Answered step by step

Verified Expert Solution

Question

1 Approved Answer

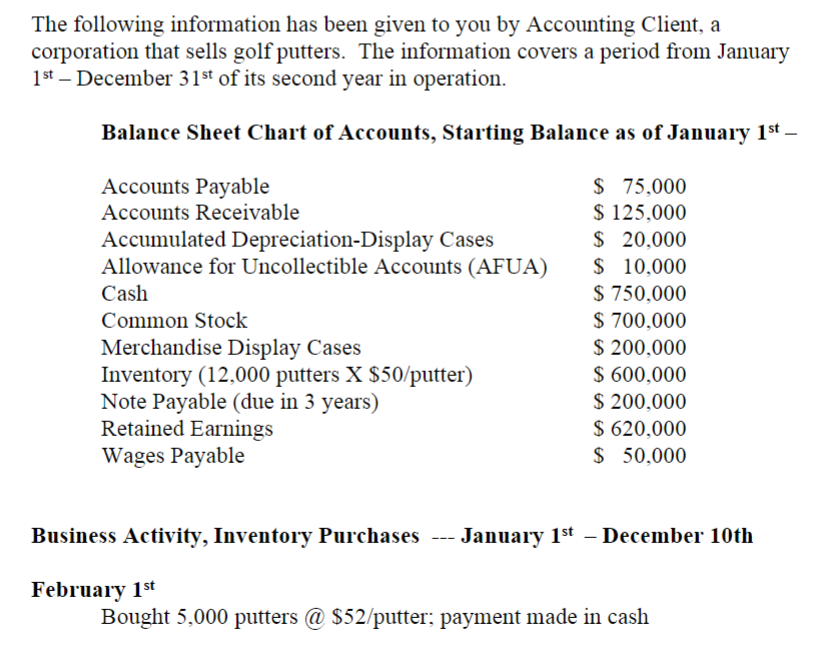

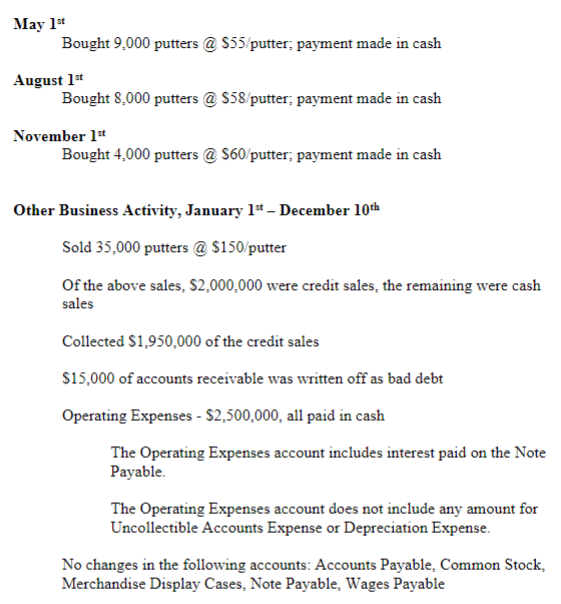

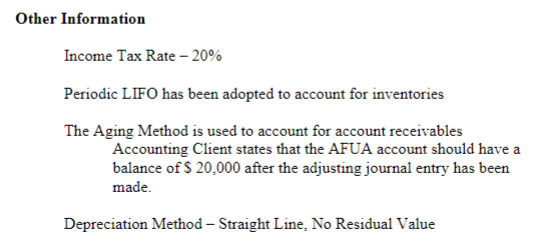

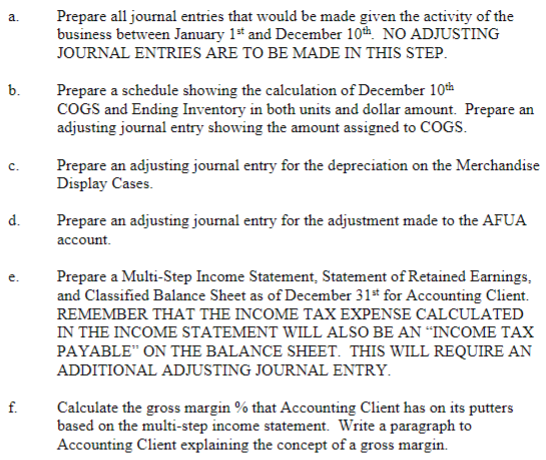

The following information has been given to you by Accounting Client, a corporation that sells golf putters. The information covers a period from January 1st

