Answered step by step

Verified Expert Solution

Question

1 Approved Answer

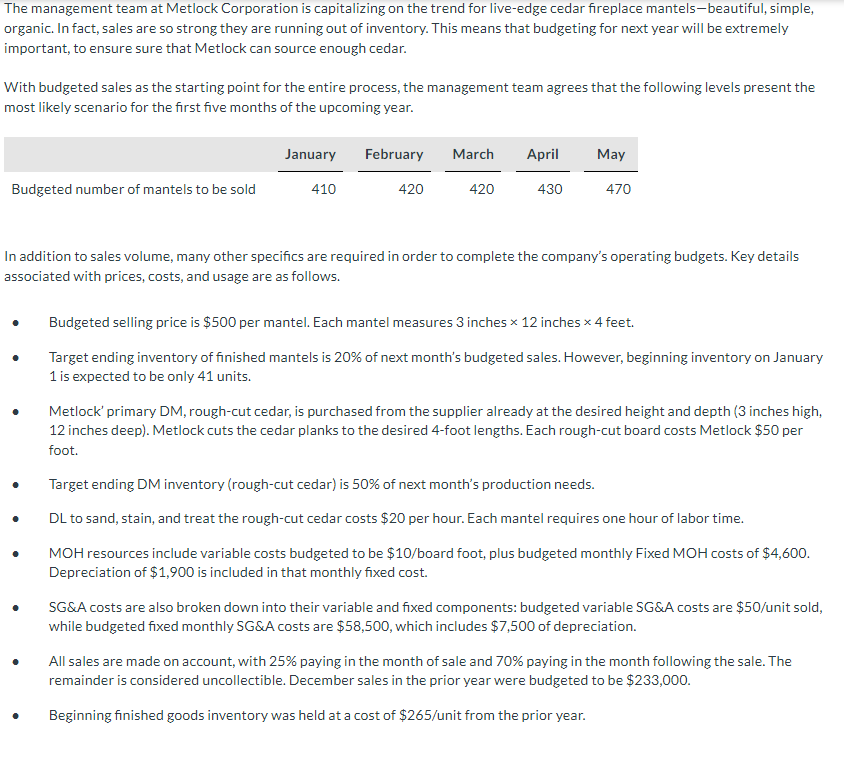

The management team at Metlock Corporation is capitalizing on the trend for live-edge cedar fireplace mantels-beautiful, simple, organic. In fact, sales are so strong

