Answered step by step

Verified Expert Solution

Question

1 Approved Answer

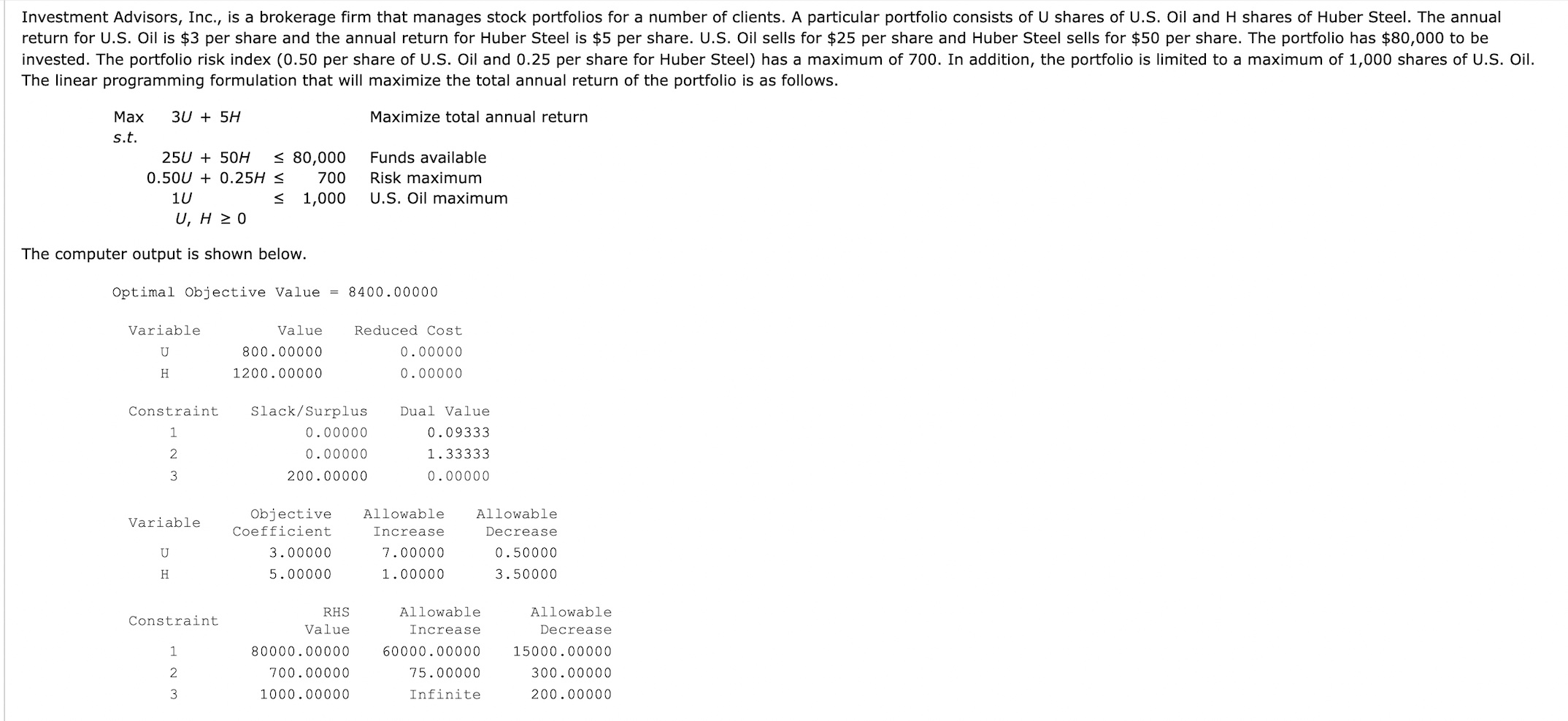

The linear programming formulation that will maximize the total annual return of the portfolio is as follows. Max 3 U + 5 H Maximize total

The linear programming formulation that will maximize the total annual return of the portfolio is as follows.

Max Maximize total annual return

Funds available

Risk maximum

Oil maximum

The computer output is shown in picture.

a What is the optimal solution, and what is the value of the total annual return in $

U

H

estimated annual return $

b Which constraints are binding? What is your interpretation of these constraints in terms of the problem? Select all that apply.

a Constraint All funds available are being utilized.

b Constraint The maximum permissible risk is being incurred.

c Constraint All available shares of US Oil are being purchased.

d None of the constraints are binding.

cWhat are the dual values for the constraints? Interpret each. Round your answers to two decimal places.

constraint

a Constraint has a dual value of If an additional dollar is added to the available funds, the total annual return is predicted to increase by $

b Constraint has a dual value of If an additional dollar is added to the available funds, the total annual return is predicted to increase by $

c Constraint has a slack of $ Additional dollars added to the available funds will not improve the total annual return.

d Constraint has a dual value of If an additional dollar is added to the available funds, the total annual return is predicted to increase by $

eConstraint has a dual value of If an additional dollar is added to the available funds, the total annual return is predicted to increase by $

constraint

a Constraint has a dual value of If the risk index is increased by the total annual return is predicted to increase by $

b Constraint has a dual value of If the risk index is increased by the total annual return is predicted to increase by $

c Constraint has a slack of Allowing additional risk will not improve the total annual return.

d Constraint has a dual value of If the risk index is increased by the total annual return is predicted to increase by $

e Constraint has a dual value of If the risk index is increased by the total annual return is predicted to increase by $

constraint

a Constraint has a dual value of If the maximum number of shares of US Oil is increased by the total annual return is predicted to increase by $

b Constraint has a dual value of If the maximum number of shares of US Oil is increased by the total annual return is predicted to increase by $

c Constraint has a slack of shares. Raising the maximum number of shares of US Oil will not improve the total annual return.

d Constraint has a dual value of If the maximum number of shares of US Oil is increased by the total annual return is predicted to increase by $

e Constraint has a dual value of If the maximum number of shares of US Oil is increased by the total annual return is predicted to increase by $

dWould it be beneficial to increase the maximum amount invested in US Oil? Why or why not?

a Yes, each additional share increases the profit by $

b Yes, each additional share increases the profit by $

c Yes, each additional share increases the profit by $

d No increasing the maximum shares does not affect the optimal value.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Machine Learning And Knowledge Discovery In Databases European Conference Ecml Pkdd 2019 Wurzburg Germany September 16 20 2019 Proceedings Part 2 Lnai 11907

Authors: Ulf Brefeld ,Elisa Fromont ,Andreas Hotho ,Arno Knobbe ,Marloes Maathuis ,Celine Robardet

1st Edition

3030461467, 978-3030461461