The First picture here is the instructions, we have a-f completed I just need help with the last two questions G, and H (which is shown at the bottom) I just need help making and calculating the T-account and answering G, thank you.

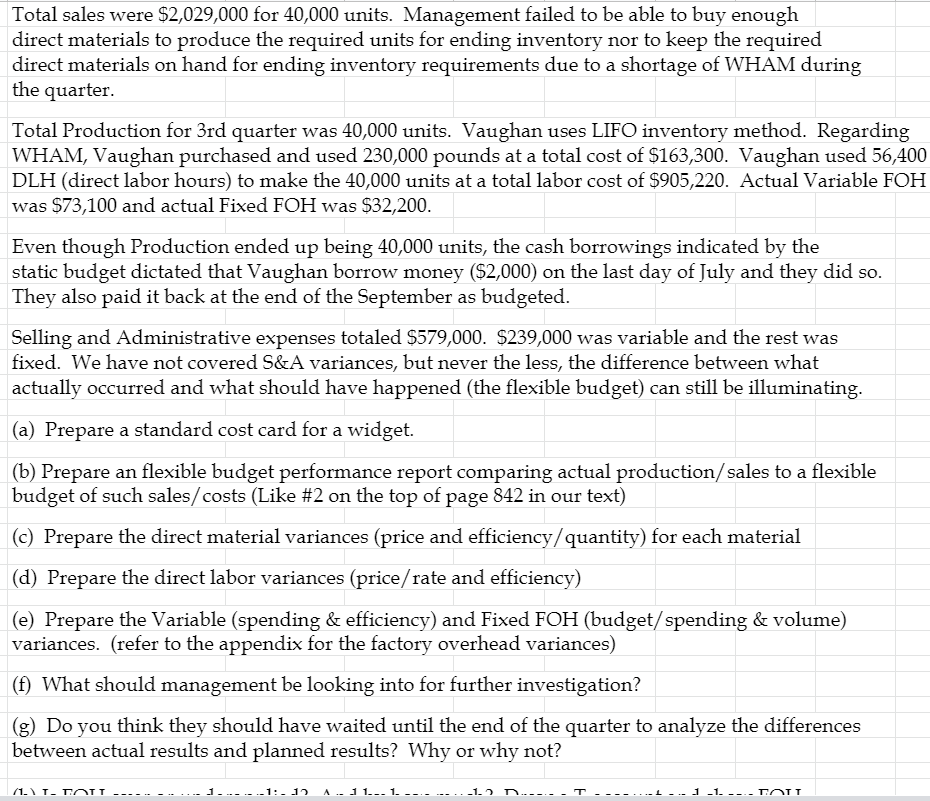

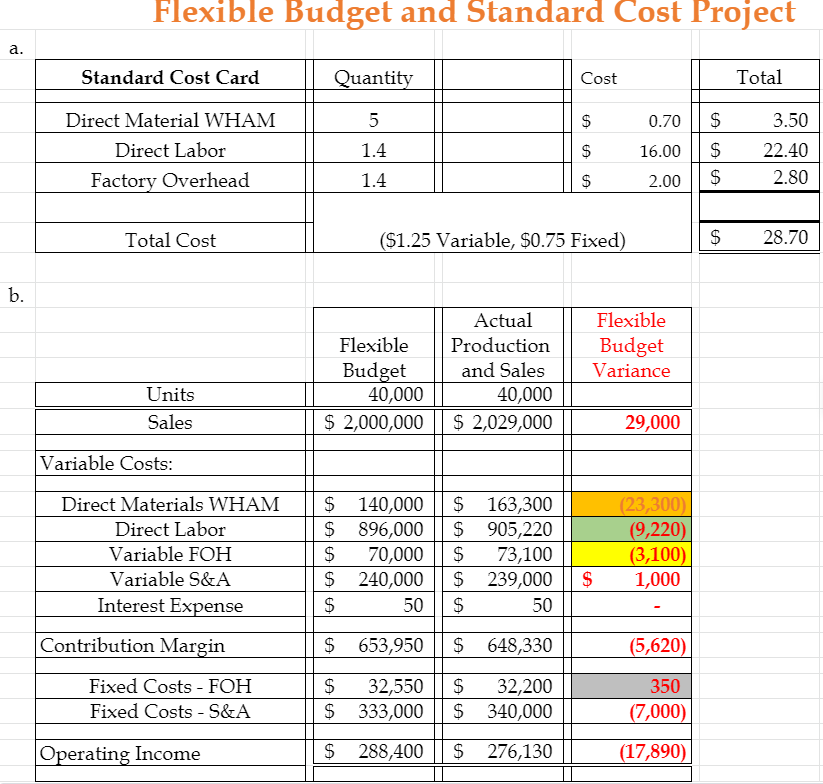

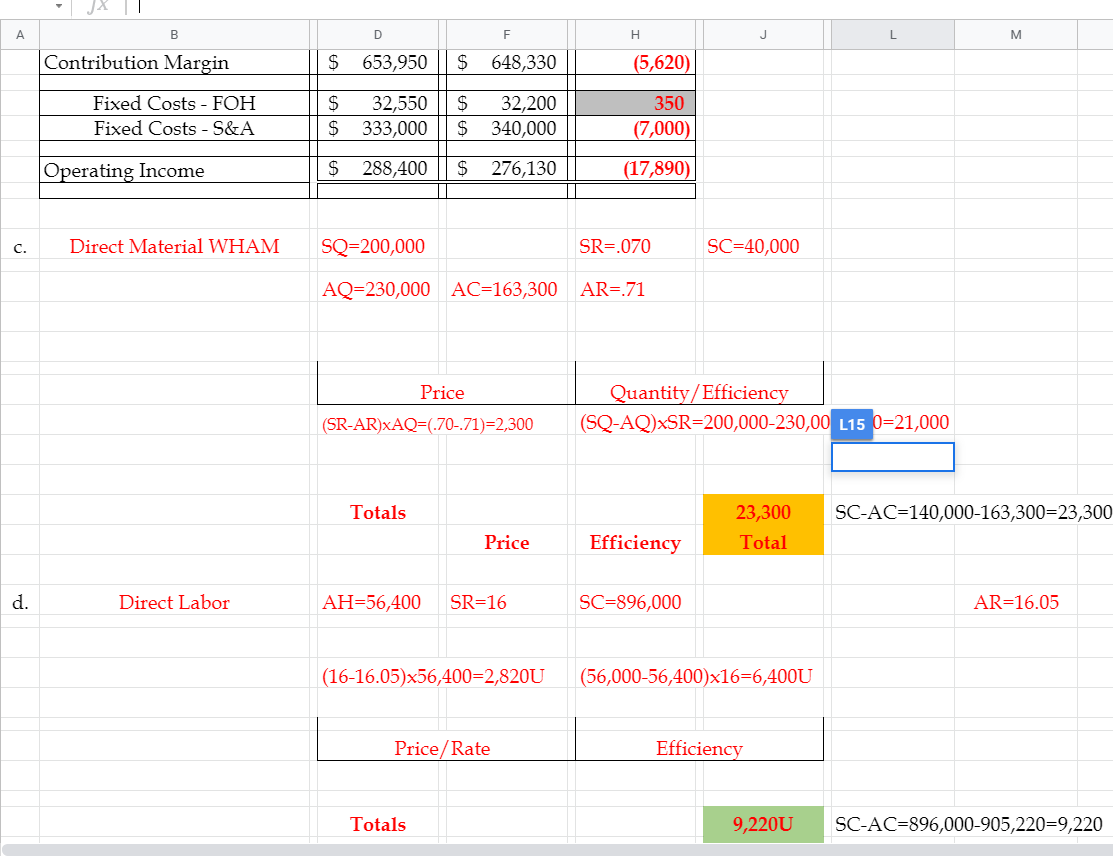

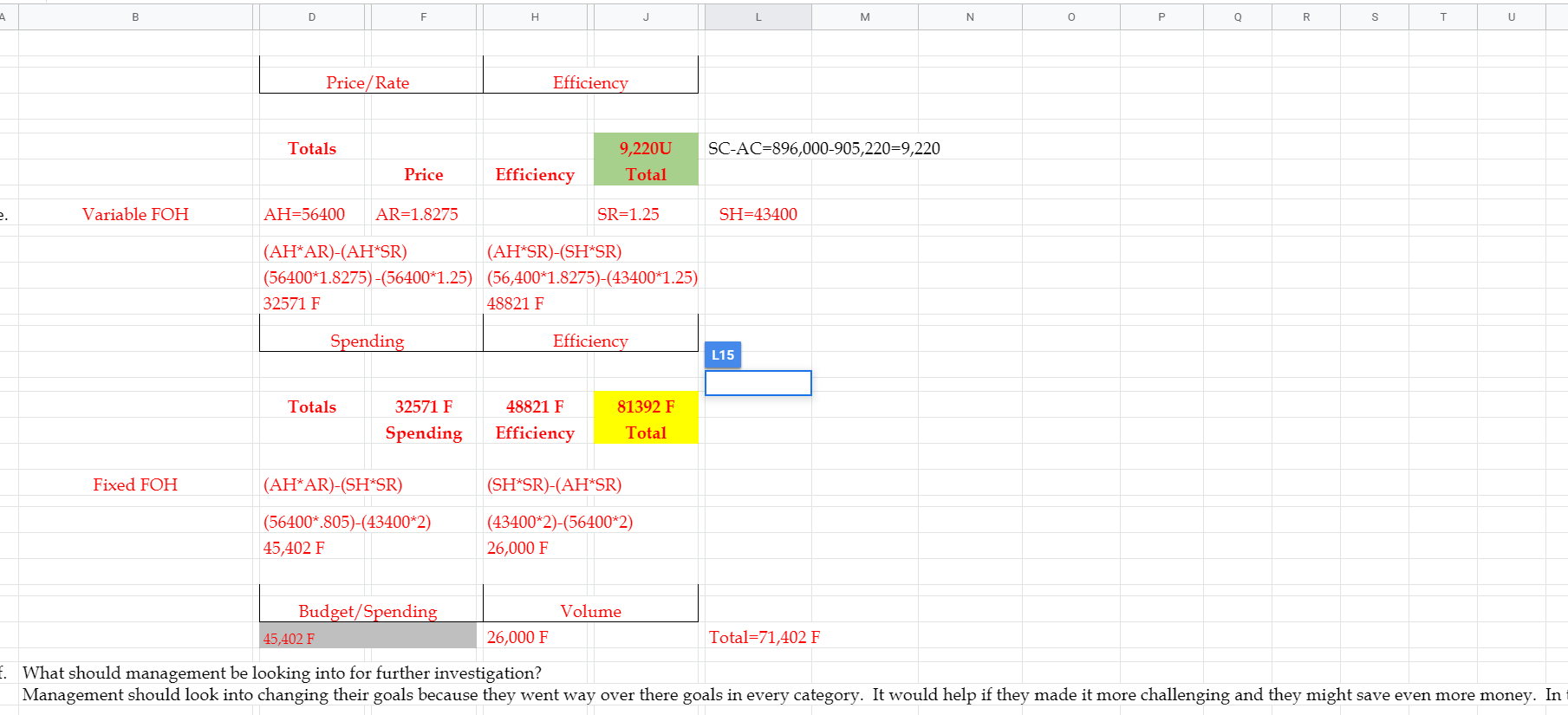

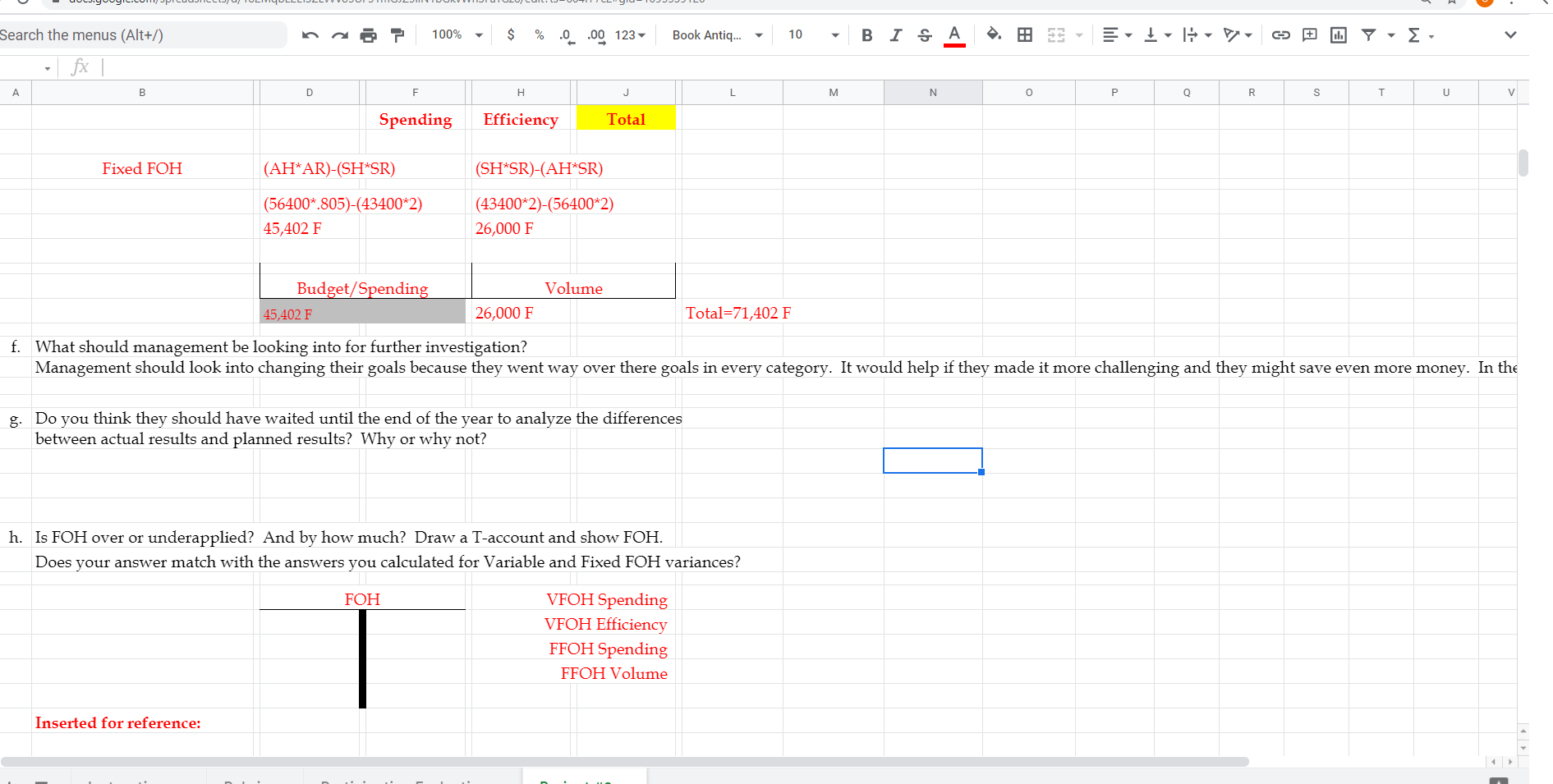

Total sales were $2,029,000 for 40,000 units. Management failed to be able to buy enough direct materials to produce the required units for ending inventory nor to keep the required direct materials on hand for ending inventory requirements due to a shortage of WHAM during the quarter. Total Production for 3rd quarter was 40,000 units. Vaughan uses LIFO inventory method. Regarding WHAM, Vaughan purchased and used 230,000 pounds at a total cost of $163,300. Vaughan used 56,400 DLH (direct labor hours) to make the 40,000 units at a total labor cost of $905,220. Actual Variable FOH was $73,100 and actual Fixed FOH was $32,200. Even though Production ended up being 40,000 units, the cash borrowings indicated by the static budget dictated that Vaughan borrow money ($2,000) on the last day of July and they did so. They also paid it back at the end of the September as budgeted. Selling and Administrative expenses totaled $579,000. $239,000 was variable and the rest was fixed. We have not covered S&A variances, but never the less, the difference between what actually occurred and what should have happened (the flexible budget) can still be illuminating. (a) Prepare a standard cost card for a widget. (b) Prepare an flexible budget performance report comparing actual production/ sales to a flexible budget of such