Answered step by step

Verified Expert Solution

Question

1 Approved Answer

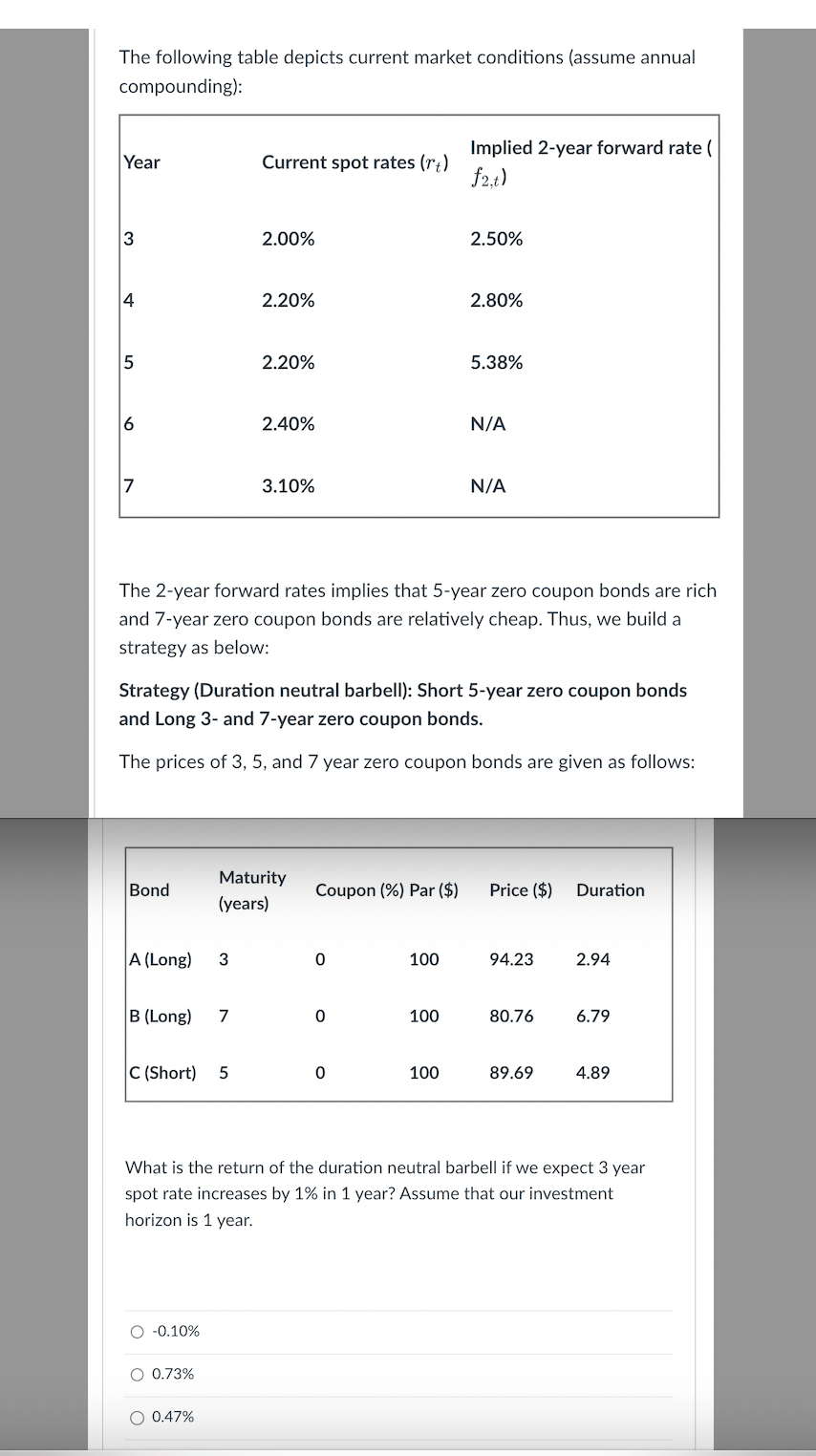

The following table depicts current market conditions ( assume annual compounding ) : The 2 - year forward rates implies that 5 - year zero

The following table depicts current market conditions assume annual compounding: The year forward rates implies that year zero coupon bonds are rich and year zero coupon bonds are relatively cheap. Thus, we build a strategy as below: Strategy Duration neutral barbell: Short year zero coupon bonds and Long and year zero coupon bonds. The prices of and year zero coupon bonds are given as follows: What is the return of the duration neutral barbell if we expect year spot rate increases by in year? Assume that our investment horizon is year.

The following table depicts current market conditions assume annual

compounding:

The year forward rates implies that year zero coupon bonds are rich

and year zero coupon bonds are relatively cheap. Thus, we build a

strategy as below:

Strategy Duration neutral barbell: Short year zero coupon bonds

and Long and year zero coupon bonds.

The prices of and year zero coupon bonds are given as follows:

What is the return of the duration neutral barbell if we expect year

spot rate increases by in year? Assume that our investment

horizon is year.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Commodity Trade And Finance

Authors: Michael Tamvakis

2nd Edition

041573245X, 978-0415732451