Answered step by step

Verified Expert Solution

Question

1 Approved Answer

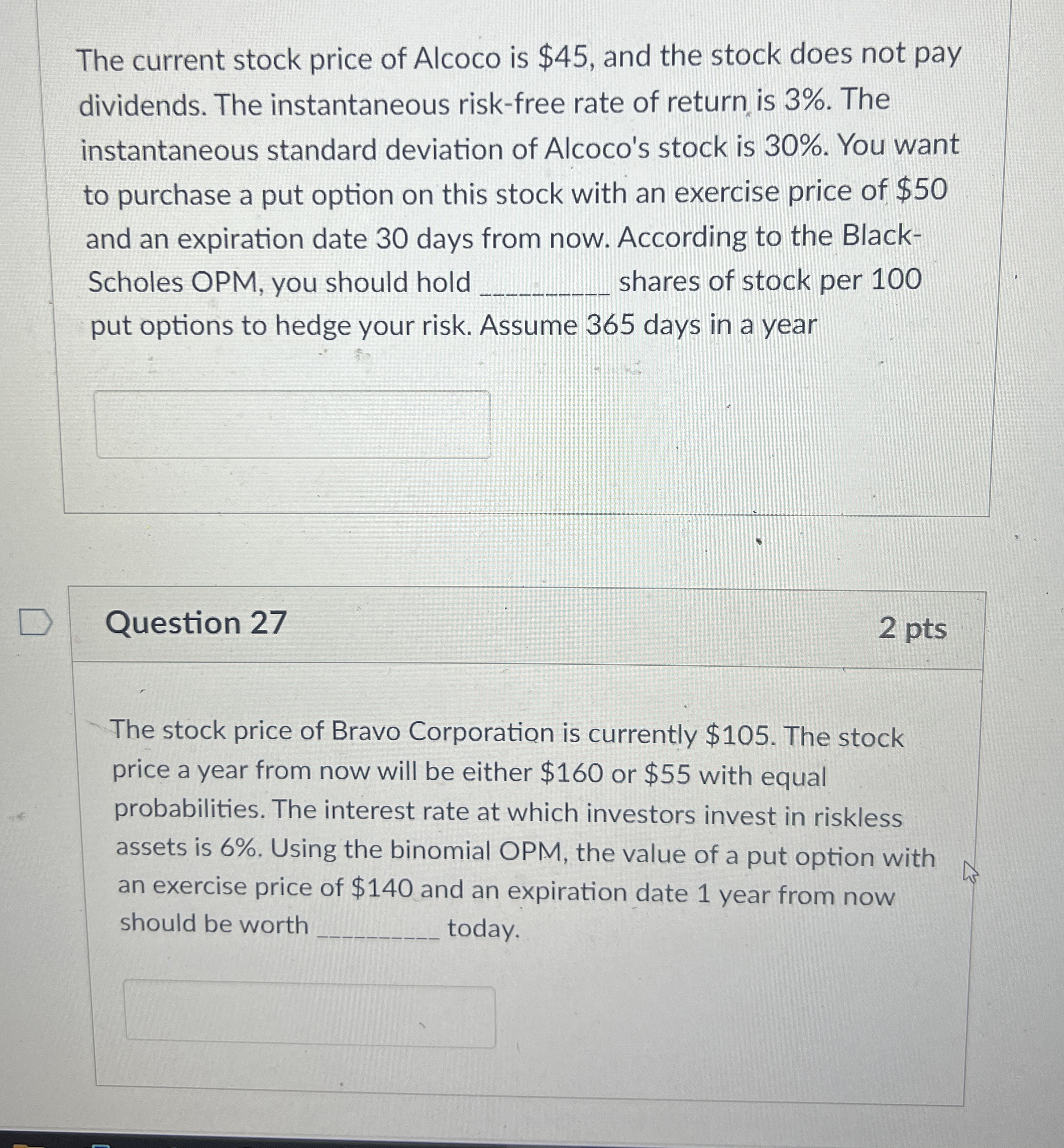

The current stock price of Alcoco is $ 4 5 , and the stock does not pay dividends. The instantaneous risk - free rate of

The current stock price of Alcoco is $ and the stock does not pay dividends. The instantaneous riskfree rate of return is The instantaneous standard deviation of Alcoco's stock is You want to purchase a put option on this stock with an exercise price of $ and an expiration date days from now. According to the BlackScholes OPM, you should hold shares of stock per put options to hedge your risk. Assume days in a year

Question

pts

The stock price of Bravo Corporation is currently $ The stock price a year from now will be either $ or $ with equal probabilities. The interest rate at which investors invest in riskless assets is Using the binomial OPM, the value of a put option with an exercise price of $ and an expiration date year from now should be worth today. Can you give me a detailed explanation on how to do this? Excel is perfect, but written is fine as well! Thank you

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Ecological Money And Finance

Authors: Thomas Lagoarde-Segot

1st Edition

3031142314, 978-3031142314