sales/costs (Like #2 on the top of page 842 in our text) (C) Prepare the direct material variances (price and efficiency/quantity) for each material (d) Prepare the direct labor variances (price/rate and efficiency) (e) Prepare the Variable (spending & efficiency) and Fixed FOH (budget/ spending & volume) variances. (refer to the appendix for the factory overhead variances) (f) What should management be looking into for further investigation? (g) Do you think they should have waited until the end of the quarter to analyze the differences between actual results and planned results? Why or why not? 712TTOTT .11.17 A.11... 1. --- --. 1.1. ----TOIT Flexible Budget and Standard Cost Project a. Standard Cost Card Quantity Cost Total 5 $ 0.70 $ Direct Material WHAM Direct Labor Factory Overhead 1.4 $ 16.00 $ $ 3.50 22.40 2.80 1.4 $ 2.00 Total Cost ($1.25 Variable, $0.75 Fixed) $ 28.70 b. Actual Production and Sales 40,000 $ 2,029,000 Flexible Budget Variance Flexible Budget 40,000 $ 2,000,000 Units Sales 29,000 Variable Costs: Direct Materials WHAM Direct Labor Variable FOH Variable S&A Interest Expense $ 140,000 $ 896,000 $ 70,000 $ 240,000 $ 50 $ 163,300 $ 905,220 $ 73,100 $ 239,000 $ 50 (23,300) (9,220) (3,100) 1,000 $ Contribution Margin $ 653,950 $ 648,330 (5,620) Fixed Costs - FOH Fixed Costs - S&A $ 32,550 $ 333,000 $ 32,200 $ 340,000 350 (7,000) Operating Income $ 288,400 $ 276,130 (17,890) A B D F H J L M Contribution Margin S 653,950 $ 648,330 (5,620) Fixed Costs - FOH Fixed Costs - S&A $ $ 32,550 333,000 $ 32,200 $ 340,000 350 (7,000) Operating Income $ 288,400 $ 276,130 (17,890) Direct Material WHAM SQ=200,000 SR=.070 SC=40,000 AQ=230,000 AC=163,300 AR= 71 Price (SR-AR)XAQ=(.70-71)=2,300 Quantity/Efficiency (SQ-AQ)XSR=200,000-230,00 