Answered step by step

Verified Expert Solution

Question

1 Approved Answer

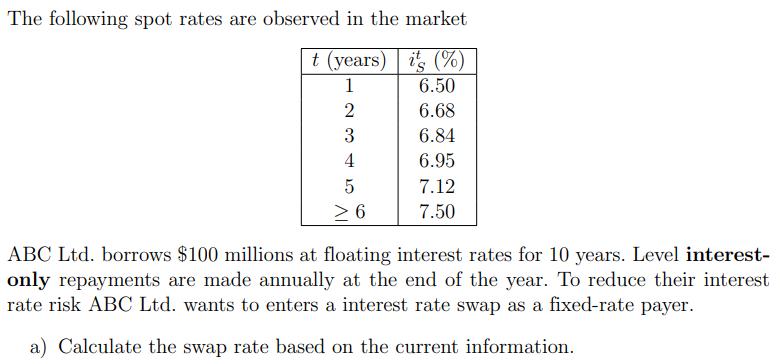

The following spot rates are observed in the market t (years) is (%) 1 6.50 2 6.68 3 6.84 4 6.95 5 7.12 6

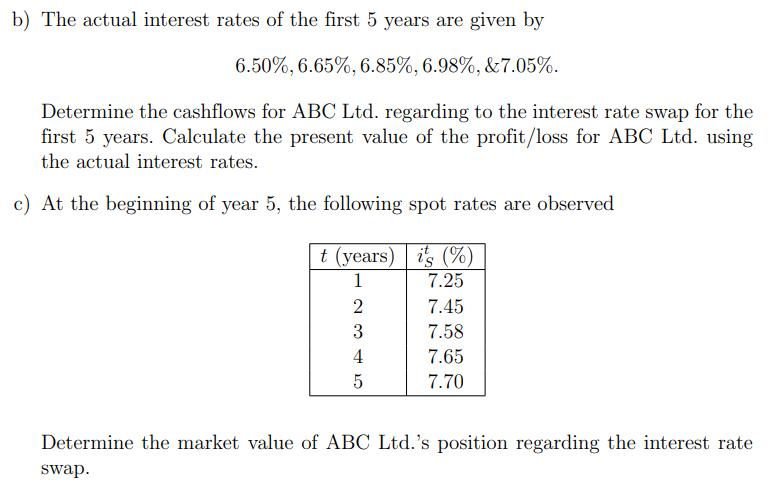

The following spot rates are observed in the market t (years) is (%) 1 6.50 2 6.68 3 6.84 4 6.95 5 7.12 6 7.50 ABC Ltd. borrows $100 millions at floating interest rates for 10 years. Level interest- only repayments are made annually at the end of the year. To reduce their interest rate risk ABC Ltd. wants to enters a interest rate swap as a fixed-rate payer. a) Calculate the swap rate based on the current information. b) The actual interest rates of the first 5 years are given by 6.50%, 6.65%, 6.85%, 6.98%, &7.05%. Determine the cashflows for ABC Ltd. regarding to the interest rate swap for the first 5 years. Calculate the present value of the profit/loss for ABC Ltd. using the actual interest rates. c) At the beginning of year 5, the following spot rates are observed t (years) is (%) 1 7.25 2 7.45 3 7.58 4 7.65 5 7.70 Determine the market value of ABC Ltd.'s position regarding the interest rate swap.

Step by Step Solution

★★★★★

3.49 Rating (152 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Financial Management

Authors: James Van Horne, John Wachowicz

13th Revised Edition

978-0273713630, 273713639