The following information has been given to you by Accounting Client, a corporation that sells golf putters. The information covers a period from January 1st December 31st of its second year in operation. Balance Sheet Chart of Accounts, Starting Balance as of January 1st Business Activity, Inventory Purchases --- January 1st December 10th February 1st Bought 5,000 putters@ @52/putter; payment made in cash Iay 1st Bought 9,000 putters@ @55/putter; payment made in cash ugust 1st Bought 8,000 putters @ \$58/putter; payment made in cash ovember 1st Bought 4,000 putters@ \$60/putter; payment made in cash ther Business Activity, January 1st - December 10th Sold 35,000 putters @ \$150/putter Of the above sales, $2,000,000 were credit sales, the remaining were cash sales Collected $1,950,000 of the credit sales $15,000 of accounts receivable was written off as bad debt Operating Expenses - $2,500,000, all paid in cash The Operating Expenses account includes interest paid on the Note Payable. The Operating Expenses account does not include any amount for Uncollectible Accounts Expense or Depreciation Expense. No changes in the following accounts: Accounts Payable, Common Stock, Merchandise Display Cases, Note Payable, Wages Payable her Information Income Tax Rate 20% Periodic LIFO has been adopted to account for inventories The Aging Method is used to account for account receivables Accounting Client states that the AFUA account should have a balance of $20,000 after the adjusting journal entry has been made. Depreciation Method - Straight Line, No Residual Value a. Prepare all journal entries that would be made given the activity of the business between January 1st and December 10th. NO ADJUSTING JOURNAL ENTRIES ARE TO BE MADE IN THIS STEP. b. Prepare a schedule showing the calculation of December 10th COGS and Ending Inventory in both units and dollar amount. Prepare an adjusting journal entry showing the amount assigned to COGS. c. Prepare an adjusting journal entry for the depreciation on the Merchandise Display Cases. d. Prepare an adjusting journal entry for the adjustment made to the AFUA account. e. Prepare a Multi-Step Income Statement, Statement of Retained Earnings, and Classified Balance Sheet as of December 31st for Accounting Client. REMEMBER THAT THE INCOME TAX EXPENSE CALCULATED IN THE INCOME STATEMENT WILL ALSO BE AN "INCOME TAX PAYABLE" ON THE BALANCE SHEET. THIS WILL REQUIRE AN ADDITIONAL ADJUSTING JOURNAL ENTRY. Calculate the gross margin % that Accounting Client has on its putters based on the multi-step income statement. Write a paragraph to Accounting Client explaining the concept of a gross margin. The following information has been given to you by Accounting Client, a corporation that sells golf putters. The information covers a period from January 1st December 31st of its second year in operation. Balance Sheet Chart of Accounts, Starting Balance as of January 1st Business Activity, Inventory Purchases --- January 1st December 10th February 1st Bought 5,000 putters@ @52/putter; payment made in cash Iay 1st Bought 9,000 putters@ @55/putter; payment made in cash ugust 1st Bought 8,000 putters @ \$58/putter; payment made in cash ovember 1st Bought 4,000 putters@ \$60/putter; payment made in cash ther Business Activity, January 1st - December 10th Sold 35,000 putters @ \$150/putter Of the above sales, $2,000,000 were credit sales, the remaining were cash sales Collected $1,950,000 of the credit sales $15,000 of accounts receivable was written off as bad debt Operating Expenses - $2,500,000, all paid in cash The Operating Expenses account includes interest paid on the Note Payable. The Operating Expenses account does not include any amount for Uncollectible Accounts Expense or Depreciation Expense. No changes in the following accounts: Accounts Payable, Common Stock, Merchandise Display Cases, Note Payable, Wages Payable her Information Income Tax Rate 20% Periodic LIFO has been adopted to account for inventories The Aging Method is used to account for account receivables Accounting Client states that the AFUA account should have a balance of $20,000 after the adjusting journal entry has been made. Depreciation Method - Straight Line, No Residual Value a. Prepare all journal entries that would be made given the activity of the business between January 1st and December 10th. NO ADJUSTING JOURNAL ENTRIES ARE TO BE MADE IN THIS STEP. b. Prepare a schedule showing the calculation of December 10th COGS and Ending Inventory in both units and dollar amount. Prepare an adjusting journal entry showing the amount assigned to COGS. c. Prepare an adjusting journal entry for the depreciation on the Merchandise Display Cases. d. Prepare an adjusting journal entry for the adjustment made to the AFUA account. e. Prepare a Multi-Step Income Statement, Statement of Retained Earnings, and Classified Balance Sheet as of December 31st for Accounting Client. REMEMBER THAT THE INCOME TAX EXPENSE CALCULATED IN THE INCOME STATEMENT WILL ALSO BE AN "INCOME TAX PAYABLE" ON THE BALANCE SHEET. THIS WILL REQUIRE AN ADDITIONAL ADJUSTING JOURNAL ENTRY. Calculate the gross margin % that Accounting Client has on its putters based on the multi-step income statement. Write a paragraph to Accounting Client explaining the concept of a gross margin

