Answered step by step

Verified Expert Solution

Question

1 Approved Answer

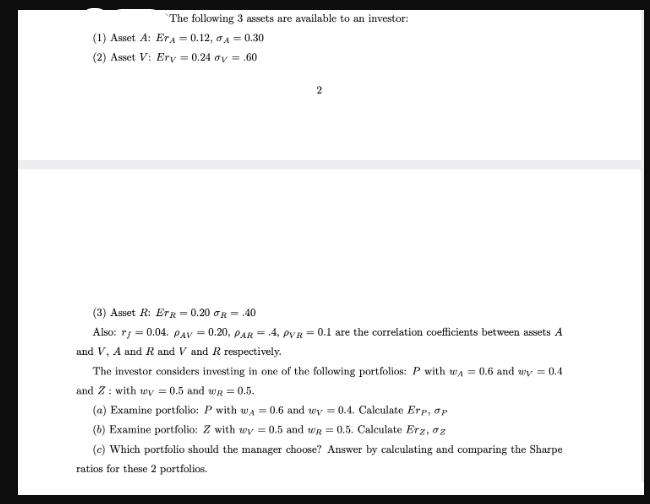

The following 3 assets are available to an investor: (1) Asset A: Er=0.12, A = 0.30 (2) Asset V: Ery = 0.24 oy =

The following 3 assets are available to an investor: (1) Asset A: Er=0.12, A = 0.30 (2) Asset V: Ery = 0.24 oy = .60 2 (3) Asset R: ETR = 0.20 R = .40 Also: ry=0.04. PAV = 0.20, PAR = 4, PVR = 0.1 are the correlation coefficients between assets A and V. A and R and V and R respectively. The investor considers investing in one of the following portfolios: P with w=0.6 and y = 0.4 and Z: with wy 0.5 and wR = 0.5. (a) Examine portfolio: P with wA=0.6 and wy 0.4. Calculate Erp, op (b) Examine portfolio: Z with wy = 0.5 and R = 0.5. Calculate Erz, oz (c) Which portfolio should the manager choose? Answer by calculating and comparing the Sharpe ratios for these 2 portfolios.

Step by Step Solution

★★★★★

3.45 Rating (155 Votes )

There are 3 Steps involved in it

Step: 1

To solve this problem we will first calculate the expected return and the standard deviation of each ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516