Answered step by step

Verified Expert Solution

Question

1 Approved Answer

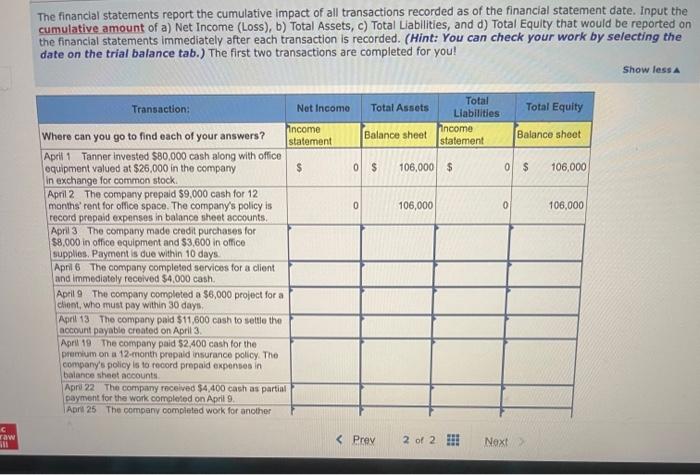

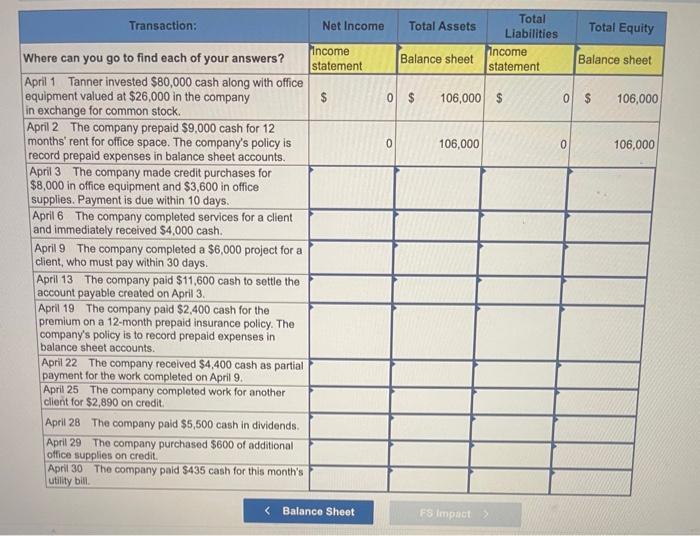

The financial statements report the cumulative impact of all transactions recorded as of the financial statement date. Input the cumulative amount of a) Net

The financial statements report the cumulative impact of all transactions recorded as of the financial statement date. Input the cumulative amount of a) Net Income (Loss), b) Total Assets, c) Total Liabilities, and d) Total Equity that would be reported on the financial statements immediately after each transaction is recorded. (Hint: You can check your work by selecting the date on the trial balance tab.) The first two transactions are completed for you! C raw Transaction: Where can you go to find each of your answers? April 1 Tanner invested $80,000 cash along with office equipment valued at $26,000 in the company in exchange for common stock. April 2 The company prepaid $9,000 cash for 12 months' rent for office space. The company's policy is record prepaid expenses in balance sheet accounts. April 3 The company made credit purchases for $8,000 in office equipment and $3,600 in office supplies. Payment is due within 10 days April 6 The company completed services for a client and immediately received $4,000 cash. April 9 The company completed a $6,000 project for a client, who must pay within 30 days, April 13 The company paid $11,600 cash to settle the account payable created on April 3. April 19 The company paid $2,400 cash for the premium on a 12-month prepaid insurance policy. The company's policy is to record prepaid expenses in balance sheet accounts. April 22 The company received $4,400 cash as partial payment for the work completed on April 9. April 25 The company completed work for another Net Income Total Assets Total Liabilities Total Equity Income Balance sheet statement Income statement Balance sheet. $ 0 $ 106,000 $ 0 $ 106,000 0 106,000 0 106,000 < Prev 2 of 2 Next > Show less A Transaction: Where can you go to find each of your answers? April 1 Tanner invested $80,000 cash along with office equipment valued at $26,000 in the company in exchange for common stock. April 2 The company prepaid $9,000 cash for 12 months' rent for office space. The company's policy is record prepaid expenses in balance sheet accounts. April 3 The company made credit purchases for $8,000 in office equipment and $3,600 in office supplies. Payment is due within 10 days. April 6 The company completed services for a client and immediately received $4,000 cash. April 9 The company completed a $6,000 project for a client, who must pay within 30 days. April 13 The company paid $11,600 cash to settle the account payable created on April 3. April 19 The company paid $2,400 cash for the premium on a 12-month prepaid insurance policy. The company's policy is to record prepaid expenses in balance sheet accounts. April 22 The company received $4,400 cash as partial payment for the work completed on April 9.1 April 25 The company completed work for another client for $2,890 on credit. April 28 The company paid $5,500 cash in dividends. April 29 The company purchased $600 of additional office supplies on credit. April 30 The company paid $435 cash for this month's utility bill. Net Income Total Assets Total Liabilities Total Equity Income Balance sheet statement Income statement Balance sheet $ 0 $ 106,000 $ 0 $ 106,000 0 106,000 < Balance Sheet FS Impact > 106,000

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516