Answered step by step

Verified Expert Solution

Question

1 Approved Answer

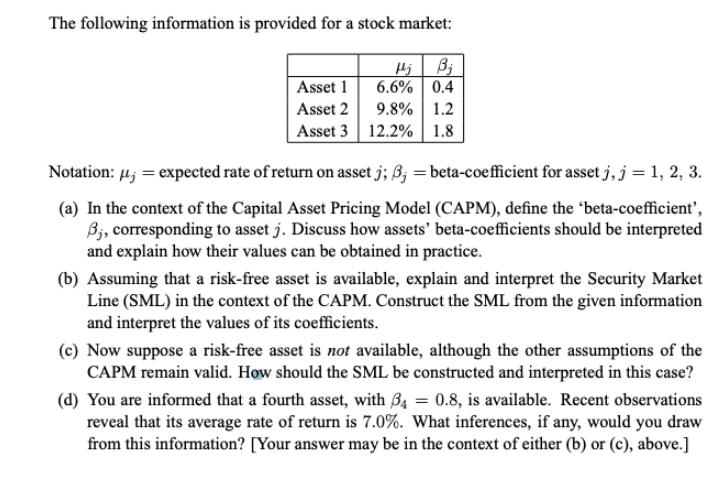

The following information is provided for a stock market: HjBj 6.6% 0.4 9.8% 1.2 12.2% 1.8 Asset 1 Asset 2 Asset 3 Notation: =

The following information is provided for a stock market: HjBj 6.6% 0.4 9.8% 1.2 12.2% 1.8 Asset 1 Asset 2 Asset 3 Notation: = expected rate of return on asset j; 3; = beta-coefficient for asset j, j = 1, 2, 3. (a) In the context of the Capital Asset Pricing Model (CAPM), define the 'beta-coefficient', 3, corresponding to asset j. Discuss how assets' beta-coefficients should be interpreted and explain how their values can be obtained in practice. (b) Assuming that a risk-free asset is available, explain and interpret the Security Market Line (SML) in the context of the CAPM. Construct the SML from the given information and interpret the values of its coefficients. (c) Now suppose a risk-free asset is not available, although the other assumptions of the CAPM remain valid. How should the SML be constructed and interpreted in this case? (d) You are informed that a fourth asset, with 34 = 0.8, is available. Recent observations reveal that its average rate of return is 7.0%. What inferences, if any, would you draw from this information? [Your answer may be in the context of either (b) or (c), above.]

Step by Step Solution

★★★★★

3.48 Rating (151 Votes )

There are 3 Steps involved in it

Step: 1

SOLUTION a In the context of the Capital Asset Pricing Model CAPM the betacoefficient corresponding to asset j measures the sensitivity of the assets returns to the overall market returns It quantifie...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516