Question

The following option prices were observed for a stock (no n- dividend) for July 6 of a particular year. The stock is priced today at

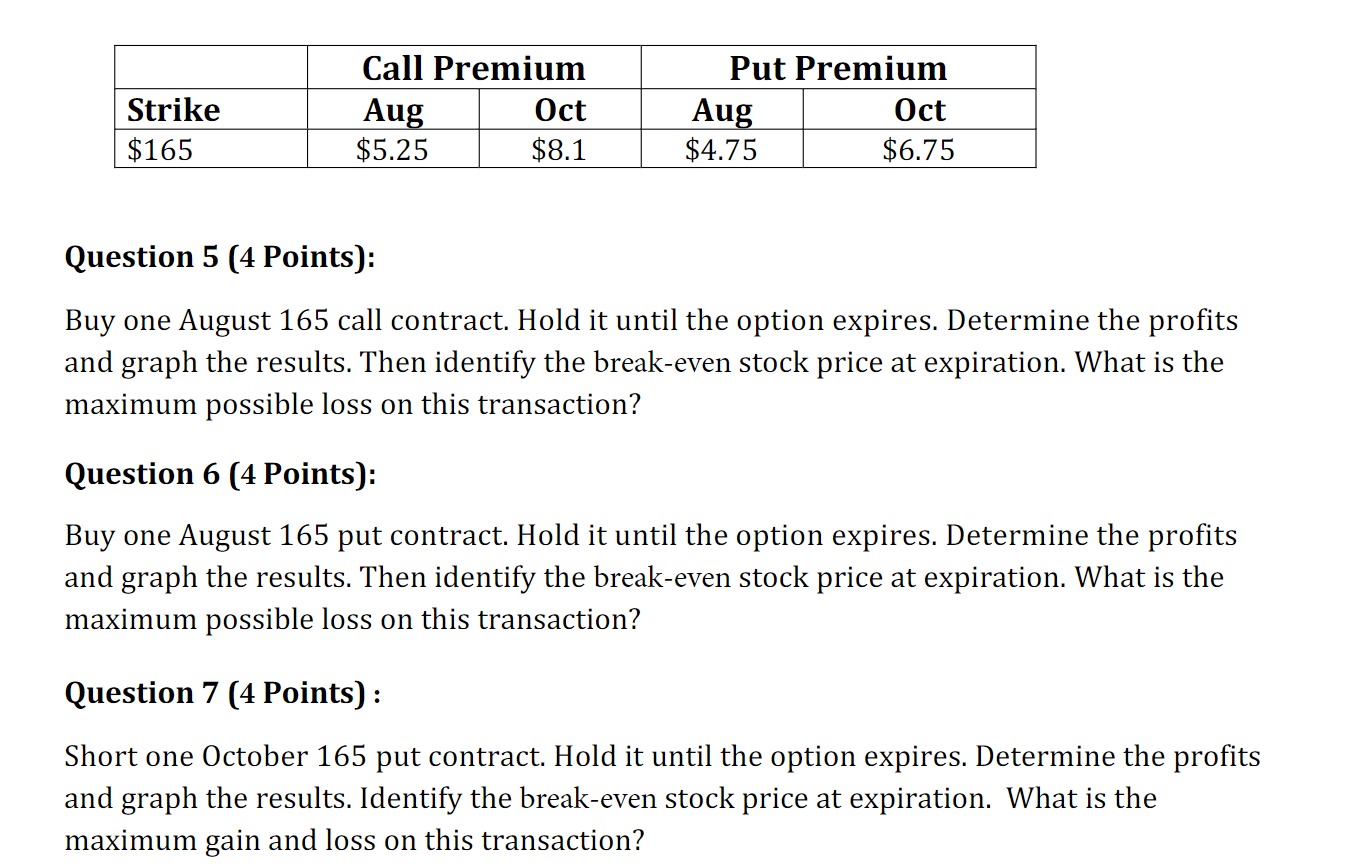

The following option prices were observed for a stock (no n- dividend) for July 6 of a particular year. The stock is priced today at $165.13/ s hare . Assume interest rate=0% The options are European. In the following problems, determine the profits for possible stock prices of $150, 155, 160, 165, 170, 175, and 180. Answer any other questions as requested.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Volatility Surface A Practitioner's Guide

Authors: Jim Gatheral

1st Edition

0471792519, 978-0471792512