Answered step by step

Verified Expert Solution

Question

1 Approved Answer

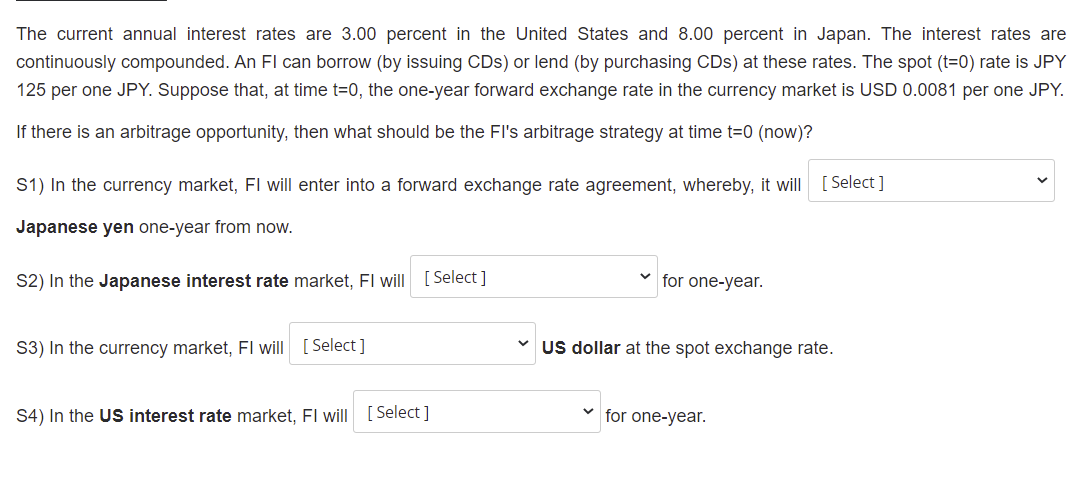

The current annual interest rates are 3.00 percent in the United States and 8.00 percent in Japan. The interest rates are continuously compounded. An Fl

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Marketing For Financial Advisors

Authors: Eric Bradlow, Keith Niedermeier, Patti Williams

1st Edition

0071605142, 978-0071605144