The mean-variance optimization is known for having high sensitivity to changing target return. The Chief Investment Officer (CIO) would like you to test the sensitivity of the mean-variance optimization to a change in the portfolio target return. Explain your results.

The mean-variance optimization is known for having high sensitivity to changing target return. The Chief Investment Officer (CIO) would like you to test the sensitivity of the mean-variance optimization to a change in the portfolio target return. Explain your results.

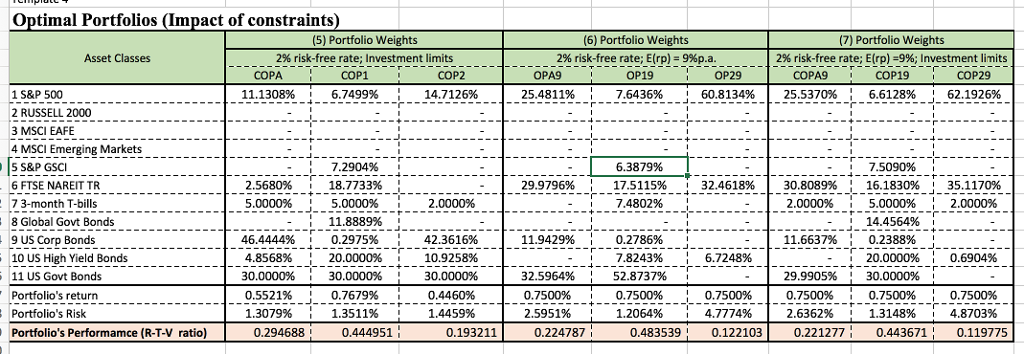

Optimal Portfolios (Impact of constraints (5) Portfolio Weights (6) Portfolio Weights 7) Portfolio Weights Asset Classes 2% free rate; E(rp 99%p.a. 29% risk-free rate 2% risk-free rate; E(rp) -9%; investment limits nvestment limits COPA. COP1 COP22 OPA9 OP19 OP29 COPA9 COP19 COP29 6.749996 25.5370% 6.6128% 11.1308% 14.7126% 1 S&P 500 25.4811% 7.6436% 60.8134% 62.1926% 2 RUSSELL 2000 3 MSCI EAFE 4 MSCI Emerging Markets 7.2904 6.3879% 7.5090% 5 S&P GSC 29.9796% 6 FTSE NAREIT TR 2.5680% 18.7733% 32.4618% 30.8089% H 16.1830% 35.1170% 17.5115% 7 3-month T-bills 5.0000% 2.0000% 7.4802% 2.0000% 2.0000% 5.0000% 5.0000% 14.4564% 8 Global Govt Bonds 11.8889% 11.6637% 90 US Corp Bonds 46.4444% 0.2975% 42.3616% 11.9429% 0.2786% 0.2388% 10 US High Yield Bonds 4.8568% 20.0000% 10.9258% 7.8243% 6.7248% 20.0000% 0.6904% 30.0000% 30.0000% 30.0000% 32.5964% 52.8737% 29.9905% 30.0000% 11 US Govt Bonds 0.4A60% --1- 23951% ---0.7679% 1.2064% 2.6362% 4.8703% Portfolio's Performamce (R-T-V ratio) 0.294688 0.444951 H 0.193211 0.224787 0.483539 0.122103 0.221277 H 0.443671 H 0.119775 Optimal Portfolios (Impact of constraints (5) Portfolio Weights (6) Portfolio Weights 7) Portfolio Weights Asset Classes 2% free rate; E(rp 99%p.a. 29% risk-free rate 2% risk-free rate; E(rp) -9%; investment limits nvestment limits COPA. COP1 COP22 OPA9 OP19 OP29 COPA9 COP19 COP29 6.749996 25.5370% 6.6128% 11.1308% 14.7126% 1 S&P 500 25.4811% 7.6436% 60.8134% 62.1926% 2 RUSSELL 2000 3 MSCI EAFE 4 MSCI Emerging Markets 7.2904 6.3879% 7.5090% 5 S&P GSC 29.9796% 6 FTSE NAREIT TR 2.5680% 18.7733% 32.4618% 30.8089% H 16.1830% 35.1170% 17.5115% 7 3-month T-bills 5.0000% 2.0000% 7.4802% 2.0000% 2.0000% 5.0000% 5.0000% 14.4564% 8 Global Govt Bonds 11.8889% 11.6637% 90 US Corp Bonds 46.4444% 0.2975% 42.3616% 11.9429% 0.2786% 0.2388% 10 US High Yield Bonds 4.8568% 20.0000% 10.9258% 7.8243% 6.7248% 20.0000% 0.6904% 30.0000% 30.0000% 30.0000% 32.5964% 52.8737% 29.9905% 30.0000% 11 US Govt Bonds 0.4A60% --1- 23951% ---0.7679% 1.2064% 2.6362% 4.8703% Portfolio's Performamce (R-T-V ratio) 0.294688 0.444951 H 0.193211 0.224787 0.483539 0.122103 0.221277 H 0.443671 H 0.119775