The following information has been given to you by Accounting Client, a corporation that sells golf putters. The information covers a period from January 1st December 31st of its second year in operation. Balance Sheet Chart of Accounts, Starting Balance as of January 1st Business Activity, Inventory Purchases --- January 1st December 10th February 1st Bought 5,000 putters@ @52/putter; payment made in cash Iay 1st Bought 9,000 putters@ @55/putter; payment made in cash ugust 1st Bought 8,000 putters @ \$58/putter; payment made in cash ovember 1st Bought 4,000 putters@ \$60/putter; payment made in cash ther Business Activity, January 1st - December 10th Sold 35,000 putters @ \$150/putter Of the above sales, $2,000,000 were credit sales, the remaining were cash sales Collected $1,950,000 of the credit sales $15,000 of accounts receivable was written off as bad debt Operating Expenses - $2,500,000, all paid in cash The Operating Expenses account includes interest paid on the Note Payable. The Operating Expenses account does not include any amount for Uncollectible Accounts Expense or Depreciation Expense. No changes in the following accounts: Accounts Payable, Common Stock, Merchandise Display Cases, Note Payable, Wages Payable her Information Income Tax Rate 20% Periodic LIFO has been adopted to account for inventories The Aging Method is used to account for account receivables Accounting Client states that the AFUA account should have a balance of $20,000 after the adjusting journal entry has been made. Depreciation Method - Straight Line, No Residual Value a. Prepare all journal entries that would be made given the activity of the business between January 1st and December 10th. NO ADJUSTING JOURNAL ENTRIES ARE TO BE MADE IN THIS STEP. b. Prepare a schedule showing the calculation of December 10th COGS and Ending Inventory in both units and dollar amount. Prepare an adjusting journal entry showing the amount assigned to COGS. c. Prepare an adjusting journal entry for the depreciation on the Merchandise Display Cases. d. Prepare an adjusting journal entry for the adjustment made to the AFUA account. e. Prepare a Multi-Step Income Statement, Statement of Retained Earnings, and Classified Balance Sheet as of December 31st for Accounting Client. REMEMBER THAT THE INCOME TAX EXPENSE CALCULATED IN THE INCOME STATEMENT WILL ALSO BE AN "INCOME TAX PAYABLE" ON THE BALANCE SHEET. THIS WILL REQUIRE AN ADDITIONAL ADJUSTING JOURNAL ENTRY. Calculate the gross margin % that Accounting Client has on its putters based on the multi-step income statement. Write a paragraph to Accounting Client explaining the concept of a gross margin. The following information has been given to you by Accounting Client, a corporation that sells golf putters. The information covers a period from January 1st December 31st of its second year in operation. Balance Sheet Chart of Accounts, Starting Balance as of January 1st Business Activity, Inventory Purchases --- January 1st December 10th February 1st Bought 5,000 putters@ @52/putter; payment made in cash Iay 1st Bought 9,000 putters@ @55/putter; payment made in cash ugust 1st Bought 8,000 putters @ \$58/putter; payment made in cash ovember 1st Bought 4,000 putters@ \$60/putter; payment made in cash ther Business Activity, January 1st - December 10th Sold 35,000 putters @ \$150/putter Of the above sales, $2,000,000 were credit sales, the remaining were cash sales Collected $1,950,000 of the credit sales $15,000 of accounts receivable was written off as bad debt Operating Expenses - $2,500,000, all paid in cash The Operating Expenses account includes interest paid on the Note Payable. The Operating Expenses account does not include any amount for Uncollectible Accounts Expense or Depreciation Expense. No changes in the following accounts: Accounts Payable, Common Stock, Merchandise Display Cases, Note Payable, Wages Payable her Information Income Tax Rate 20% Periodic LIFO has been adopted to account for inventories The Aging Method is used to account for account receivables Accounting Client states that the AFUA account should have a balance of $20,000 after the adjusting journal entry has been made. Depreciation Method - Straight Line, No Residual Value a. Prepare all journal entries that would be made given the activity of the business between January 1st and December 10th. NO ADJUSTING JOURNAL ENTRIES ARE TO BE MADE IN THIS STEP. b. Prepare a schedule showing the calculation of December 10th COGS and Ending Inventory in both units and dollar amount. Prepare an adjusting journal entry showing the amount assigned to COGS. c. Prepare an adjusting journal entry for the depreciation on the Merchandise Display Cases. d. Prepare an adjusting journal entry for the adjustment made to the AFUA account. e. Prepare a Multi-Step Income Statement, Statement of Retained Earnings, and Classified Balance Sheet as of December 31st for Accounting Client. REMEMBER THAT THE INCOME TAX EXPENSE CALCULATED IN THE INCOME STATEMENT WILL ALSO BE AN "INCOME TAX PAYABLE" ON THE BALANCE SHEET. THIS WILL REQUIRE AN ADDITIONAL ADJUSTING JOURNAL ENTRY. Calculate the gross margin % that Accounting Client has on its putters based on the multi-step income statement. Write a paragraph to Accounting Client explaining the concept of a gross margin Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managefirst Managerial Accounting With Pencil/Paper Exam

Authors: National Restaurant Association

1st Edition

0132283417, 978-0132283410