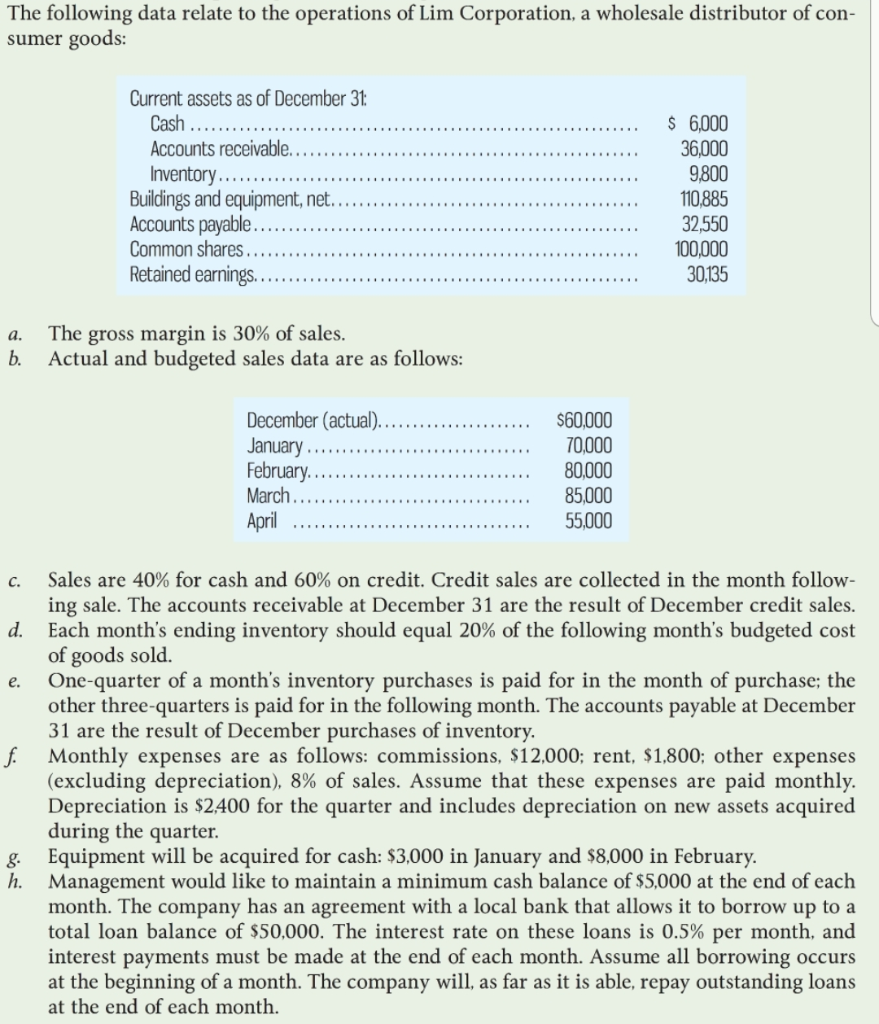

The following data relate to the operations of Lim Corporation, a wholesale distributor of con- sumer goods: Current assets as of December 31: Cash Accounts receivable. Inventory Buildings and equipment, net.. Accounts payable. Common shares Retained earnings $ 6,000 36,000 9,800 110.885 32,550 100,000 30,135 a. b. The gross margin is 30% of sales. Actual and budgeted sales data are as follows: December (actual). January February March April $60,000 70,000 80,000 85,000 55,000 c. e. Sales are 40% for cash and 60% on credit. Credit sales are collected in the month follow- ing sale. The accounts receivable at December 31 are the result of December credit sales. d. Each month's ending inventory should equal 20% of the following month's budgeted cost of goods sold. One-quarter of a month's inventory purchases is paid for in the month of purchase; the other three-quarters is paid for in the following month. The accounts payable at December 31 are the result of December purchases of inventory. f. Monthly expenses are as follows: commissions, $12,000; rent, $1,800; other expenses (excluding depreciation), 8% of sales. Assume that these expenses are paid monthly. Depreciation is $2,400 for the quarter and includes depreciation on new assets acquired during the quarter. g. Equipment will be acquired for cash: $3,000 in January and $8,000 in February. h. Management would like to maintain a minimum cash balance of $5,000 at the end of each month. The company has an agreement with a local bank that allows it to borrow up to a total loan balance of $50,000. The interest rate on these loans is 0.5% per month, and interest payments must be made at the end of each month. Assume all borrowing occurs at the beginning of a month. The company will, as far as it is able, repay outstanding loans at the end of each month. The following data relate to the operations of Lim Corporation, a wholesale distributor of con- sumer goods: Current assets as of December 31: Cash Accounts receivable. Inventory Buildings and equipment, net.. Accounts payable. Common shares Retained earnings $ 6,000 36,000 9,800 110.885 32,550 100,000 30,135 a. b. The gross margin is 30% of sales. Actual and budgeted sales data are as follows: December (actual). January February March April $60,000 70,000 80,000 85,000 55,000 c. e. Sales are 40% for cash and 60% on credit. Credit sales are collected in the month follow- ing sale. The accounts receivable at December 31 are the result of December credit sales. d. Each month's ending inventory should equal 20% of the following month's budgeted cost of goods sold. One-quarter of a month's inventory purchases is paid for in the month of purchase; the other three-quarters is paid for in the following month. The accounts payable at December 31 are the result of December purchases of inventory. f. Monthly expenses are as follows: commissions, $12,000; rent, $1,800; other expenses (excluding depreciation), 8% of sales. Assume that these expenses are paid monthly. Depreciation is $2,400 for the quarter and includes depreciation on new assets acquired during the quarter. g. Equipment will be acquired for cash: $3,000 in January and $8,000 in February. h. Management would like to maintain a minimum cash balance of $5,000 at the end of each month. The company has an agreement with a local bank that allows it to borrow up to a total loan balance of $50,000. The interest rate on these loans is 0.5% per month, and interest payments must be made at the end of each month. Assume all borrowing occurs at the beginning of a month. The company will, as far as it is able, repay outstanding loans at the end of each month