Question

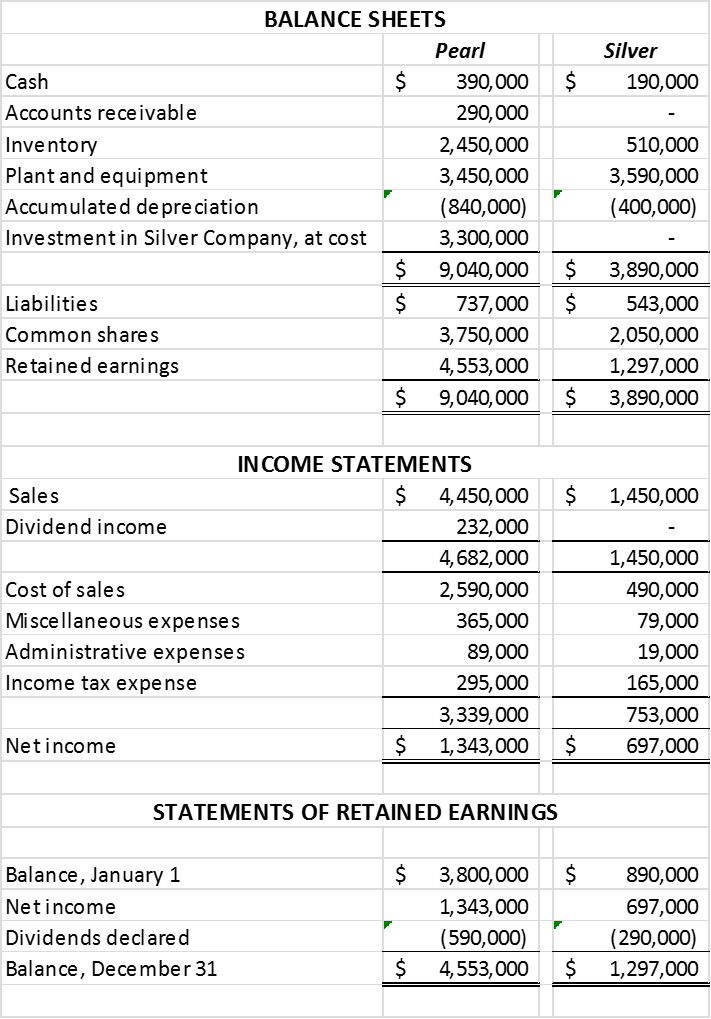

The following financial statements were prepared on December 31, Year 6: Additional Information: Pearl purchased 80% of the outstanding voting shares of Silver for $3,300,000

The following financial statements were prepared on December 31, Year 6:

Additional Information:

Pearl purchased 80% of the outstanding voting shares of Silver for $3,300,000 on July 1, Year 2, at which time Silvers retained earnings were $445,000 and accumulated depreciation was $69,000. The acquisition differential on this date was allocated as follows:

- 20% to undervalued inventory;

- 40% to equipment with a remaining useful life of 8 years;

- the balance to goodwill.

Pearl accounts for its investment in Silver using the cost method and values the non-controlling interest in its subsidiary based on its fair value on the acquisition date, proportionate to the price paid for its controlling interest.

During Year 3, a goodwill impairment loss of $79,000 was recognized, and an impairment test conducted as at December 31, Year 6, indicated that a further loss of $29,000 had occurred.

Amortization expense is to be grouped with cost of goods sold.

Silver owes Pearl $84,000 on December 31, Year 6.

Required:

- Prepare consolidated financial statements on December 31, Year 6.

- Calculate goodwill impairment loss and non-controlling interest on the consolidated income statement for the year ended December 31, Year 6, under the parent company extension theory.

- Calculate goodwill and non-controlling interest on the consolidated balance sheet as at December 31, Year 6, under the parent company extension theory.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Energy Audit And Survey Of Street Light System A Preliminary Report

Authors: Dr. Manoj Dhondiram Patil

1st Edition

B08GBCWWFY, 979-8676818388