L15 0=21,000 Totals SC-AC=140,000-163,300=23,300 23,300 Total Price Efficiency d. Direct Labor AH=56,400 SR=16 SC=896,000 AR=16.05 (16-16.05)x56,400=2,820U (56,000-56,400)x16=6,400U Price/Rate Efficiency Totals 9,2200 SC-AC=896,000-905,220=9,220 A B D F . J L M N 0 Q R S T U Price/Rate Efficiency Totals SC-AC=896,000-905,220=9,220 9,2200 Total Price Efficiency e. Variable FOH AH=56400 AR=1.8275 SR=1.25 SH=43400 (AH*AR)-(AH*SR) (AH*SR)-(SH*SR) (56400*1.8275) -(56400*1.25) (56,400*1.8275)-(43400*1.25) 32571 F 48821 F Spending Efficiency L15 Totals 32571 F Spending 48821 F Efficiency 81392 F Total Fixed FOH (AH*AR)-(SH*SR) (SH*SR)-(AH*SR) (56400*.805)-(43400*2) 45,402 F (43400*2)-(56400*2) 26,000 F Volume Budget/Spending 45,402 F 26,000 F Total=71,402 F . What should management be looking into for further investigation? Management should look into changing their goals because they went way over there goals in every category. It would help if they made it more challenging and they might save even more money. In 100% $ % 0.00123 Book Antiq... 10 BIS A 11 CE L. Search the menus (Alt+/) fx | A B F H L M N o Q R S T v Spending Efficiency Total Fixed FOH (AH*AR)-(SH*SR) (SH*SR)-(AH*SR) (56400*.805)-(43400*2) 45,402 F (43400*2)-(56400*2) 26,000 F Volume Budget/Spending 45,402 F 26,000 F Total=71,402 F f. What should management be looking into for further investigation? Management should look into changing their goals because they went way over there goals in every category. It would help if they made it more challenging and they might save even more money. In the g. Do you think they should have waited until the end of the year to analyze the differences between actual results and planned results? Why or why not? h. Is FOH over or underapplied? And