Answered step by step

Verified Expert Solution

Question

1 Approved Answer

The end of the question. Hello, Book Name: cost Management, Strategies for business decision. International Edition Homework: Chapter 15 (Transfer Pricing), Case 15.43 Case 15.43

The end of the question.

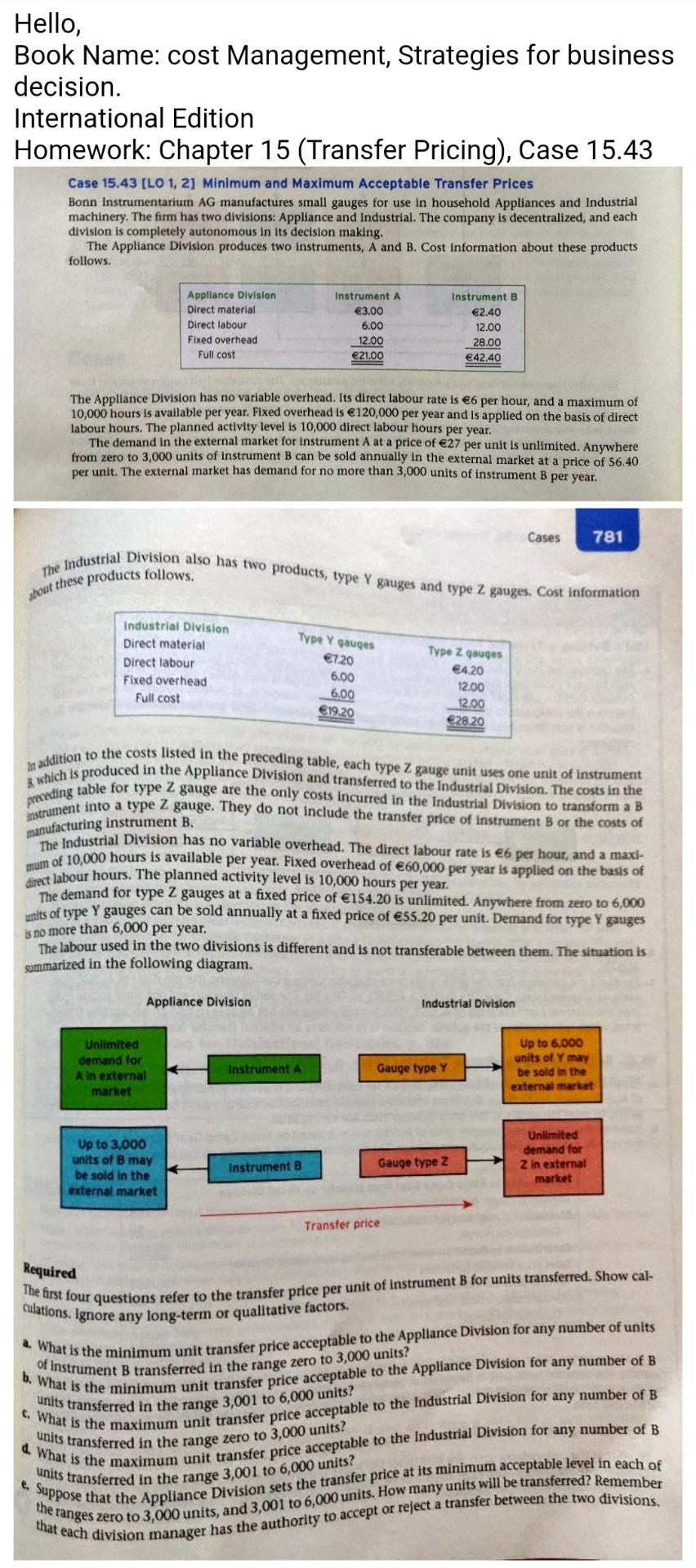

Hello, Book Name: cost Management, Strategies for business decision. International Edition Homework: Chapter 15 (Transfer Pricing), Case 15.43 Case 15.43 [LO 1, 2] Minimum and Maximum Acceptable Transfer Prices Bonn Instrumentarium AG manufactures small gauges for use in household Appliances and Industrial machinery. The firm has two divisions: Appliance and Industrial. The company is decentralized, and each division is completely autonomous in its decision making. The Appliance Division produces two instruments, A and B. Cost information about these products follows. Appliance Division Direct material Direct labour Fixed overhead Full cost Instrument A 3.00 6.00 Instrument B 2.40 12.00 28.00 42.40 12.00 21.00 The Appliance Division has no variable overhead. Its direct labour rate is 6 per hour, and a maximum of 10,000 hours is available per year. Fixed overhead is 120,000 per year and is applied on the basis of direct labour hours. The planned activity level is 10,000 direct labour hours per year. The demand in the external market for instrument A at a price of 27 per unit is unlimited. Anywhere from zero to 3,000 units of instrument B can be sold annually in the external market at a price of 56.40 per unit. The external market has demand for no more than 3,000 units of instrument B per year. Cases 781 The Industrial Division also has two products, type Y gauges and type 2 gauges. Cost information shout these products follows. Industrial Division Direct material Direct labour 4.20 Fixed overhead 12.00 Full cost 12.00 Type Z gauges Type Y gauges 7.20 6.00 6.00 19.20 28.20 In addition to the costs listed in the preceding table, each type Z gauge unit uses one unit of instrument which is produced in the Appliance Division and transferred to the Industrial Division. The costs in the preceding table for type Z gauge are the only costs incurred in the Industrial Division to transform a B instrument into a type Z gauge. They do not include the transfer price of instrument B or the costs of manufacturing instrument The Industrial Division has no variable overhead. The direct labour rate is 6 per hour, and a maxi. mum of 10,000 hours is available per year. Fixed overhead of 60,000 per year is applied on the basis of direct labour hours. The planned activity level is 10,000 hours per year. The demand for type Z gauges at a fixed price of 154.20 is unlimited. Anywhere from zero to 6,000 units of type Y gauges can be sold annually at a fixed price of 55.20 per unit. Demand for type Y gauges is no more than 6,000 per year, The labour used in the two divisions is different and is not transferable between them. The situation is summarized in the following diagram. Appliance Division Industrial Division Unlimited demand for A ln external market Instrument A Gauge type Y Up to 6.000 units of Y may be sold in the external market Up to 3,000 units of B may be sold in the external market Unlimited demand for Z in external market Instrument B Gauge type 2 Transfer price Required The first four questions refer to the transfer price per unit of instrument B for units transferred. Show cal- culations. Ignore any long-term or qualitative factors. a. What is the minimum unit transfer price acceptable to the Appliance Division for any number of units b. What is the minimum unit transfer price acceptable to the Appliance Division for any number of B of instrument B transferred in the range zero to 3,000 units? c. What is the maximum unit transfer price acceptable to the Industrial Division for any number of B units transferred in the range 3,001 to 6,000 units? d. What is the maximum unit transfer price acceptable to the Industrial Division for any number of B units transferred in the range zero to 3,000 units? units transferred in the range 3,001 to 6,000 units? Suppose that the Appliance Division sets the transfer price at its minimum acceptable level in each of the ranges zero to 3,000 units, and 3,001 to 6,000 units. How many units will be transferred? Remember that each division manager has the