Answered step by step

Verified Expert Solution

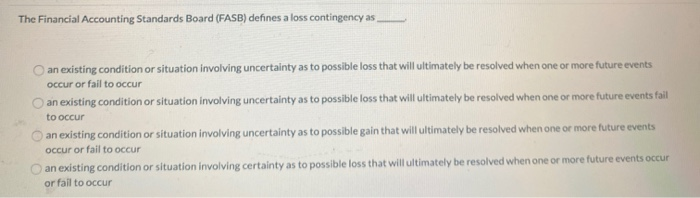

Question

1 Approved Answer

The Financial Accounting Standards Board (FASB) defines a loss contingency as an existing condition or situation involving uncertainty as to possible loss that will ultimately

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

I Love My Awesome Auditor

Authors: Lovely Hearts Publishing

1st Edition

1794298169, 978-1794298163