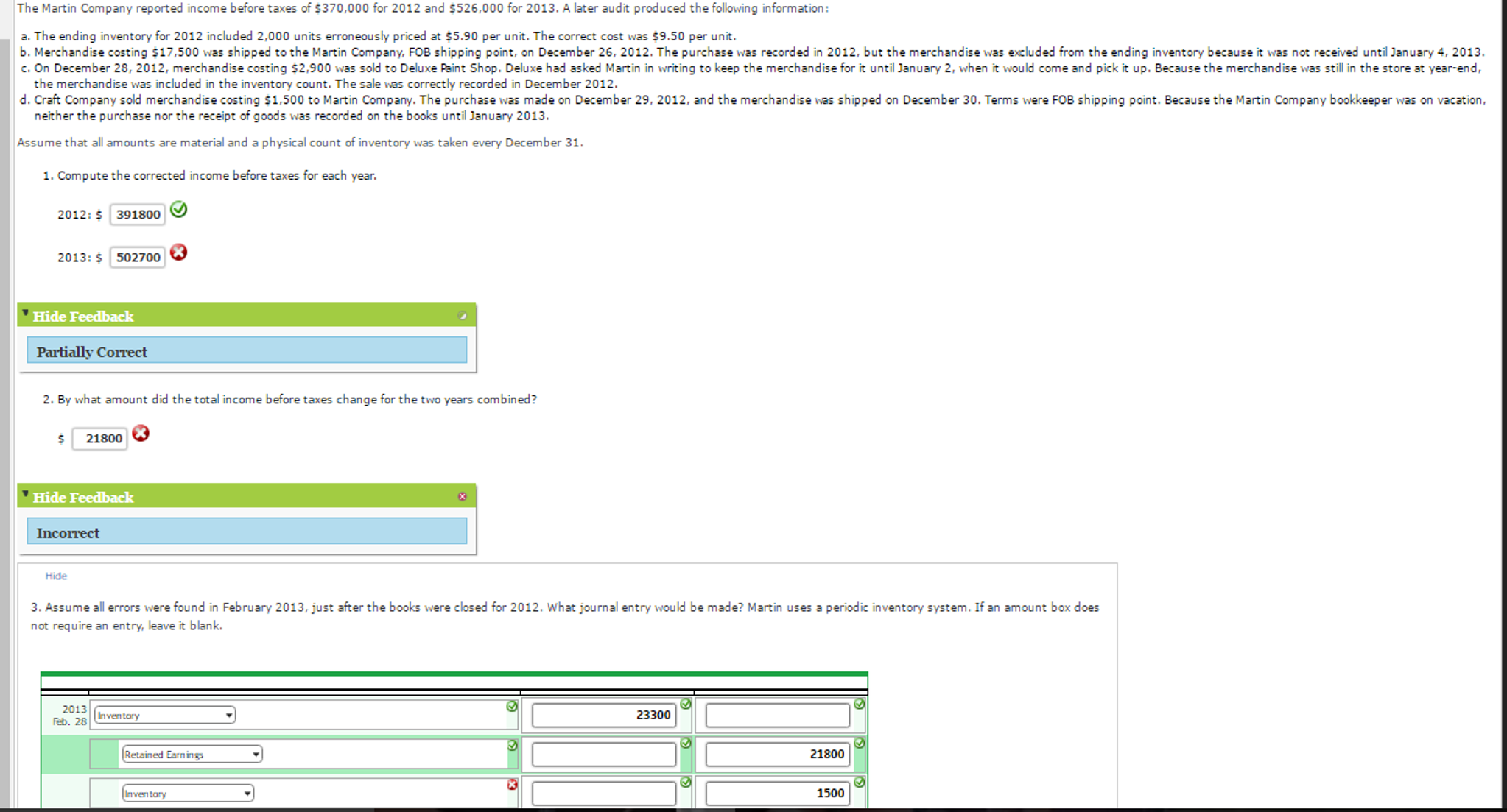

The Martin Company reported income before taxes of $370.000 for 2012 and $526.000 for 2013. A later audit produced the following information: The ending inventory for 2012 included 2,000 units erroneously priced at $5.90 per unit. The correct cost was S9.50 per unit. Merchandise costing $17.500 was shipped to the Martin Company, FOB shipping point, on December 26, 2012. The purchase was recorded in 2012, but the merchandise was excluded from the ending inventory because it was not received until January 4, 2013. On December 28, 2012, merchandise costing $2, 900 was sold to Deluxe feint Shop. Deluxe had asked Martin in writing to keep the merchandise for it until January 2, when it would come and pick it up. Because the merchandise was still in the store at year-end, the merchandise was included in the inventory count. The sale was correctly recorded in December 2012. Craft Company sold merchandise costing $1, 500 to Martin Company. The purchase was made on December 29, 2012, and the merchandise was shipped on December 30. Terms were FOB shipping point. Because the Martin Company bookkeeper was on vacation, neither the purchase nor the receipt of goods was recorded on the books until January 2013. Assume that all amounts are material and a physical count of inventory was taken every December 31. Compute the corrected income before taxes for each year. 2012: $ 2013: $ By what amount did the total income before taxes change for the two years combined? Assume all errors were found in February 2013, just after the books were closed for 2012. What journal entry would be made? Martin uses a periodic inventory system. If an amount box does not require an entry, leave it blank. The Martin Company reported income before taxes of $370.000 for 2012 and $526.000 for 2013. A later audit produced the following information: The ending inventory for 2012 included 2,000 units erroneously priced at $5.90 per unit. The correct cost was S9.50 per unit. Merchandise costing $17.500 was shipped to the Martin Company, FOB shipping point, on December 26, 2012. The purchase was recorded in 2012, but the merchandise was excluded from the ending inventory because it was not received until January 4, 2013. On December 28, 2012, merchandise costing $2, 900 was sold to Deluxe feint Shop. Deluxe had asked Martin in writing to keep the merchandise for it until January 2, when it would come and pick it up. Because the merchandise was still in the store at year-end, the merchandise was included in the inventory count. The sale was correctly recorded in December 2012. Craft Company sold merchandise costing $1, 500 to Martin Company. The purchase was made on December 29, 2012, and the merchandise was shipped on December 30. Terms were FOB shipping point. Because the Martin Company bookkeeper was on vacation, neither the purchase nor the receipt of goods was recorded on the books until January 2013. Assume that all amounts are material and a physical count of inventory was taken every December 31. Compute the corrected income before taxes for each year. 2012: $ 2013: $ By what amount did the total income before taxes change for the two years combined? Assume all errors were found in February 2013, just after the books were closed for 2012. What journal entry would be made? Martin uses a periodic inventory system. If an amount box does not require an entry, leave it blank