Question

The following information pertains to Zhifang who is a UK resident for the tax year 2020/21: Zhifang was paid an annual salary of 52,000 by

The following information pertains to Zhifang who is a UK resident for the tax year 2020/21:

- Zhifang was paid an annual salary of £52,000 by her employer, a private equity firm that invests in renewable energy companies within emerging markets. Her employer had also deducted income tax of £10,250 from Zhifang’s salary under the PAYE system.

- Zhifang received two bonus payments from her employer in recognition of her outstanding performance as follows:

- First bonus payment amounted to £1,900 paid on 30 September 2020.

- Second bonus payment of £2,100 was paid on 31 March 2021.

- Zhifang was provided with a diesel-powered car with a list price of £32,000. Zhifang’s employer had however paid £30,000 for the car after obtaining a discount from the car dealership because of their continued custom. Zhifang also contributed £4,000 towards the cost of this car. The car had an official carbon dioxide emission rate of 120g/km. Zhifang used the car both for private and work use and all fuel was provided by her employer.

- Zhifang was provided with accommodation by her employer since the beginning of her employment on 1 January 2017. Her employer had initially acquired this house on 1 November 2015 for £190,000. The market value of this property was estimated at £200,000 following a valuation conducted on 1 January 2017. The annual value of the property is £5,000.

- Zhifang has a home theatre system provided by her employer for private enjoyment. This equipment had cost her employer £5,000 when it was acquired on 1 January 2017.

- Zhifang’s employer also paid £500 to a local golf club so that she can enjoy her weekends when she is off work.

- Zhifang also took three loans from her employer that were in existence during the entire tax year, as follows:

- An interest-free loan of £20,000 which Zhifang used to purchase a vintage car.

- A Loan of £3,000 to buy an annual ticket for Manchester United home games, taken at an interest rate of 1.5% p.a.

- An interest-free loan of £3,000 to purchase an equipment she needed for her job.

- Zhifang earned annual rental income of £4,800 from a property located in Liverpool, out of which she spent £700 to repair a section of the property’s roof that had been damaged by strong winds. Zhifang also paid £150 with respect to insurance for this property during the year.

Additional information:

- Zhifang is a very philanthropic person and she donated £3,000 to a charity through her employer’s gift aid scheme on 31 January 2021.

- Zhifang received a premium bond prize of £270 on 1 April 2021.

- Zhifang received net interest of £2,000 from her savings account with a local bank, and gross dividends of £1,000. Both amounts were deposited into her bank account on 3 April 2021.

Required: Calculate the income tax payable by Zhifang for the tax year 2020/21 (Assume an official rate of interest of 2.25%).

[TOTAL: 20 MARKS]

IF NEEDED, below is tax rate and allowances information:

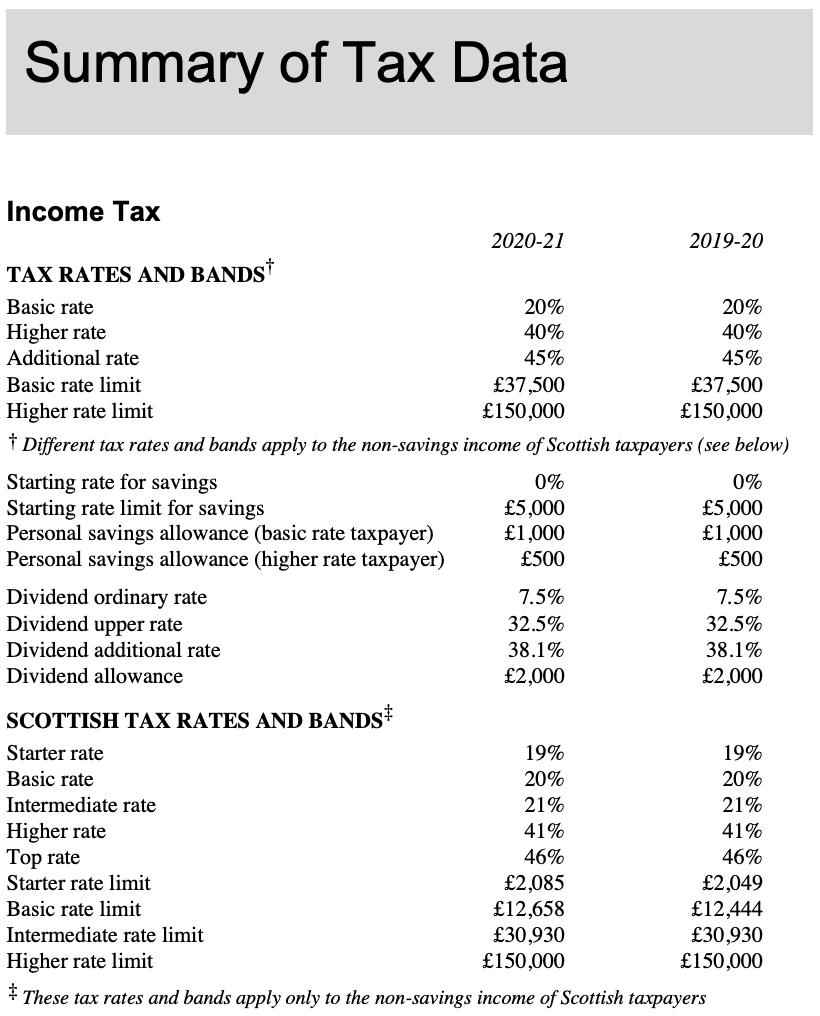

Summary of Tax Data Income Tax TAX RATES AND BANDS Basic rate Higher rate Additional rate Basic rate limit Higher rate limit Dividend ordinary rate Dividend upper rate Dividend additional rate Dividend allowance SCOTTISH TAX RATES AND BANDS Starter rate Basic rate Intermediate rate Higher rate Top rate Starter rate limit Basic rate limit 2020-21 37,500 150,000 Different tax rates and bands apply to the non-savings income of Scottish taxpayers (see below) Starting rate for savings Starting rate limit for savings Personal savings allowance (basic rate taxpayer) Personal savings allowance (higher rate taxpayer) Intermediate rate limit Higher rate limit 20% 40% 45% 37,500 150,000 0% 5,000 1,000 500 7.5% 32.5% 38.1% 2,000 19% 20% 21% 41% 46% 2019-20 2,085 12,658 30,930 150,000 20% 40% 45% 0% 5,000 1,000 500 7.5% 32.5% 38.1% 2,000 These tax rates and bands apply only to the non-savings income of Scottish taxpayers 19% 20% 21% 41% 46% 2,049 12,444 30,930 150,000

Step by Step Solution

3.30 Rating (156 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Document Format ( 2 attachments)

6362800377085_221748.pdf

180 KBs PDF File

6362800377085_221748.docx

120 KBs Word File

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting

Authors: LibbyShort

7th Edition

78111021, 978-0078111020