authority to accept or reject a transfer between the two divisions. e Hello, Book Name: cost Management, Strategies for business decision. International Edition Homework: Chapter 15 (Transfer Pricing), Case 15.43 Case 15.43 [LO 1, 2] Minimum and Maximum Acceptable Transfer Prices Bonn Instrumentarium AG manufactures small gauges for use in household Appliances and Industrial machinery. The firm has two divisions: Appliance and Industrial. The company is decentralized, and each division is completely autonomous in its decision making. The Appliance Division produces two instruments, A and B. Cost information about these products follows. Appliance Division Direct material Direct labour Fixed overhead Full cost Instrument A 3.00 6.00 Instrument B 2.40 12.00 28.00 42.40 12.00 21.00 The Appliance Division has no variable overhead. Its direct labour rate is 6 per hour, and a maximum of 10,000 hours is available per year. Fixed overhead is 120,000 per year and is applied on the basis of direct labour hours. The planned activity level is 10,000 direct labour hours per year. The demand in the external market for instrument A at a price of 27 per unit is unlimited. Anywhere from zero to 3,000 units of instrument B can be sold annually in the external market at a price of 56.40 per unit. The external market has demand for no more than 3,000 units of instrument B per year. Cases 781 The Industrial Division also has two products, type Y gauges and type 2 gauges. Cost information shout these products follows. Industrial Division Direct material Direct labour 4.20 Fixed overhead 12.00 Full cost 12.00 Type Z gauges Type Y gauges 7.20 6.00 6.00 19.20 28.20 In addition to the costs listed in the preceding table, each type Z gauge unit uses one unit of instrument which is produced in the Appliance Division and transferred to the Industrial Division. The costs in the preceding table for type Z gauge are the only costs incurred in the Industrial Division to transform a B instrument into a type Z gauge. They do not include the transfer price of instrument B or the costs of manufacturing instrument The Industrial Division has no variable overhead. The direct labour rate is 6 per hour, and a maxi. mum of 10,000 hours is available per year. Fixed overhead of 60,000 per year is applied on the basis of direct labour hours. The planned activity level is 10,000 hours per year. The demand for type Z gauges at a fixed price of 154.20 is unlimited. Anywhere from zero to 6,000 units of type Y gauges can be sold annually at a fixed price of 55.20 per unit. Demand for type Y gauges is no more than 6,000 per year, The labour used in the two divisions is different and is not transferable between them. The situation is summarized in the following diagram. Appliance Division Industrial Division Unlimited demand for A ln external market Instrument A Gauge type Y Up to 6.000 units of Y may be sold in the external market Up to 3,000 units of B may be sold in the external market Unlimited demand for Z in external market Instrument B Gauge type 2 Transfer price Required The first four questions refer to the transfer price per unit of instrument B for units transferred. Show cal- culations. Ignore any long-term or qualitative factors. a. What is the minimum unit transfer price acceptable to the Appliance Division for any number of units b. What is the minimum unit transfer price acceptable to the Appliance Division for any number of B of instrument B transferred in the range zero to 3,000 units? c. What is the maximum unit transfer price acceptable to the Industrial Division for any number of B units transferred in the range 3,001 to 6,000 units? d. What is the maximum unit transfer price acceptable to the Industrial Division for any number of B units transferred in the range zero to 3,000 units? units transferred in the range 3,001 to 6,000 units? Suppose that the Appliance Division sets the transfer price at its minimum acceptable level in each of the ranges zero to 3,000 units, and 3,001 to 6,000 units. How many units will be transferred? Remember that each division manager has the authority to accept or reject a transfer between the two divisions. eStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Front Office Operations And Auditing Workbook

Authors: Patrick J. Moreo, Gail Sammons, Jeff Beck

2nd Edition

0130324930, 978-0130324931