by how much? Draw a T-account and show FOH. Does your answer match with the answers you calculated for Variable and Fixed FOH variances? FOH I VFOH Spending VFOH Efficiency FFOH Spending FFOH Volume Inserted for reference: Total sales were $2,029,000 for 40,000 units. Management failed to be able to buy enough direct materials to produce the required units for ending inventory nor to keep the required direct materials on hand for ending inventory requirements due to a shortage of WHAM during the quarter. Total Production for 3rd quarter was 40,000 units. Vaughan uses LIFO inventory method. Regarding WHAM, Vaughan purchased and used 230,000 pounds at a total cost of $163,300. Vaughan used 56,400 DLH (direct labor hours) to make the 40,000 units at a total labor cost of $905,220. Actual Variable FOH was $73,100 and actual Fixed FOH was $32,200. Even though Production ended up being 40,000 units, the cash borrowings indicated by the static budget dictated that Vaughan borrow money ($2,000) on the last day of July and they did so. They also paid it back at the end of the September as budgeted. Selling and Administrative expenses totaled $579,000. $239,000 was variable and the rest was fixed. We have not covered S&A variances, but never the less, the difference between what actually occurred and what should have happened (the flexible budget) can still be illuminating. (a) Prepare a standard cost card for a widget. (b) Prepare an flexible budget performance report comparing actual production/ sales to a flexible budget of such sales/costs (Like #2 on the top of page 842 in our text) (C) Prepare the direct material variances (price and efficiency/quantity) for each material (d) Prepare the direct labor variances (price/rate and efficiency) (e) Prepare