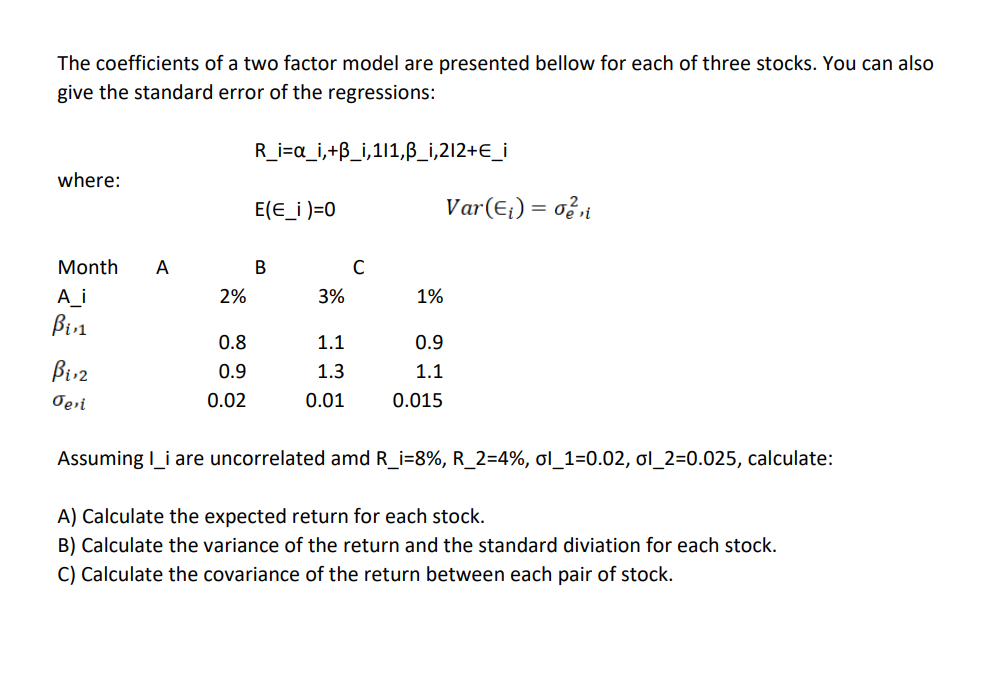

The coefficients of a two factor model are presented bellow for each of three stocks. You can also give the standard error of the regressions:

The coefficients of a two factor model are presented bellow for each of three stocks. You can also give the standard error of the regressions: Ri=i,+_i,11,i,212+_i where: E(i)=0Var(i)=e2,i Assuming I_i are uncorrelated amd R_i=8%,R_2=4%,_1=0.02,_2=0.025, calculate: A) Calculate the expected return for each stock. B) Calculate the variance of the return and the standard diviation for each stock. C) Calculate the covariance of the return between each pair of stock

The coefficients of a two factor model are presented bellow for each of three stocks. You can also give the standard error of the regressions: Ri=i,+_i,11,i,212+_i where: E(i)=0Var(i)=e2,i Assuming I_i are uncorrelated amd R_i=8%,R_2=4%,_1=0.02,_2=0.025, calculate: A) Calculate the expected return for each stock. B) Calculate the variance of the return and the standard diviation for each stock. C) Calculate the covariance of the return between each pair of stock Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Currency And Finance In Time Of War A Lecture

Authors: Francis Ysidro Edgeworth

1st Edition

1178449807, 9781178449808