Answered step by step

Verified Expert Solution

Question

1 Approved Answer

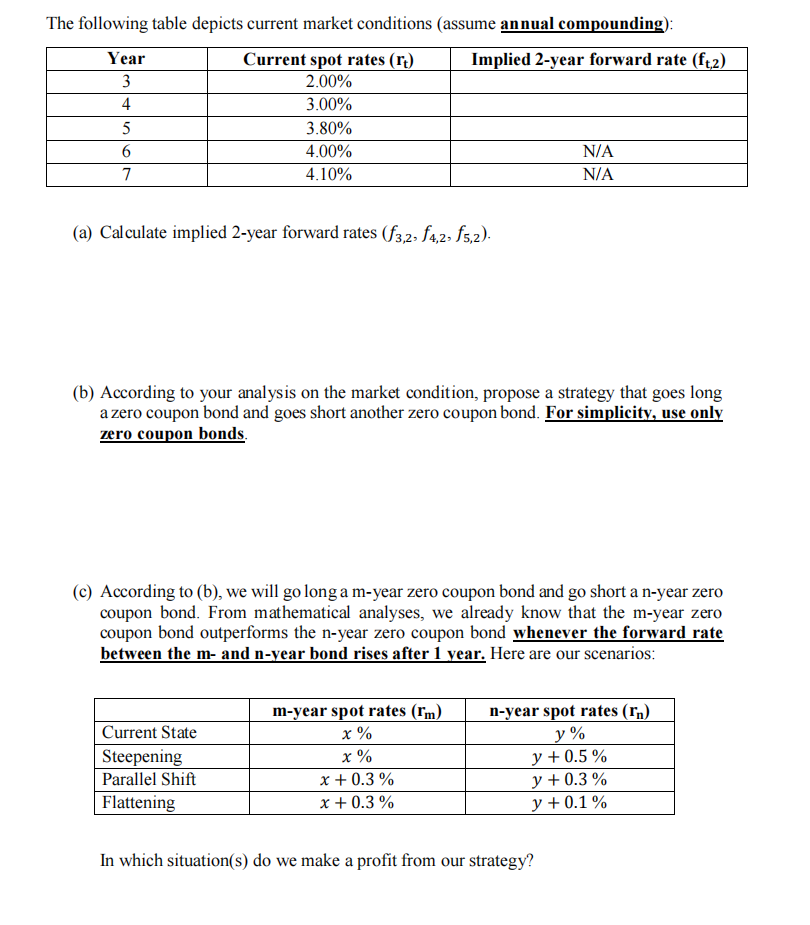

The following table depicts current market conditions (assume annual compounding): Year Current spot rates (ru) Implied 2-year forward rate (ft,2) 3 2.00% 4 3.00% 5

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Candlestick Charts Training For Dummies

Authors: Walletter Books

1st Edition

979-8727316689