the Variable (spending & efficiency) and Fixed FOH (budget/ spending & volume) variances. (refer to the appendix for the factory overhead variances) (f) What should management be looking into for further investigation? (g) Do you think they should have waited until the end of the quarter to analyze the differences between actual results and planned results? Why or why not? 712TTOTT .11.17 A.11... 1. --- --. 1.1. ----TOIT Flexible Budget and Standard Cost Project a. Standard Cost Card Quantity Cost Total 5 $ 0.70 $ Direct Material WHAM Direct Labor Factory Overhead 1.4 $ 16.00 $ $ 3.50 22.40 2.80 1.4 $ 2.00 Total Cost ($1.25 Variable, $0.75 Fixed) $ 28.70 b. Actual Production and Sales 40,000 $ 2,029,000 Flexible Budget Variance Flexible Budget 40,000 $ 2,000,000 Units Sales 29,000 Variable Costs: Direct Materials WHAM Direct Labor Variable FOH Variable S&A Interest Expense $ 140,000 $ 896,000 $ 70,000 $ 240,000 $ 50 $ 163,300 $ 905,220 $ 73,100 $ 239,000 $ 50 (23,300) (9,220) (3,100) 1,000 $ Contribution Margin $ 653,950 $ 648,330 (5,620) Fixed Costs - FOH Fixed Costs - S&A $ 32,550 $ 333,000 $ 32,200 $ 340,000 350 (7,000) Operating Income $ 288,400 $ 276,130 (17,890) A B D F H J L M Contribution Margin S 653,950 $ 648,330 (5,620) Fixed Costs - FOH Fixed Costs - S&A $ $ 32,550 333,000 $ 32,200 $ 340,000 350 (7,000) Operating Income $ 288,400 $ 276,130 (17,890) Direct Material WHAM SQ=200,000 SR=.070 SC=40,000 AQ=230,000 AC=163,300 AR= 71 Price (SR-AR)XAQ=(.70-71)=2,300 Quantity/Efficiency (SQ-AQ)XSR=200,000-230,00 L15 0=21,000 Totals SC-AC=140,000-163,300=23,300 23,300 Total Price Efficiency d. Direct Labor AH=56,400 SR=16 SC=896,000 AR=16.05 (16-16.05)x56,400=2,820U (56,000-56,400)x16=6,400U Price/Rate Efficiency Totals 9,2200 