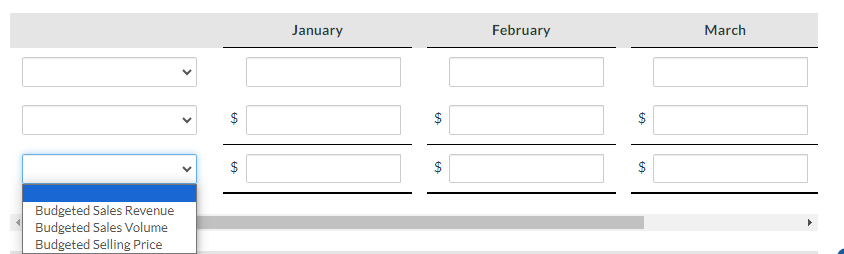

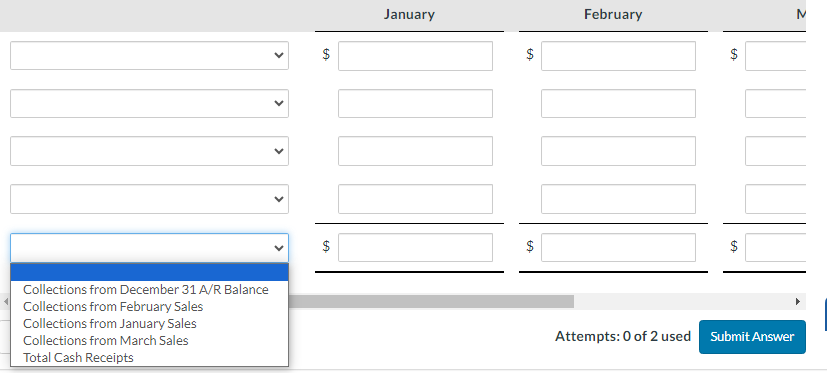

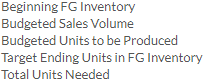

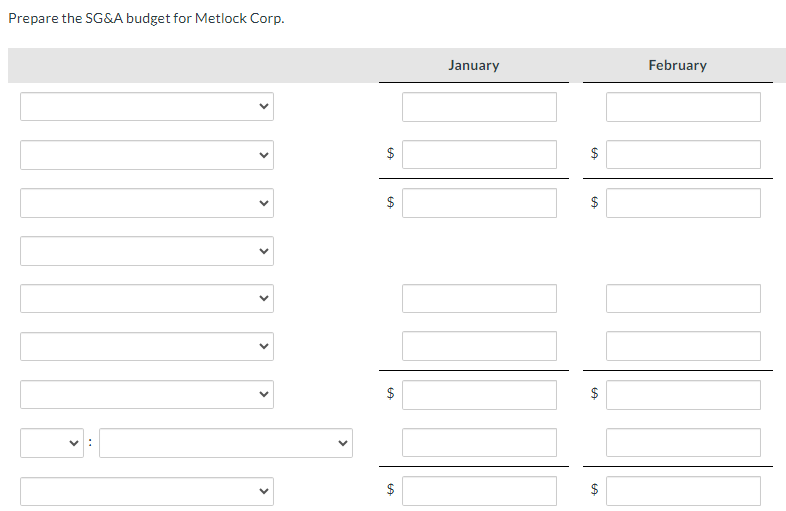

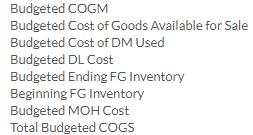

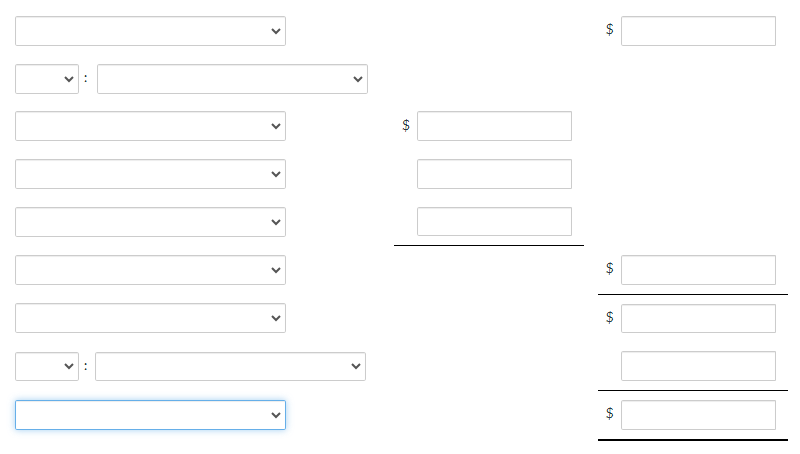

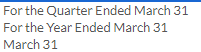

The management team at Metlock Corporation is capitalizing on the trend for live-edge cedar fireplace mantels-beautiful, simple, organic. In fact, sales are so strong they are running out of inventory. This means that budgeting for next year will be extremely important, to ensure sure that Metlock can source enough cedar. With budgeted sales as the starting point for the entire process, the management team agrees that the following levels present the most likely scenario for the first five months of the upcoming year. January February March April May Budgeted number of mantels to be sold 410 420 420 430 470 In addition to sales volume, many other specifics are required in order to complete the company's operating budgets. Key details associated with prices, costs, and usage are as follows. Budgeted selling price is $500 per mantel. Each mantel measures 3 inches x 12 inches x 4 feet. Target ending inventory of finished mantels is 20% of next month's budgeted sales. However, beginning inventory on January 1 is expected to be only 41 units. Metlock' primary DM, rough-cut cedar, is purchased from the supplier already at the desired height and depth (3 inches high, 12 inches deep). Metlock cuts the cedar planks to the desired 4-foot lengths. Each rough-cut board costs Metlock $50 per foot. Target ending DM inventory (rough-cut cedar) is 50% of next month's production needs. DL to sand, stain, and treat the rough-cut cedar costs $20 per hour. Each mantel requires one hour of labor time. MOH resources include variable costs budgeted to be $10/board foot, plus budgeted monthly Fixed MOH costs of $4,600. Depreciation of $1,900 is included in that monthly fixed cost. SG&A costs are also broken down into their variable and fixed components: budgeted variable SG&A costs are $50/unit sold, while budgeted fixed monthly SG&A costs are $58,500, which includes $7,500 of depreciation. All sales are made on account, with 25% paying in the month of sale and 70% paying in the month following the sale. The remainder is considered uncollectible. December sales in the prior year were budgeted to be $233,000. Beginning finished goods