Question

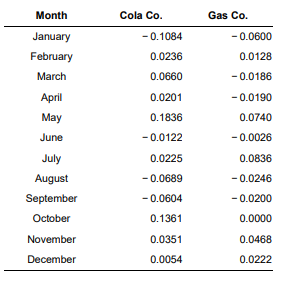

The following table contains monthly returns for Cola Co. and Gas Co. for 2010 (the returns are shown in decimal form, i.e., 0.035 is 3.5%).

The following table contains monthly returns for Cola Co. and Gas Co. for 2010 (the returns are shown in decimal form, i.e., 0.035 is 3.5%).

Using this table and the fact that Cola Co. and Gas Co. have a correlation of 0.6084, calculate the volatility (standard deviation) of a portfolio that is 55% invested in Cola Co. stock and 45% invested in Gas Co. stock. Calculate the volatility by:

a. Using this formula:

b. Calculating the monthly returns of the portfolio and computing its volatility directly.

Month Cola Co. Gas Co. -0.0600 January February March - 0.1084 0.0236 0.0660 0.0128 -0.0186 0.0201 -0.0190 April May 0.0740 June -0.0026 0.1836 -0.0122 0.0225 -0.0689 0.0836 -0.0246 -0.0200 July August September October November December -0.0604 0.1361 0.0000 0.0351 0.0468 0.0054 0.0222 (cy) as (ta)as (28 day) wo92mm2 + (2x) as{m+ z(ta) as m = (07)JenStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Truth About Buying Annuities Annuities Can Make Or Break Your Retirement

Authors: Steve Weisman

1st Edition

0132353083,0132701162