Answered step by step

Verified Expert Solution

Question

1 Approved Answer

The first step is to find the value of d and u but im confused about that, can anyone help 2. Consider a 2-period binomial

The first step is to find the value of d and u but im confused about that, can anyone help

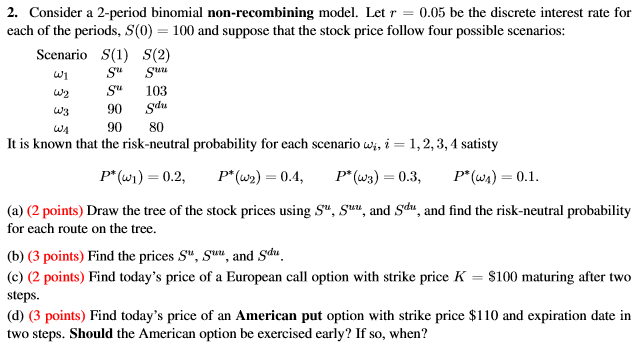

2. Consider a 2-period binomial non-recombining model. Let r- 0.05 be the discrete interest rate for each of the periods, S(0) 100 and suppose that the stock price follow four possible scenarios: Scenario S(1) S(2) 2 S103 W 90 80 It is known that the risk-neutral probability for each scenario ai, i = 1, 2, 3, 4 satisty (a) (2 points) Draw the tree of the stock prices using S"S for each route on the tree. andu, and find the risk-neutral probability (b) (3 points) Find the prices S S and S. (c) (2 points) Find today's price of a European call option with strike price K S100 maturing after two steps. d) (3 points) Find today's price of an American put option with strike price $110 and expiration date in two steps. Should the American option be exercised early? If so, whenStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Enterprise Risk Management Todays Leading Research And Best Practices For Tomorrows Executives

Authors: John R. S. Fraser, Rob Quail, Betty Simkins

1st Edition

1119741483, 978-1119741480