inventory was held at a cost of $265/unit from the prior year. Budgeted Sales Revenue Budgeted Sales Volume Budgeted Selling Price EA $ January + $ + February March + $ Collections from December 31 A/R Balance Collections from February Sales Collections from January Sales Collections from March Sales Total Cash Receipts $ +A GA January $ GA February Attempts: 0 of 2 used $ Submit Answer A Beginning FG Inventory Budgeted Sales Volume Budgeted Units to be Produced Target Ending Units in FG Inventory Total Units Needed Add Less : January February Beginning DM Inventory (Board Feet) Budgeted Board Feet of DM to be Purchased Budgeted Units to be Produced Desired Ending DM Inventory (Board Feet) DM Cost per Board Foot Quantity of DM per Unit (Board Feet) Total Budgeted Cost of DM Purchases Total DM Inventory Needs (Board Feet) Total Production Needs (Board Feet) Fabric : : > January February EA $ $ LA EA $ 6A Add Less Budgeted DL Cost per Hour Budgeted Units to be Produced Quantity of DL per Unit (Hours) Total Budgeted DL Cost Total Budgeted DL Hours Needed January February March $ $ $ $ + $ GA $ Budgeted DM Quantity Needed (Board Feet) Budgeted Fixed MOH Costs Budgeted Units to be Produced Budgeted Variable MOH Rate per Board Foot Depreciation on Plant Assets Non-cash MOH Costs Other Fixed MOH Costs Property Taxes and Insurance Quantity of DM per Unit (Board Feet) Total Budgeted Cash Needs for MOH Total Budgeted MOH Cost Total Budgeted Variable MOH Costs > > > > January > > $ > February $ $ > $ GA $ $ FA Add Less Budgeted Fixed SG&A Costs Budgeted Sales Volume Budgeted Variable SG&A Cost per Unit Depreciation Non-cash Depreciation Other Fixed SG&A Costs Total Budgeted Cash Needs for SG&A Total Budgeted SG&A Costs Total Budgeted Variable SG&A Costs Prepare the SG&A budget for Metlock Corp. > > $ January EA $ February $ EA EA $ $ $ Add Less Budgeted COGM Budgeted Cost of Goods Available for Sale Budgeted Cost of DM Used Budgeted DL Cost Budgeted Ending FG Inventory Beginning FG Inventory Budgeted MOH Cost Total Budgeted COGS Add Less $ CA $ $ 6A $ $ For the Quarter Ended March 31 For the Year Ended March 31 March 31 Cost of Goods Sold Gross Margin Operating Income Sales SG&A Expenses Add Less MetlockCompany Budgeted Income Statement : GA GA

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Excellence in Business Communication

Authors: John V. Thill, Courtland L. Bovee

9th edition

136103766, 978-0136103769