Question

The first-order autoregressive model AR(1) has the form R t = 0+ 1 R t -1+ u t Where R t denotes the continuously compounded

The first-order autoregressive model AR(1) has the form

Rt=0+1Rt-1+ut

Where Rt denotes the continuously compounded return on an asset at time t and ut is the error term at time t.

In the AR(1) model, how do you test mean aversion and reversion in asset returns using the value of 1?

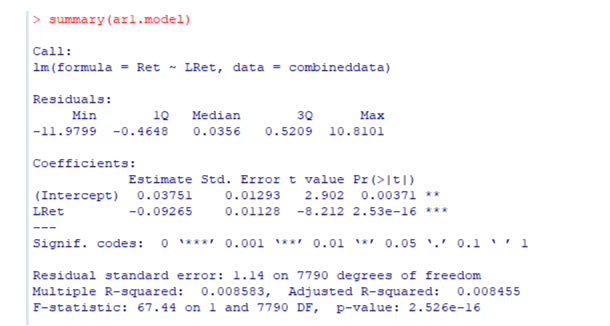

The following represents R linear regression output from estimating the AR(1) model for S&P 500 index using monthly continuously compounded return data over the 5-year period September 2015 September 2021.

Using the estimated results, how do you interpret the estimate of each coefficient and R-squared?

Using the estimation results, what can you say about the market efficiency?

If the this month's return on the S&P 500 index is 5% (0.05), what will be the next month's expected returns predicted by the AR(1) model?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Word Scramble For Auditors And Accounting Professionals Puzzle Book Vocabulary Brain Puzzle Adults And Teens

Authors: Drew Dream

1st Edition

B0B5KVD4CK, 979-8839167865