SC-AC=896,000-905,220=9,220 A B D F . J L M N 0 Q R S T U Price/Rate Efficiency Totals SC-AC=896,000-905,220=9,220 9,2200 Total Price Efficiency e. Variable FOH AH=56400 AR=1.8275 SR=1.25 SH=43400 (AH*AR)-(AH*SR) (AH*SR)-(SH*SR) (56400*1.8275) -(56400*1.25) (56,400*1.8275)-(43400*1.25) 32571 F 48821 F Spending Efficiency L15 Totals 32571 F Spending 48821 F Efficiency 81392 F Total Fixed FOH (AH*AR)-(SH*SR) (SH*SR)-(AH*SR) (56400*.805)-(43400*2) 45,402 F (43400*2)-(56400*2) 26,000 F Volume Budget/Spending 45,402 F 26,000 F Total=71,402 F . What should management be looking into for further investigation? Management should look into changing their goals because they went way over there goals in every category. It would help if they made it more challenging and they might save even more money. In 100% $ % 0.00123 Book Antiq... 10 BIS A 11 CE L. Search the menus (Alt+/) fx | A B F H L M N o Q R S T v Spending Efficiency Total Fixed FOH (AH*AR)-(SH*SR) (SH*SR)-(AH*SR) (56400*.805)-(43400*2) 45,402 F (43400*2)-(56400*2) 26,000 F Volume Budget/Spending 45,402 F 26,000 F Total=71,402 F f. What should management be looking into for further investigation? Management should look into changing their goals because they went way over there goals in every category. It would help if they made it more challenging and they might save even more money. In the g. Do you think they should have waited until the end of the year to analyze the differences between actual results and planned results? Why or why not? h. Is FOH over or underapplied? And by how much? Draw a T-account and show FOH. Does your answer match with the answers you calculated for Variable and Fixed FOH variances? FOH I VFOH Spending VFOH Efficiency FFOH Spending FFOH Volume Inserted for reference