Answered step by step

Verified Expert Solution

Question

1 Approved Answer

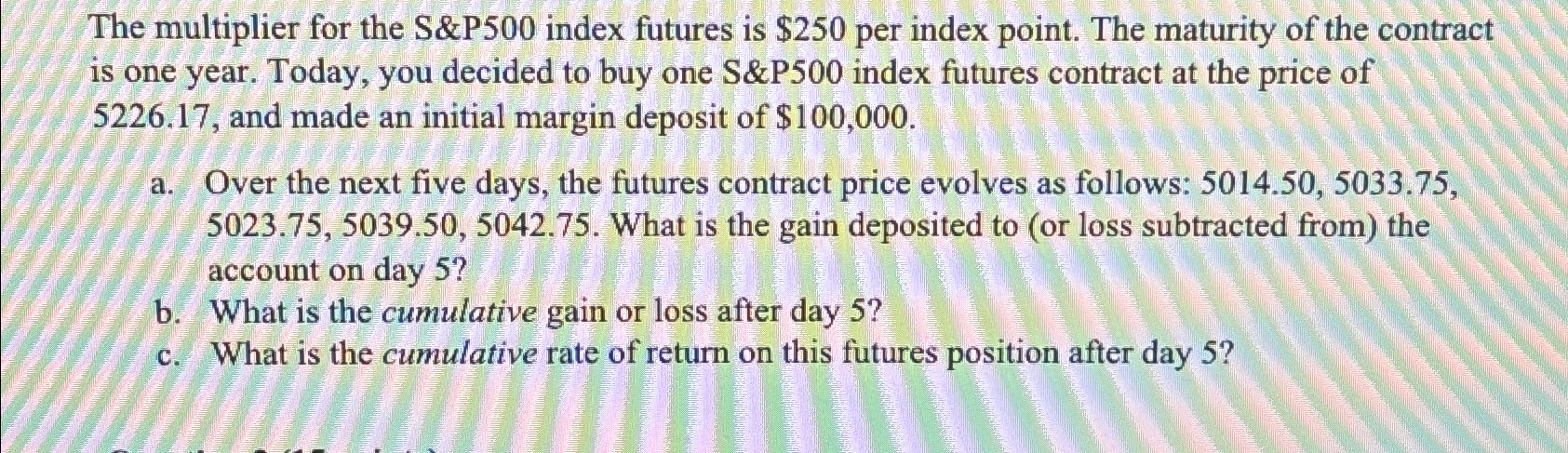

The multiplier for the S&P 5 0 0 index futures is $ 2 5 0 per index point. The maturity of the contract is one

The multiplier for the S&P index futures is $ per index point. The maturity of the contract is one year. Today, you decided to buy one S&P index futures contract at the price of and made an initial margin deposit of $

a Over the next five days, the futures contract price evolves as follows: What is the gain deposited to or loss subtracted from the account on day

b What is the cumulative gain or loss after day

c What is the cumulative rate of return on this futures position after day

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Ecological Money And Finance

Authors: Thomas Lagoarde-Segot

1st Edition

3031142314, 978-3031142314