Answered step by step

Verified Expert Solution

Question

1 Approved Answer

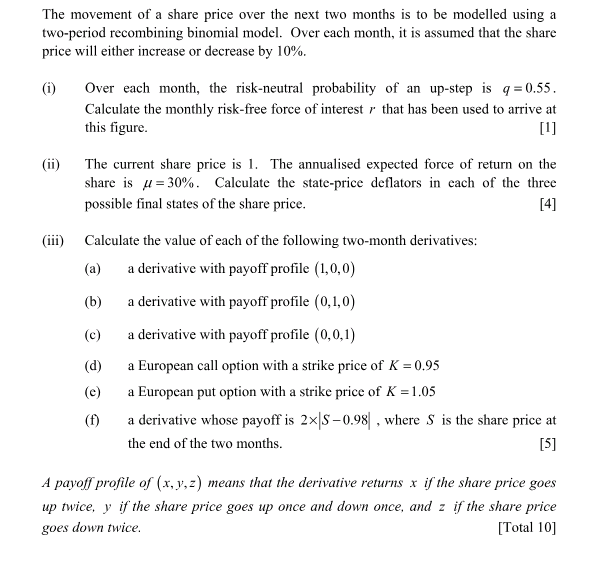

The movement of a share price over the next two months is to be modelled using a two-period recombining binomial model. Over each month,

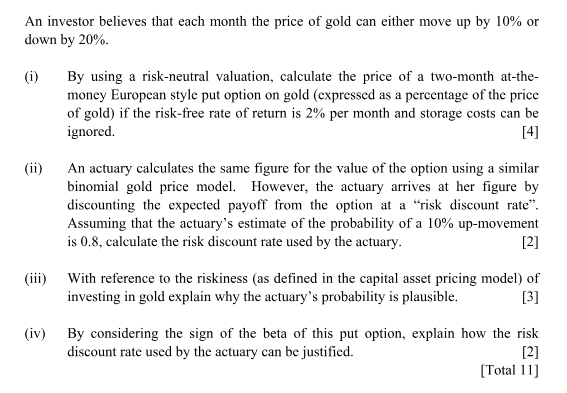

The movement of a share price over the next two months is to be modelled using a two-period recombining binomial model. Over each month, it is assumed that the share price will either increase or decrease by 10%. (i) Over each month, the risk-neutral probability of an up-step is q=0.55. Calculate the monthly risk-free force of interest that has been used to arrive at this figure. [1] (ii) The current share price is 1. The annualised expected force of return on the share is =30%. Calculate the state-price deflators in each of the three possible final states of the share price. [4] (iii) Calculate the value of each of the following two-month derivatives: (a) a derivative with payoff profile (1,0,0) (b) a derivative with payoff profile (0,1,0) (c) a derivative with payoff profile (0,0,1) (d) a European call option with a strike price of K = 0.95 (e) a European put option with a strike price of K = 1.05 (f) a derivative whose payoff is 2|S-0.98, where S is the share price at the end of the two months. [5] A payoff profile of (x,y,z) means that the derivative returns x if the share price goes up twice, y if the share price goes up once and down once, and z if the share price goes down twice. [Total 10] An investor believes that each month the price of gold can either move up by 10% or down by 20%. (i) (ii) By using a risk-neutral valuation, calculate the price of a two-month at-the- money European style put option on gold (expressed as a percentage of the price of gold) if the risk-free rate of return is 2% per month and storage costs can be ignored. [4] An actuary calculates the same figure for the value of the option using a similar binomial gold price model. However, the actuary arrives at her figure by discounting the expected payoff from the option at a "risk discount rate". Assuming that the actuary's estimate of the probability of a 10% up-movement is 0.8, calculate the risk discount rate used by the actuary. [2] (iii) With reference to the riskiness (as defined in the capital asset pricing model) of investing in gold explain why the actuary's probability is plausible. [3] (iv) By considering the sign of the beta of this put option, explain how the risk discount rate used by the actuary can be justified. [2] [Total 11]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial statements

Authors: Stephen Barrad

5th Edition

978-007802531, 9780324186383, 032418638X