Answered step by step

Verified Expert Solution

Question

1 Approved Answer

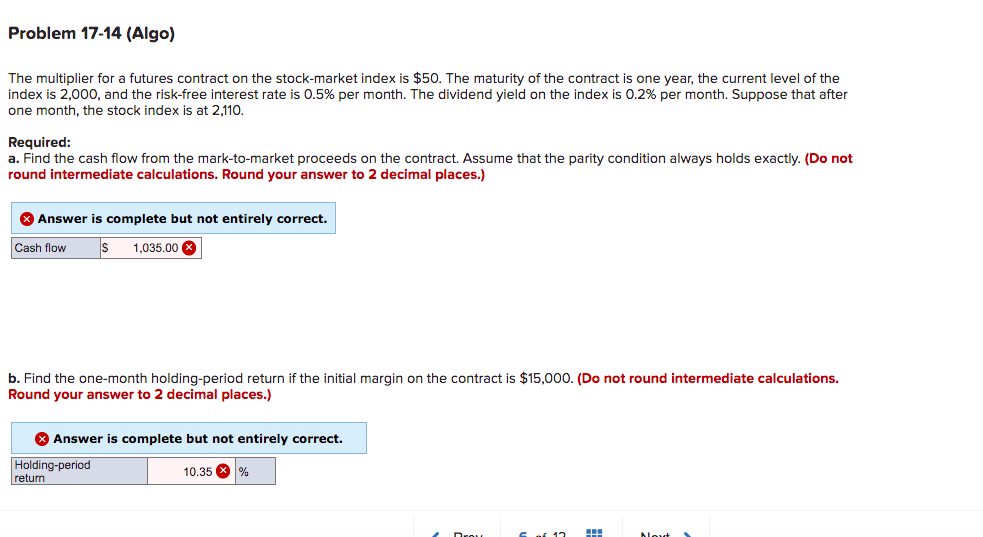

The multiplier for a futures contract on the stock-market index is $50. The maturity of the contract is one year, the current level of the

The multiplier for a futures contract on the stock-market index is $50. The maturity of the contract is one year, the current level of the index is 2,000 , and the risk-free interest rate is 0.5% per month. The dividend yield on the index is 0.2% per month. Suppose that after one month, the stock index is at 2,110. Required: a. Find the cash flow from the mark-to-market proceeds on the contract. Assume that the parity condition always holds exactly. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Answer is complete but not entirely correct. b. Find the one-month holding-period return if the initial margin on the contract is $15,000. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Answer is complete but not entirely correct

The multiplier for a futures contract on the stock-market index is $50. The maturity of the contract is one year, the current level of the index is 2,000 , and the risk-free interest rate is 0.5% per month. The dividend yield on the index is 0.2% per month. Suppose that after one month, the stock index is at 2,110. Required: a. Find the cash flow from the mark-to-market proceeds on the contract. Assume that the parity condition always holds exactly. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Answer is complete but not entirely correct. b. Find the one-month holding-period return if the initial margin on the contract is $15,000. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Answer is complete but not entirely correct Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Legaltech Book

Authors: Susanne Chishti ,Sophia Adams Bhatti ,Akber Datoo ,Drago Indjic

1st Edition

1119574277, 978-1119574279