Answered step by step

Verified Expert Solution

Question

1 Approved Answer

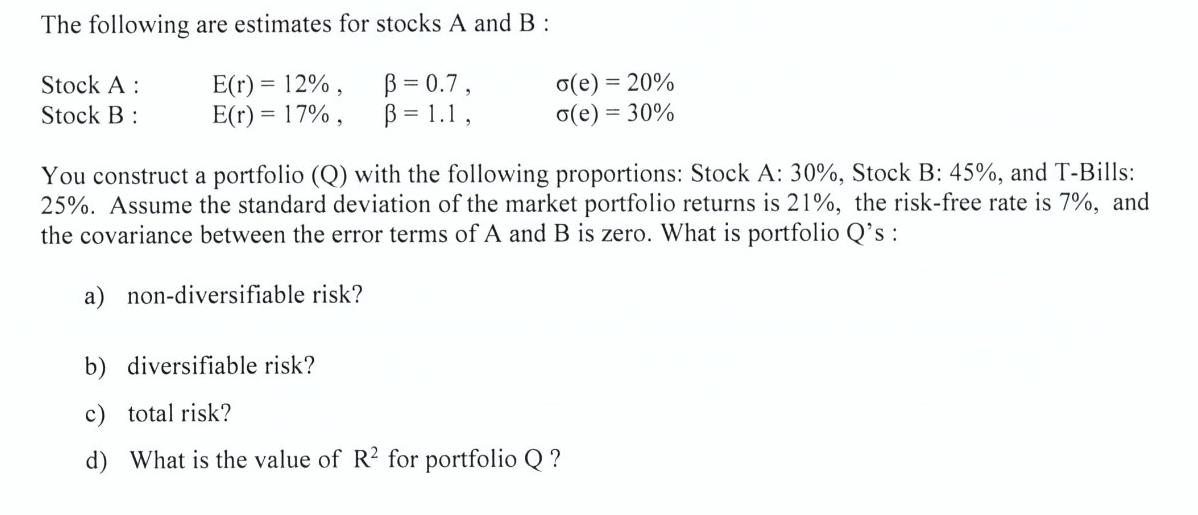

The following are estimates for stocks A and B : Stock A: Stock B: E(r) = 12%, E(r) = 17%, =0.7, = 1.1, (e)

The following are estimates for stocks A and B : Stock A: Stock B: E(r) = 12%, E(r) = 17%, =0.7, = 1.1, (e) = 20% (e) = 30% You construct a portfolio (Q) with the following proportions: Stock A: 30%, Stock B: 45%, and T-Bills: 25%. Assume the standard deviation of the market portfolio returns is 21%, the risk-free rate is 7%, and the covariance between the error terms of A and B is zero. What is portfolio Q's: a) non-diversifiable risk? b) diversifiable risk? total risk? d) What is the value of R for portfolio Q?

Step by Step Solution

★★★★★

3.53 Rating (153 Votes )

There are 3 Steps involved in it

Step: 1

To calculate the portfolio Qs risk components and R we need to use the Capital Asset Pricing Model C...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Financial Management

Authors: Eugene F. Brigham, Joel F. Houston

16th Edition

0357517571, 978-0357517574